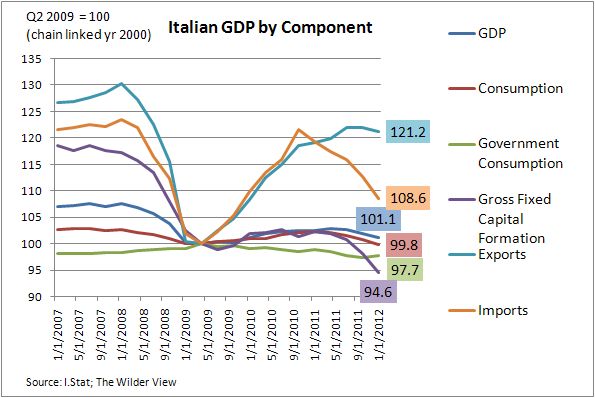

- Gross fixed capital formation (investment net of inventory formation) fell 3.6% over the quarter, or 13.7% at an annualized rate. This was the fastest quarterly rate of decline since Q1 2009 when GFCF fell 5% over the quarter.

- Private consumption dropped 1.0% over the quarter, or 3.9% at an annualized rate

- Imports fell 3.6%, or 13.6% at an annualized rate

- Exports fell 0.6%, or 2.2% at an annualized rate

- The only positive contribution to domestic spending was government consumption, which increased 0.4% over the quarter, or 1.4% at an annualized rate.

Italy’s real GDP is only 1.1% higher than its lowest point during the recession (Q2 2009). Furthermore, gross fixed capital formation has dropped at an increasing rate for four consecutive quarters. Hope for stabilization eludes, as the current business confidence survey continues its decent – IStat manufacturing confidence was 86.2 in May, which was the second lowest level since the outset of the EMU and well below the 100 average since 2000. Broadly speaking, the economy is imploding.

Don’t pin your hopes on exports. The contribution of exports to real GDP growth has dropped for two consecutive quarters, bucking a trend of positive contribution since the middle of 2009. The only reason that the net export contribution was positive in Q1 was due to the +1% contribution coming from a sharp decline in imports. This cannot be sustained, as the crisis of confidence has begun.

(Note: In the chart below, if real import growth is positive, then the contribution is negative; and if the real import growth is negative, then the contribution is positive.)

This is a product of failed policy at the Euro area level, and something needs to be done to break the positive feedback loop.

Also Read: The Policymaker’s Fear of the Italian Penalty Shot