The Central Bank of Turkey managed to surprise again by cutting its overnight lending rate, the ceiling of the interest rare corridor, a full one percentage point and not hiking reserve requirement ratios (RRRs). Of the 16economists surveyed by business channel CNBC-e, only 3 were expecting a cut, and all only 25bp. Similarly, only 2 were expecting no hikes to lira RRRs.

So what is going on? The answer is in the bank’s one-pager that comes with the rate decision and the accompanying statement on open market operations. The Bank’s actions are as mysterious and “unsurprisingly surprising:)” as in the last couple of months, so let me try to simplify things a bit:

1. The Bank is saying that while it hasn’t stopped, the music has certainly slowed down: “there is a deceleration in capital inflows in the recent period.” That’s why they feel they don’t need a wide interest rate corridor to battle excessive capital flows and are narrowing it.

2. The slowdown in music is also the reason why the RRRs were not hiked. Since credit (and growth) is closely linked to capital flows in Turkey, the Bank feels credit growth will slow down although it “has been hovering above the reference rates during the early months of the year amid strong capital inflows.”

3. In this environment, the Bank is opting to use the reserve options coefficients (ROCs) more actively, so they increased the ROCs in all tranches except the first by 0.1. Note that the cut in the overnight lending rate is in line with this move in the sense that if the rate banks borrow from the Central Bank (the overnight lending rate) is lower, they will have more incentive to use lira for required reserves when they need FX. Also note that according to the Bank’s statement regarding ROCs, they are utilized at 86 percent, which may explain why the lira has not weakened despite the turmoil of the last few days- i.e. banks have already made use of the mechanism a bit.

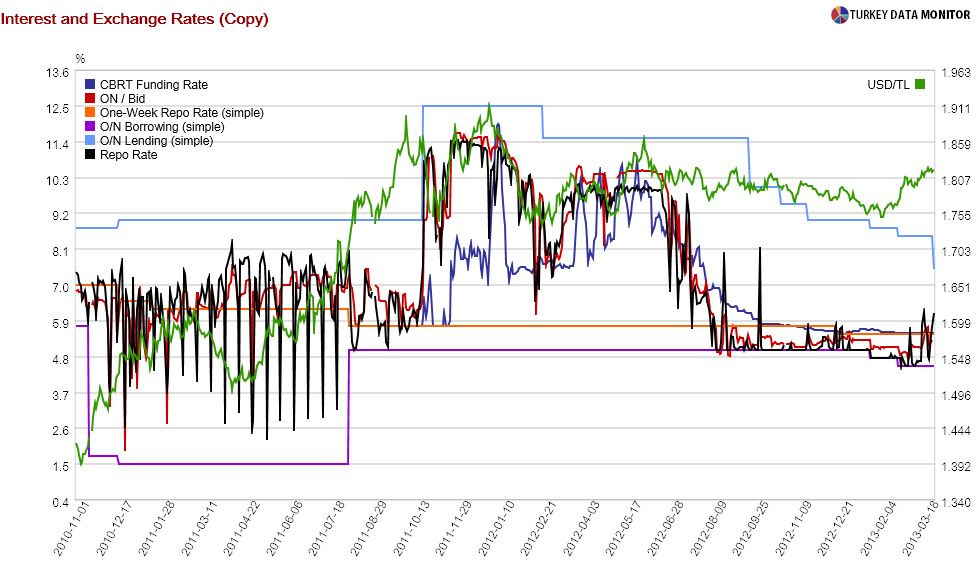

4. Liquidity Management is Back: Just like back in 2011, RRRs did not manage to slow down credit, as I was expecting: Lending rates have decreased this year so far despite the RRR hikes and loan growth has not slowed. While the Bank will leave some of the job to the slowdown in capital flows, by reducing one-month repo funding to TRY1bn from 2.5bn, they plan to make the banks more dependent on shorter (overnight and one-week) borrowing from the Central Bank. In fact, I believe they will also decrease one-week funding, and so banks will rely more on overnight lending. As a result, the markets rates (interbank, repo) will rise; overnight repo should apprroach 7 percent (lending rate for primary dealers) in the coming weeks. It is also important to note that the Bank has been tightening liquidity for a while: The liquidity provided by open markets operations has fallen from TRY 21bn to around 15bn in the past month or so.

