That’s what the villain Auric Goldfinger tells 007 when the latter asks, “Do you expect me to talk?” in the Bond movie Goldfinger. This is exactly how I feel about Turkish bonds.

This is the intro. to my latest Hurriyet Daily News (HDN) column, where I argue that the ultra-low Turkish bond yields are not sustainable based on the economy’s fundamentals such as inflation and the monetary policy outlook and upcoming borrowing schedule. You can read the whole thing at the HDN website, but before I go further, I should be clear about what I mean by “to die”: I definitely don’t think the benchmark will hit double-digit territory, but I feel that 6.5-7 percent is more realistic.

Before I start with a lengthy addendum, I should report myself to the Turkish Capital Markets Board. As I detailed in my last post, this column of mine may count as market manipulation if Prime Minister Recep Tayyip Erdogan the Capital Markets Board chooses to do so. So I am in snitching on myself:)

Coming to more serious matters,a reader joked that I had put a disclaimer to the column with my last paragraph:

it will be real money flows into emerging markets, which amounted to a whopping $1.8 billion in the last four days, that will decide whether Mr. Bond dies soon or another day.

This may sound like a disclaimer, but we did see huge flows into emerging markets (EMs) bonds and equities last week– in fact, the biggest weekly real money inflows into bonds since Feb. 2012! Note that there was an even split between hard and local currency bonds- the flows into local currency funds were the largest since Aug. 2011. So it was definitely not just Turkey. For example, investors seemed hungry at last Thursday’s Hungary (sorry for the lame wordplay) auction as well. You can read more about this hunt for yield in the latest weekend Wall Street Journal (WSJ). Another WSJ article argues that the same hunt for yield has caused a corporate bond boom.

But there is reason to be worried. For one thing, this central-bank based party will not last forever; that was in essence Mohamed El-Erian’s point I referred to in the article. And blogger Tyler Durden at Zero Hedge notes that “it is starting to feel a lot like 2007“, which was one of El-Erian’s main points as well. But El-Erian adds that the current situation is less risky, as it was created by central, not investment banks. However, you should remember the party will not go on forever, as the the Fed FOMC minutes and the Jan. 10 ECB rates meeting/Dragbi comments hinted. A related issue is whether the risk on-risk off environment will continue, and for that, I would recommend the FT Alphaville blog post on the topic. Another interesting side point is Nomura’s observation that extreme moves like last week’s are usually a contrarian indicator…

Perhaps, despite the flows into EMs like there is no tomorrow, or tomorrow never dies to continue with my Bond references, investors are already taking an eventual central bank unwinding into consideration. You can get some insight by looking at different types of Turkish bonds. First of all, Deutsche notes that there was more demand for the front end of the curve than the back end at last week’s auctions. Other then valuation reasons, they note that “market participants (especially local banks and fast money accounts) might have been weary of the risk of another sell off in UST (which caused many EMEA curves to bear steepen last Friday) and therefore preferred exposure to the frontend and belly of the bond curve”. This is related to the El-Erian point as well. A bond trader friend told me that the 10-year is being sold by foreigners this week, so there may be some truth to this explanation. But of course, the alternative explanation for this steepening of the yield curve could be better growth expectations for this year, but 2013 growth expectations fell to 4.2 from 4.4 percent in the Central Bank’s latest expectations survey, which was released yesterday.

Speaking of the specifics of Turkish bonds, I find inflation linkers quite interesting. Not that I take the break-even inflation of 5.5 percent or so implied by these bonds very seriously. But I am more interested in the fact that there has been quite a bit of demand for those this week. This may because markets may be expecting inflation to go up, as I wrote in the column. But that should have been clear after the December inflation was released. Anyway, Citi analysts make a strong case for linkers in their latest bond markets round-up as well.

