No, we aren’t celebrating either the Monarch or the ship. We’re talking about the Fed’s Quantitative Easing. I’m going to discuss the basics of QE and explain why it’s Much Ado about almost Nothing.

This past September the Fed announced full speed ahead with QE3. Three’s a charm, or so they hope. This time, the Fed promised to buy $40 billion worth of mortgage backed securities (MBSs) every month through the end of the year, and to keep what is essentially a zero interest policy (ZIRP) in place through mid 2015. The Fed also announced that it will purchase other long-maturity assets to bring the total monthly purchases up to $85 billion, with the bias toward the long end expected to put downward pressure on long term interest rates. The Fed made clear that QE3 is open-ended, to continue as long as necessary to stimulate to a robust economic recovery.

There are two reasons why economic stimulus has come down to reliance on the Fed’s QE. First, policy-makers have bought the Austerian view that fiscal policy is out-of-bounds; some believe it doesn’t work, others believe government has “run out of money”. Both of those views are pure nonsense, but beyond the scope of this blog.

The second reason is that Chairman Bernanke is enamored with the view that proper monetary policy could have avoided the American Great Depression as well as the Japanese lost decade(s)—two and counting. Essentially, he staked his academic career on the argument that there’s more that the central bank can do, beyond pushing its overnight rate (fed funds rate in the US) to zero (ZIRP).

When the crisis hit the US in 2007, Bernanke followed the Japanese example by quickly relaxing monetary policy, rapidly pushing down the policy interest rate. After some fumbling around, the Fed also gradually opened its discount window to lend an unprecedented amount of reserves to troubled institutions. As I’ve discussed in previous blogs, all told the Fed spent and lent a cumulative total of $29 trillion to rescue the banks.

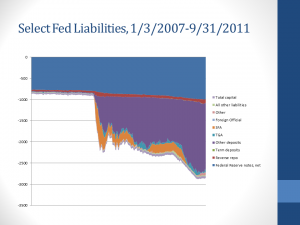

And the Fed’s balance sheet literally exploded—which has got our quantity theory Monetarists and Austrians and Ron Paul followers hyperventilating about hyperinflation. The following graph documents the spectacular growth of the Fed’s liabilities, most of which are “deposits”, that is bank reserves. (See here for discussion: http://www.levyinstitute.org/pubs/wp_698.pdf)

But that didn’t put the economy on the road to recovery. (Surprise, surprise! Bailing out Wall Street doesn’t help Main Street.)

And so the Chairman got the chance to try out his pet theory. The Fed should go beyond ZIRP to try unconventional policy, namely, it should continue to buy assets even after it had driven short term interest rates to the zero lower bound. Over the course of the three rounds of Quantitative Easing the Fed has bought prodigious amounts of Treasuries and MBSs. The following graph shows what the Fed bought. (For detailed explanation, and a key to the abbreviations, see here: http://www.levyinstitute.org/pubs/wp_698.pdf)

When the Fed buys assets, it purchases them by crediting banks with reserves. So the result of QE is that the Fed’s balance sheet grows rapidly—to, literally, trillions of dollars. At the same time, banks exchange the assets they are selling (the Treasuries and MBSs that the Fed is buying) for credits to their reserves held at the Fed. Normally, banks try to minimize reserve holdings—to what they need to cover payments clearing (banks clear accounts with one another using reserves) as well as Fed-imposed required reserve ratios. With QE, the banks have ended up with humongous quantities of excess reserves.

As we said, normally banks would not hold excess reserves voluntarily—reserves used to earn zero, so banks would try to lend them out in the fed funds market (to other banks). But in the ZIRP environment, they can’t get any return on lending reserves. Further, the Fed switched policy in the aftermath of the crisis so that it now pays a small, positive return on reserves. So the banks are holding the excess reserves and the Fed credits them with a bit of interest. They aren’t thrilled with that but there’s nothing they can do: the Fed offers them a price they cannot refuse on the Treasuries and MBSs it wants to buy, and they get stuck with the reserves.

A lot of people—including policy makers—exhort the banks to “lend out the reserves” on the notion that this would “get the economy going”. There are two problems with that. First, banks can lend reserves only to other banks—and all the other banks have exactly the same problem: too many reserves. A bank cannot lend reserves to your household or firm. You do not have an account at the Fed, so there is no operational maneuver that would allow you to borrow the reserves (when a bank lends reserves to another bank, the Fed debits the lending bank’s reserves and credits the borrowing bank’s reserves). Unless you are a bank, you cannot borrow them.

