An important question is how severe the downturn will be and how long will it last? A related question is whether one can observe external or internal economic imbalances in Russia that could trigger an abrupt further collapse.

Oil and the ruble

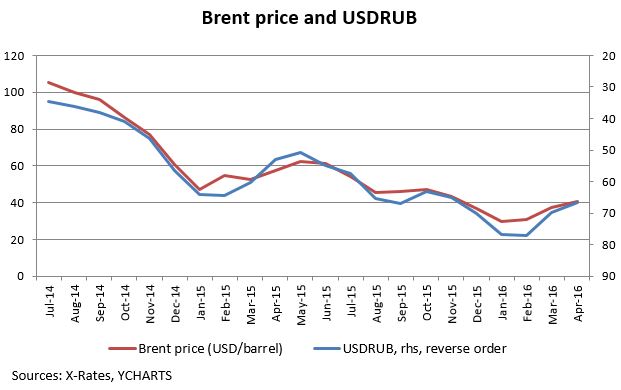

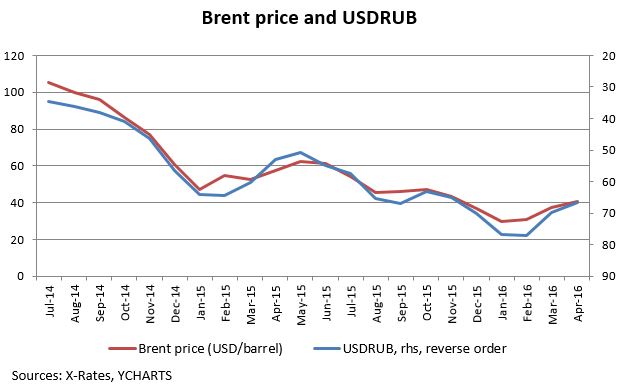

One thing that has collapsed already is the value of the ruble. The USDRUB exchange rate almost perfectly mirrors the decline in oil price (see the chart below). As the oil price has dropped to about half its earlier level, the ruble price of the dollar has approximately doubled.

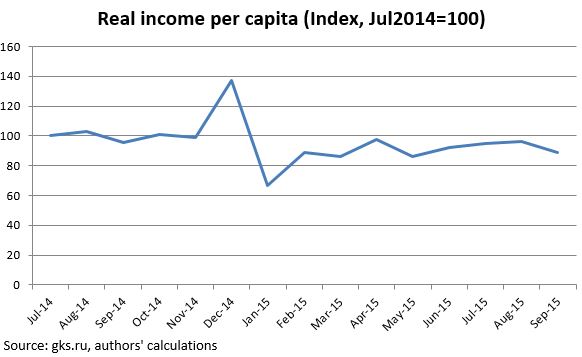

As a result of the collapse in the USDRUB exchange rate, the USD-equivalent income of the average Russian in the third quarter of 2015 had fallen by more than one third compared to the summer of 2014. Thus, fewer Russians can now afford to go abroad or buy imported goods. However, the domestic purchasing power had declined relatively little – by about 10% (see the chart below, we were not able to adjust it for the peak/trough at the end of the year). According to the World Bank, the average consumer price inflation in Russia in 2015 reached about 15% while the nominal average income in rubles was growing.

Oil prices are volatile and difficult to predict, but the recent decline reminds observers of the severe and protracted decline that began in 1980. In terms of 2015 dollars, the oil price fell from around USD100 per barrel in 1980, and it did not return to USD100 until 2008. The price dropped below USD40 by 1986, and it did not rise to USD40 again until 2004 (Grennes and Goodwin). This extended period of cheap oil coincided with the disintegration of the Soviet Union. History is not destiny, but large and persistent swings in oil prices have not been uncommon.

Economic growth as a way to legitimize power

When Vladimir Putin rose to power in 2000, he inherited severe economic problems. Since then, the Russian economy has grown, real wages increased consistently from 2000 to 2013, but they have declined in 2014-15 (Economist 2016a). However, people have come to expect further success. After all, economic growth is one of the ways to legitimize power (another one being free and democratic elections). Various Russian economists and officials have warned that conditions may get worse (Zubarevich). It remains to be seen, how much economic hardship the Russian people will tolerate.