5. Note that the Bank is more tolerant of commercial credit, and since the Bank claims the overnight lending rate effects commercial rates more than consumer rates, the cut is justified according to their thinking. I am getting rather hungry and Turkey is playing Hungary (no pun/ wordplay intended!) in World Cup qualifiers, and so I’ll just quote from my friend Ozlem from Ekspres Invest: “Commercial credit rates are at 10.5% as of March 15th,while the Deputy PM Governor stated that they should come down close to housing credits around 9.3%. The other reason is the commercial credit-deposit spread. The CBT has been aiming to lower the spread to below 4.5%, which is currently at around 4.7% in four-week moving average basis. The cut in the upper bound would push the spread to below threshold.”

6. Is the banking regulator (BRSA) not playing along? The reference to “macroprudential measures” for slowing down credit in the last statement has been dropped. This may simply be because the Bank will rely on the measures I mentioned above (slowdown in capital flows and liquidity management), but I still wonder- as I tend to believe the most effective way to deal with credit growth would be for the BRSA to enact higher provisioning for consumer lending.

My feel for all this: When you look at all the actions as a whole, and take it with the Bank’s assumption that capital flows are slowing / will slow down, the Bank’s action plan is at least internally consistent. My usual reservations on the effectiveness of this policy mix and its side effects (such as the inflation outlook -from the one-pager, the Bank seems less confident on inflation; moreover, in business channel Bloomberg HT’s quarterly survey released today, only one half of respondents believe the Central Bank cares about inflation sufficiently, compared to 75 percent last July- and the rise in short-term external debt of banks because of ROCs) remain. But all I’m saying is that there is a logical story going on here, as you can see from my explanations.

Finally, not much market reaction: The lira weakened initially and there was some inflow into the benchmark, but by market close, everything had returned to normal.

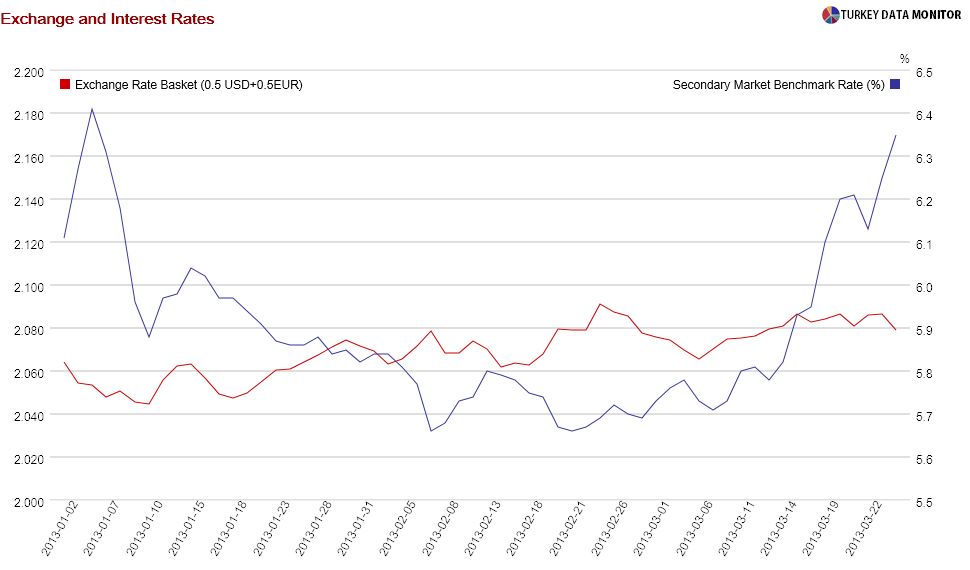

As you can see, the lira is stable, whereas the upward move in the benchmark is continuing…