The second problem is that banks don’t need reserves in order to lend. What they need is good, willing, and credit-worthy borrowers. That is what is sadly lacking. Those who are credit-worthy are not willing; those who are willing are mostly not credit-worthy.

And we should be glad that banks are not currently lending to the uncredit-worthy. Here’s why: that’s what got us into this mess in the first place.

Indeed, the mountain of debt that US households are buried under makes the whole Bernanke notion that we need to get banks lending again just plain ludicrous. I don’t want banks to lend. I don’t want households to borrow. What we need is to work off the private debt—pay it down or default on it.

Some believe that the path to recovery is to get firms to borrow. Again, I think that is wrong-headed. Firms are actually wallowing in cash—they’ve cut costs, fired workers, and stopped spending in order to shore up their cash reserves. They don’t need banks. Indeed, they mostly stopped using banks to finance their spending a long time ago, as they shifted to commercial paper and other nonbank funding.

Yes, I know that the story is different for small firms—they don’t have cash flow and they aren’t considered credit-worthy so they cannot borrow. They are in a sense collateral damage—Wall Street screwed the economy and households and small business are paying the price. The solution is not more debt for them. If anything, small firms need to do the same thing that most households need to do: reduce debt.

So, we’ve got banks that don’t want to lend and households and small firms that shouldn’t borrow. We’ve got bigger firms hoarding cash. We have what Richard Koo calls a “balance sheet recession”: too much debt and a strong incentive to de-lever. Firms and households are not only cutting spending, they are also trying to sell assets to pay back debt. And so asset prices are falling.

All the more reason why banks don’t want to lend. The assets that could serve as collateral are falling in value.

Is there a way out? Yes there is. There is only one entity in the US that can spend more in a balance sheet recession: Uncle Sam. But Washington won’t let Sam do it. And so we will not recover.

That is the lesson Chairman Bernanke should have learned from Japan: if you don’t ramp up the fiscal stimulus, and keep it ramped up until a full blown recovery has occurred, you will remain trapped in recession.

To be sure, it is not Bernanke’s fault that Washington won’t spend more. He’s not in the White House; he’s not in the Treasury; and he’s not in Congress. He has nothing to do with fiscal policy. He’s playing with the only hand he was dealt: monetary policy. And in a balance sheet recession, that hand is impotent.

So at most, the Chairman is guilty only of creating irrational expectations. He’s the Wizard of Oz, but that steering wheel he’s spinning is not attached to the economy.

What QE comes down to, really, is a substitution of reserve deposits at the Fed in place of Treasuries and MBSs on the asset side of banks. In the case of Fed purchases of Treasuries, this reduces bank interest income—making them less profitable. Some held out the unjustifiable hope that less profits for banks would equate to more inducement to increase lending. Won’t work, and a bad idea even if it did.

We want banks to make good loans to willing and credit-worthy borrowers. We don’t want to make banks so desperate for profits that they make crazy loans (again!).

On the other hand there could be some benefits to banks that manage to unload trashy MBSs by selling them to the Fed. If you were a bank that was stuffed full of all the NINJA mortgages (no income, no job, no assets) made back in 2006, you’d be quite willing to sell those to the Fed—if the Chairman wants to play the role of dope, you’ll happily dupe him. I suspect that as a result of the bail-out plus three rounds of QE, a lot of the trash has been moved to the Fed’s balance sheet.

That’s good for banksters but it’s horrible public policy. Effectively the banks are moving sure losers off their balance sheets in order to get safe reserves that earn next to nothing. That’s a good trade! But, again, it doesn’t induce them to make more loans, does nothing to stimulate Main Street, and creates all sorts of moral hazard in the financial system. Uncle Ben has taught banks an invaluable lesson: too dumb to fail!

Let’s summarize QE this way. You have a checking account and a saving account at your bank. Your bank makes you an offer you cannot refuse to shift some funds from your saving account to your checking account. (Let us say they will give you a toaster as a reward—and you really like toasted bread.) Will this shift of funds induce you to run out and spend more? Probably not. Especially if you are worried about the future, your spouse was recently fired, and you are underwater in your mortgage. You might even spend a bit less because you earn less on interest in the checking account.

QE essentially amounts to shifting funds from a bank’s saving account at the Fed (Treasuries) to its checking account at the Fed (Reserves). It reduces bank earnings by a hundred or two basis points.

And that is supposed to simulate the economy?