A reduction in the percentage of Russians living in poverty was a major achievement of the Putin administration until 2014. However, that trend has now reversed. Russian government data show that the share of Russians in poverty has risen since the oil crisis (Guardian). However, some wealthy Russians appear to be protected from the adverse effects of the crisis. The Economist has constructed an index of crony capitalism based on the wealth of oligarchs relative to GDP, and Russia is the most extreme crony capitalist in the world (Economist 2016b). Moreover, Russia is a country with relatively many billionaires, but relatively few millionaires. Russian officials are now considering raising the current flat income tax rate from 13% to 20% or moving to a progressive income tax (Wall Street Journal 2016b).

Russia also faces debt problems for some important financial institutions, such as the Vneshekonombank (VEB). Since becoming Russia’s development bank in 2007, it has made many bad loans, and may not survive without a bailout (Wall Street Journal 2016a).

The low oil price is a fundamental problem for the Russian economy, but it is largely beyond the control of Russian officials. The entire world energy economy has become more competitive due to improved energy efficiency and innovations such as the shale revolution. However, the government of Russia has at the same time failed to break the so-called resource curse and diversify the economy away from dependence on export of natural resources.

Internal and external equilibria

The above might lead one to think that a yawning gap has opened up in the public finances of Russia. The budget deficit has indeed increased. However, since a significant part of the budget income is oil based and USD denominated, the declining exchange rate has largely meant that the fall in USD revenue has been compensated by exchange rate adjustment. The result has been a budget deficit of slightly over 3% of GDP in 2015 (see the chart below) while the non-oil deficit has been relatively stable at 10-11% of GDP. The public debt to GDP is low at just above 15%.

Russia has been running a current account surplus for many years, as a result of which its net international investment position is positive. In addition, its foreign liabilities are largely in the form of equity investment. Issuing equity rather than debt protects against having to pay more rubles to service dollar-denominated debt when the ruble depreciates. This explains why the net foreign assets are the highest in the years of downturn when the stock market indexes are collapsing (see the chart below). Thus, also on the external front the economy of Russia is rather balanced.

In 2014 the Central Bank of Russia initially attempted to mitigate the collapse of the ruble by selling its foreign reserves. By 2015 it had largely stopped doing that, and allowed greater flexibility of the exchange rate. In fact, there has been more than one episode in both 2015 and the first quarter of 2016 when the Central Bank of Russia has bought foreign exchange on the currency market and kept the USDRUB rate below its market value. The reserve position of the Central Bank has stabilized as a result (see the chart below).

Conclusion

The economy of Russia has clearly been negatively affected by the collapse of the oil price. The corresponding fall of the ruble, however, while significantly reducing the external purchasing power of the average Russian, has also had the positive side effect of helping Russia keep its budget deficit at a moderate level. In addition, the Net International Investment Position of Russia is positive and has been strengthened further by the decrease in its stock market capitalization. The important remaining question is whether the remaining decline in the Russian economy will be mild and brief or severe and long-lasting. The answer depends partly on developments in Russia, but it also depends heavily on developments in world energy markets Currently the baseline scenario appears to be that of a prolonged moderate decline or stagnation rather than an abrupt collapse.

References

Economist 2016a. „Russia’s Economy: Phase Two”. January 23.

Economist. 2016b. „Our Crony Capitalism Index: the Party Winds Down”. May 7.

Grennes, Thomas, and Barry K. Goodwin. 2015. „Perspectives on Food, Water, and Agricultural Trade in the Gulf Cooperation Council”. DERASAT Journal, December.

Guardian. 2016. „Millions More Russians Living in Poverty as Economic Crisis Bites”. March 21.

Moscow Times. 2016. „How Putin’s Bank Became Russia’s $20 billion Problem”. March 3.

Wall Street Journal. 2016a. „Key Russian Bank Needs Bailout”. April 11.

Wall Street Journal. 2016b. “Russia Weighs Tough Steps to Fill Budget Gap”. May 16.

Zubarevich, Natalya. 2016. „Russian Economic Crisis Risks Stagnation, Degradation”. Moscow Times, March 25.