As opposed to the FT, though, I would argue that the transmission mechanism is at least not getting worse in Spain and Portugal, and worsening in Italy. Italy is the only periphery economy (where data is made available) where the corporate borrowing costs are higher since the peak of corporate lending rates in the Euro area in July 2011.

The FT is wrong. It takes Spain as the case study and uses the incorrect corporate lending rate information. Specifically, according to the FT (bolded by RW):

The interest rate charged by banks on a corporate loan of up to €1m lasting between one and five years – which would typically be taken out by a small business – was 6.5 per cent in July in Spain, according to the ECB figures.

True, the rate on new business loans up to and including €1 mn with maturity of 1-5 years did see an average borrowing rate of 6.5% in July. However, corporate loans up to and including €1 mn with maturity of greater than 5 years saw a drop in borrowing costs of 1.4% in July to 5.17% . The 5.17% rate is the rate that should be quoted, rather than the 6.5% rate.

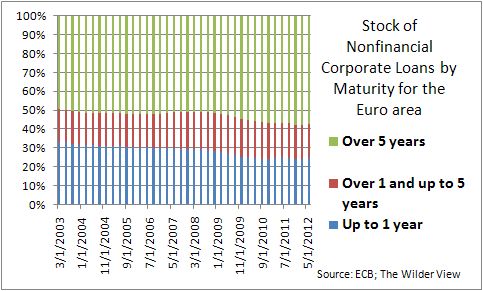

The 2012 Euro area stock of outstanding debt shows clearly that 57% of corporate loans had been made with maturity of greater than 5 years – the ECB provides no breakdown of loan data by maturity at the country level, so the FT must have been referring to the ECB’s Euro area data as the ‘typical loan’.

As demonstrated in the chart below, the story is much more complicated than the FT curtly portrays – it’s not just ‘Spain’ versus ‘Germany’. French corporate borrowing costs barely budged since July 2011. Furthermore, the corporate borrowing rates in Spain are improving rather materially compared to those in Italy and Portugal.

Italian corporate borrowing are up 0.67% since the peak of EA corporate lending rates in July 2011 (the ECB hiked its policy rate on July 13). Spanish corporates, on the other hand, saw corporate borrowing costs fall the most of all the periphery economies, -1.35% since July 2011.

As demonstrated in the illustration below, the core is benefiting largely from ECB rate cuts compared to the periphery (chart 1 below). However, on a 3-month moving average (the rates moves are pretty choppy in Spain), the transmission mechanism in Spain is improving relative to that Italy and Portugal (chart 2 below). Using the correct data, the FT should have included this information in their article.

Rebecca Wilder