Answer: The Fed, and e) 50% of its assets have ten years or more to maturity.

Recap. The GFC began about four years ago. The Fed pulled out all the stops to save the biggest banks. As I discussed previously (https://www.economonitor.com/lrwray/2012/02/16/let%e2%80%99s-make-a-deal-the-bail-out-of-wall-street-in-unusual-and-exigent-circumstances/) the Fed engaged in “deal-making” designed to protect creditors of failing banks, and used Section 13(3) to create Special Purpose Vehicles that engaged in legally questionable lending and asset purchases to save banks and shadow banks. Four years later, the Fed’s balance sheet is still humongous and it is even increasing its interventions in recent weeks through loans to foreign central banks.

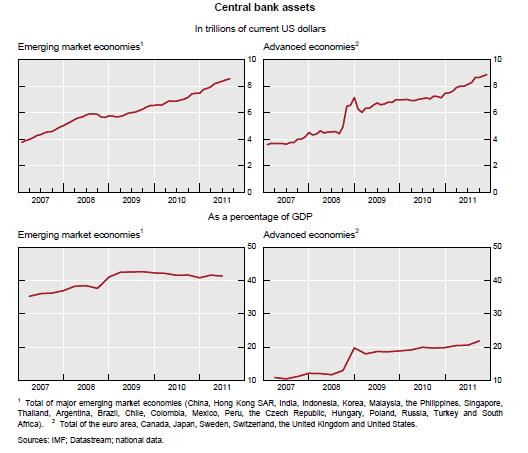

A recent speech by Herve Hannoun at the Bank for International Settlements, “Monetary policy in the crisis: testing the limits of monetary policy” (link below) shows that ramping up the role for central banks has taken place all over the world. Indeed, in emerging market economies, the central banks have assets equal to 40% of GDP. In large part that is due to accumulation of foreign currency reserves among countries like China and Brazil–a topic beyond the scope of this blog. But the intervention by central banks during this GFC is entirely unprecedented–and is starting to worry most observers, who are asking when, or if, this will ever end.

Graph 1: Central bank assets, and as a share of GDP

Graph 2: Maturity of assets

You can find the BIS report here: http://www.bis.org/speeches/sp120216.htm

To be sure, I do not share the worry of the BIS and many other commentators that the central bank expansions will cause inflation. My worry is this: the “too big to fail” (or as my colleague Bill Black calls them “systemically dangerous”) institutions have learned that no matter what they do, they will be saved and their top management will never be punished.

With the “deal-making” and “bail-out” approaches of the Fed and Treasury, it is unlikely that financial institutions have learned anything from the crisis—except that risky behavior will lead to a bail-out. In the Saving and Loan crisis of the 1980s, many institutions were shut down and resolved, and more than a thousand officers in top management served jail time. In the current crisis, no top officer has been prosecuted, much less jailed. Banks have been slapped on the wrists with some fines—usually without being forced to admit wrong-doing.

Critics like Walker Todd have long argued that continued expansion of government’s “safety net” to protect “too big to fail” institutions not only runs afoul of established legal tradition, but also produces perverse incentives and competitive advantages. The largest institutions enjoy “subsidized” interest rates—their uninsured liabilities have de facto protection because of the way the government (Fed, FDIC, OCC, and Treasury) props them up, eliminating risk of default on their liabilities (usually only stockholders lose). The “deal-making” approach described last week extended the principle of lender of last resort activities to entirely novel areas—protecting creditors of even shadow banks and, as discussed, favoring bond holders while forcing stockholders and securities holders (and defrauded homeowners) to take losses. As William Black argues, these SDIs are mostly run as “control frauds” to enrich top management. As long as they remain in business they destroy economic value—not just the capital value of the firm, but the financial and real wealth of the economy as a whole. Total financial losses that can be attributed to the GFC already exceed $10 trillion and will eventually sum to much more. And of course that does not include the “real” economic losses—nearly 10 million jobs in the US alone.

With all the government support most of the financial institutions have so far survived the crisis. While they are reluctant to quickly resume the practices that caused the crisis—subprime lending, securitization of junk assets—they did not suffer much from them. It is probable that if the economy and financial sector were to recover, risky practices would come back. Further, and more alarmingly, the financial sector bounced right back to taking 40% of corporate profits, to pay-outs of huge bonuses to top management and traders, and to accounting for 20% of value-added toward national GDP.

No significant financial reforms made it through Congress. All of this is in sharp contrast to the 1930s New Deal reform. Half of all banks failed that time around, and most of the survivors were taken-over by the government. Management was replaced. The Pecora Commission was given relative free-reign to investigate the causes of the crisis and to go after the crooks. Widespread defaults and bankruptcies wiped out a lot of the private sector’s debt. The financial sector was down-sized and rendered unimportant for several decades.

World War II led to budget deficits equal to 25% of GDP, and government debt grew much faster than income so that it flooded private portfolios with safe and liquid assets. The New Deal provided jobs and then a safety net for those who fell through the cracks of the “Golden Era” of US economic growth. The “managerial, welfare-state” version of capitalism emerged to replace finance capitalism. This time, after the GFC, we still have the modern version of finance capitalism—money manager capitalism–somewhat worse for the wear, but still pumping up commodities market bubbles and the stock market.

Over the past several decades, the financial sector taken as a whole moved into short-term finance of positions in assets. This is related to the transformation of investment banking partnerships that had a long-term interest in the well-being of their clients to publicly-held, pump-and-dump enterprises whose only interest is the well-being of top management. It also is related to the rise of shadow banks that appeared to offer deposit-like liabilities but without the protection of FDIC. It is related to the Greenspan “put” and the Bernanke “great moderation” that appeared to guarantee that all financial practices—no matter how crazily risky—would be backstopped by Uncle Sam. And it is related to very low overnight interest rate targets by the Fed (through to 2004) that made short-term finance cheap relative to longer-term finance.

As soon as some holders of these risky assets wondered whether they would be repaid, the whole house of cards collapsed. And that largely took the form of one financial institution refusing to “roll over” another financial institution’s short term IOUs. Four years and trillions of lost dollars of wealth later, we are still in crisis. Four years later the Fed is still lending and at “subsidized” (below market) interest rates.

The problem is that this “bail-out” validated the questionable, risky, and in some cases illegal activities of top management on Wall Street, those running the “control frauds” in the terminology of my colleague, Bill Black. And it moved the long term assets—including risky MBSs—onto the balance sheet of the Fed. Ironically, it is the Fed that now provides continuous short-term finance for banks so that they can resume leveraging into risky bets. And it is the Fed that holds the long term assets.

What should have been done? Bagehot’s recommendations are sound but must be amended. Any of the “too big to fail” financial institutions (what Black calls “systemically dangerous institutions”) that needed funding should have been required to submit to Fed oversight. Top management should have been required to submit resignations as a condition of lending (with the Fed or Treasury holding the letters until they could decide which should be accepted). The Attorney General’s office should have been called in to investigate all top management, to prosecute crimes, and to pursue jail time for convictions. Short-term lending against the best collateral should have been provided, at penalty rates. A comprehensive “cease and desist” order should have been enforced to stop all trading, all lending, all asset sales, and all bonus payments. The FDIC should have been called-in (in the case of institutions with insured deposits), but in any case the institutions should have been dissolved according to existing law: at least cost to Treasury and to avoid increasing concentration in the financial sector.

This would have left the financial system healthier and smaller; it would have avoided the moral hazard problem that has grown over the past three decades as each risky innovation was validated by a government-engineered rescue; and it would have reduced the influence that a handful of huge banks have over policy-makers in Washington.