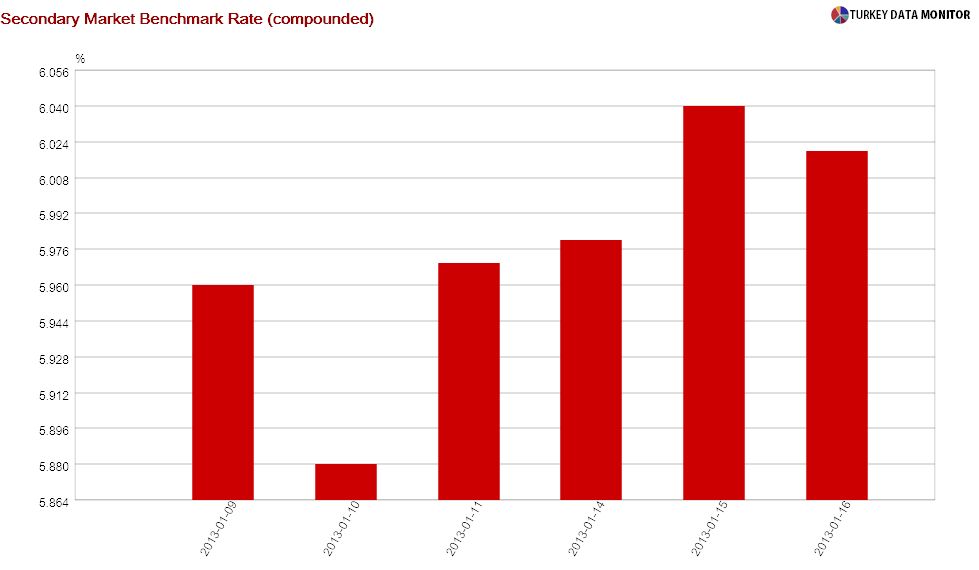

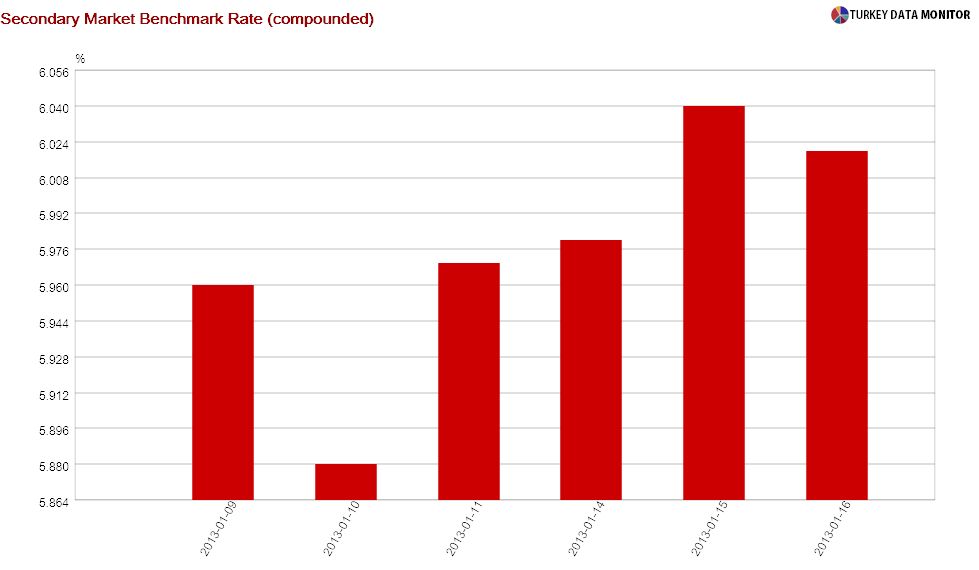

By the way, I wrote the column on Thursday (for Friday’s HDN). How did my prediction fare since then? Here’s how the new benchmark has been doing since its inauguration last Wednesday:

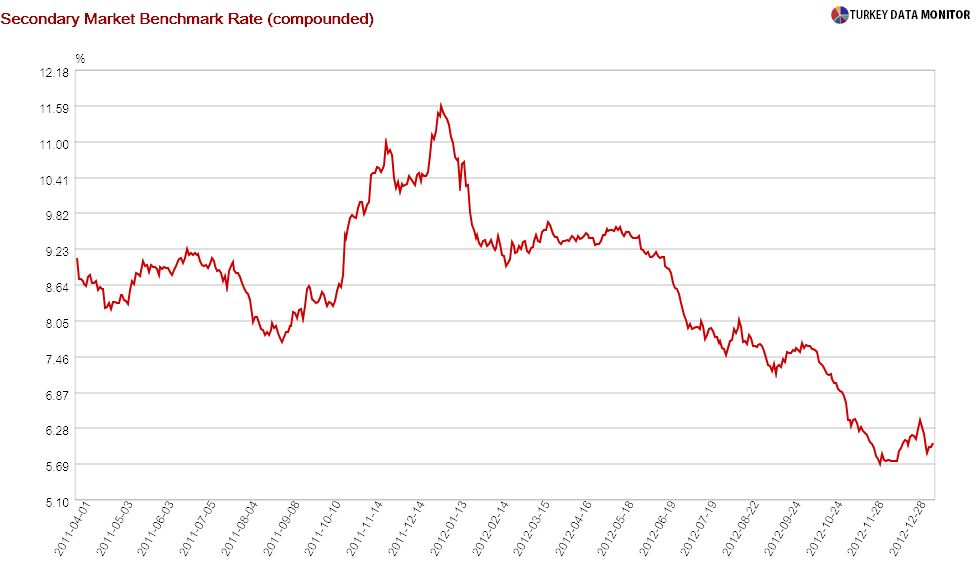

There has been only a minor rise in benchmark yields since I wrote the column, but I wasn’t expecting an immediate correction anyway. Speaking of predictions, I noticed, after writing the column, that I had written another column with the same title back in April 2011, as a response to the strong rally in bonds early in that month. Let’s see how I fared that time:

As you can see, I was right on target, at least initially: The benchmark started creeping up soon after I wrote the column, and after hitting 9 percent, hovered there for most of the summer. The rally eventually came back with a vengeance in August, but the Central Bank lowered the policy rate unexpectedly at the time, and that is cheating:)

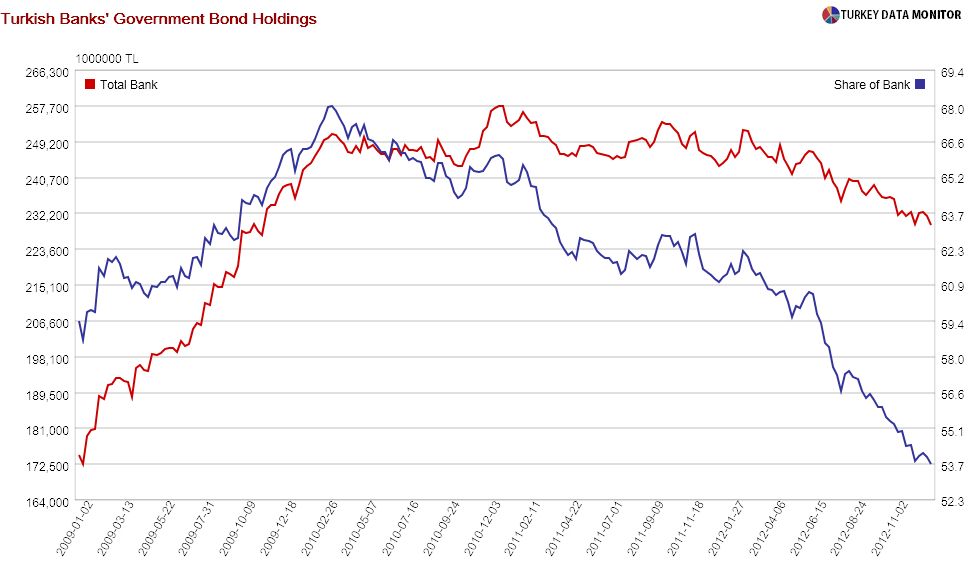

Returning to last Friday’s column, let me make one clarification: Whenever I link inflation to bond yields, someone is bound to comment that foreigners don’t care about inflation. First of all, despite the strong foreign flows of late, quite a big chunk of Turkish bonds are still owned by domestic banks.

But even foreigners would care about inflation if it causes monetary policy to tighten and if it causes the currency to depreciate. The latter is why foreigners would care about not only inflation but also inflation expectations.

Finally, just as an update, the strong demand for Turkish bonds continued in yesterday’s last auction of the month. Here’s my friend Ozlem Derici from Ekspres Invest, who summarized not only the auction but also the month’s borrowing by the Treasury:

Demand was again strong in the auction with 4.5x higher bids than the offer while average yield at 6.2% fell short of market consensus around 6.26%. Treasury completed its monthly borrowing program by selling TL11.3bn, of which TL9bn was to market. This is slightly lower than its projection of TL11.6bn, of which TL9.7bn was from market. Thanks to lower than projected borrowing, monthly rollover ratio stood at 86.7%, lower than the initially planned 89.2%. Note that annual target for domestic debt rollover ratio is 87.5%. There is only slight ease in benchmark bond yield from 6.05% to 6.03% following the auction

I really don’t think this trend will continue, especially with the continuation of the heavy supply schedule in the next couple of months. If nothing else, the primary dealers will have to offload some bonds ahead of the auctions even if you ignore the fundamentals I mention in the column. We’ll see…