First, policy was a success, given the private sector was recuperating from the bursting of a credit and investment bubble.

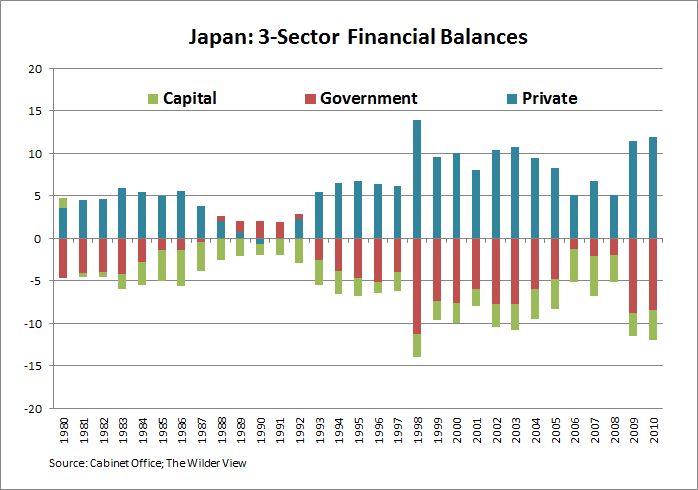

The chart below illustrates the 3-sector financial balances model – read Scott Fullwiler on New Economic Perspectives for a detailed description of the 3-sector financial balances model. According to this identity, the capital account plus government net saving plus private net saving must equal zero. For a given level of the capital account (Japan’s capital account has been quite stable over the years), when the private sector increases net saving, aggregate demand declines and government net saving declines.

In the early 1990s, all sectors were roughly in balance. However, since then government debt surged in response to a like rise in the private sector desire to save. One could argue that the government deficits and accumulated debts were indeed required, hailing the government’s actions a policy success. However, I contend that this has been a missed policy opportunity rather than overall success.

The second chart illustrates the same financial balances model, but broken down into 4 sectors: the capital account plus government net saving plus household net saving plus corporate net saving must equal zero – household plus corporate net saving equals private net saving in the chart above.

Household net saving has steadily declined with the ageing population. But the corporate saving rate has been positive every year since 1996, offsetting the stimulating effect an ageing population could have on domestic demand. So here’s the policy failure: the government missed the opportunity for structural reform targeted at the corporate saving rate.

Had the government created incentives for a reduction in the corporate saving rate, the returns could have/would have been filtered back into the domestic economy. Now they’re in a state of panic, watching the European debt crisis with an anxious eye. Why else would Noda be pushing so hard for a new tax?

Martin Wolf commented on this one year ago:

Japan’s aim now must be to achieve domestically driven growth. The most important requirement is a big reduction in corporate saving. Mr Smithers argues that this will happen naturally, since savings are largely capital consumption, itself the product of the history of excessive investment. I would add that if ever an economy needed a market in corporate control, to shift cash out of the hands of sleepy managements, Japan is it. Not being beholden to Japan’s corporate establishment, the new government should adopt policies that would change corporate behaviour, at last.

As with all credit cycles, the burden of debt falls on the government as the private sector recoups. However, in Japan’s case the government missed a great opportunity for structural reform before the crash associated with credit cycles in other major developed economies (the USA).