The accompanying database of the factors in the MIP score is made available at Eurostat. This database is particularly exciting for a data geek like me. Included in the MIP database is an indicator that I’ve wanted to construct for some time: country level exports as a share of world exports. World export share is a much broader measure of competitiveness than the commonly reported export share of country GDP.

Belgium, which is one of the 12 countries on review for potential imbalances, has experienced an 0.5 ppt drop in world export share, 2.4% in 2002 to 1.9% in 2010. Seems like a big drop – but what does a 1.9% export share mean in terms of the size of the Belgian population in the Euro area 12 (EA 12)? In 2010, Belgium’s world export share was 2.2 times what it’s EA 12 population share implies – loss of competitiveness, yes, but still competitive.

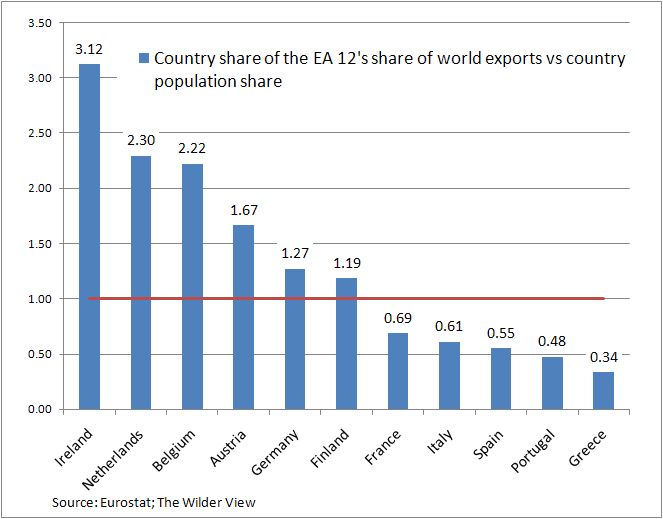

The chart below illustrates the following: (country world export share as a share of EA 12 world export share)/(country share of EA 12 population). The data can be downloaded at Eurostat: export share, and population).

If the index level > 1, then the country has a greater share of the EA 12 world export share than that implied by its population as compared to that of the EA 12 – competitive; If the index level < 1, then the country has a smaller share of the EA 12 world export share than that implied by its population relative to that of the EA 12 – not competitive.

Some takeaways from this chart are:

- All the usual ‘competitive’ suspects are at the top: Ireland, Netherlands, Belgium, Austria, Germany, and Finland. These countries hold in excess of 1.2 to 3.1 times EA 12 world export share than their relative size in the EA 12.

- All of the usual ‘uncompetitive’ suspects are at the bottom: Greece, Portugal, Spain, Italy, and France. These countries hold anywhere from 30% to 70% less world export share of that in the EA 12 than their population share would imply.

- Ireland is the most competitive in this respect, and Greece is the least.

- Germany is more in the middle with just a 27% higher export share of the EA world export share than that implied by its population share….

That’s it for today. I’d like to hear your feedback.

Rebecca