I started the year at Hurriyet Daily News (HDN) with a column on Turkish monetary policy, and out of the 63 columns I wrote this year, 18 were directly on monetary policy. Therefore, is only appropriate I end the year with a column on Turkish monetary policy.

During his presentation of the bank’s 2013 Monetary and Exchange Rate Policy on Dec. 25, Gov. Erdem Başçı noted that “short-term capital flows could disrupt price and financial stability by causing excess volatility in lending and exchange rates.” Therefore, the bank would not allow sharp moves in either. In Friday’s column (you can read the whole thing at the HDN website), I argue that this new target does not make sense: The market and academic economists I talked to are not aware of any theoretical link between the volatility in credit growth or exchange rates.

The academic economists I talked are the two of the best young (below 40) academics in Turkey. They both specialize in monetary economics and also have central banking experience, either as full-time staff or adviser. So they know what they are talking about, and they are both sure a theoretical paper showing the link does not exist. They noted that there could some empirical paper they don’t know about, but with voodoo econometrics, you can show anything: As I often say, I could probably establish a link between rainy days in Istanbul and Turkish equity performance. So I wouldn’t (and more importantly they wouldn’t either) take seriously any empirical work on the relationship that is not published in a serious journal.

One of the academics, as well as Murat Ucer of GlobalSource and Turkey Data Monitor, a well-respected Turkish macroeconomist who knows a thing or two about Turkish monetary policy, noted that I may be misreading the Bank. They both noted that the Central Bank may have been referring to big swings when they talk about volatility. But they have talked about big swings in the past, and they never used the v-word. In any case, I translated what they said word by word above, so you can decide for yourselves.

There is also some uncertainty on whether the Bank had the nominal or real exchange rate in mind when it talked about volatility. In the Governor’s presentation, where I took the text I translated, “exchange rates” were mentioned, which implied they had nominal the FX in mind. But in his speech, Basci mentioned real exchange rates, and all of the analysts / columnists assumed the Bank had real FX in mind. I’d expect a little bit of caution from the Central Bank in their annual Monetary and Exchange Rate Policy presentation!

But I don’t want to get stuck with technicalities and details. What I was trying to say in this column was more general than credit/FX volatility and inflation. I tried to make two much broader points. First, this is not the first time the Central Bank has made ambitious statements without any evidence. Most recently, they had the same problem with Reserve Option Coefficients, a new tool the Bank introduced recently. Second, if the Bank really abandoned inflation targeting, as many analysts believe, they should just admit it. It looks kind of awkward when they try to make all these new instruments, such as volatility targeting, as part of inflation targeting. It also makes me feel that I, along with all the Turkey economists, am being treated like an idiot by the Central Bank:(

I have a small anecdote for this second point: At the Q&A session after Basci’s presentation, Kerim Karakaya of Bloomberg HT asked Basci whether the Bank would officially abandon inflation targeting since it had effectively done so. Basci said they were still targeting inflation, but that their policy was called modern inflation targeting:) Anyway, Karakaya had been warned: Radikal columnist Ugur Gurses had advised him not to ask questions he would not get answers to:)…

I am aware I did not spend much time, either here or at the column, on what the Bank’s actual 2013 Monetary and FX strategy would be. For that, I would like to refer you to the excellent notes by Ata Investment and Turkish bank TEB (sub. of BNP Paribas) and move on.

Istanbul think-tank BETAM organized a panel entitled Understanding the Central Bank on Wednesday, the day after the Bank revealed its 2013 strategy. The panelists were Hakan Kara, the chief economist of the Bank, Murat Ucer, to whom I referred to above, Bilgi University professor Asaf Savas Akat and Yapi Kredi chief economist Cevdet Akcay. This was a very good mix: Kara is the best person to give the official view of the Bank, Ucer is a critique who thinks along the same lines as your friendly neighborhood economist and Akcay is a harsh critique those like Ucer and your friendly neighborhood economist. If you speak Turkish, you can reach the presentations at the BETAM website, but if you don’t your friendly neighborhood economist summarized the key points of the panel- as much as could be done withing the confines of 3000 characters, or 500 words- in his Hurriyet Daily News column today.

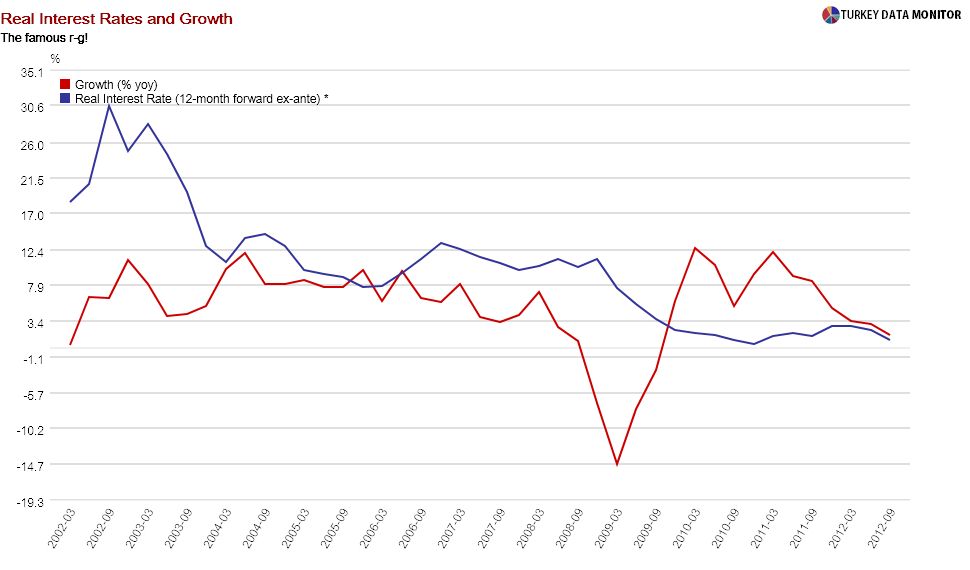

I have quite a few additional points to make. First, a careful reader may note, after looking at the sole graph in my column, that the Bank has now been controlling both interest and exchange rates of late. That is an illusion created by the strong capital flows of late, as Ucer noted.

Another important point from the panel is with regards to debt sustainability: As all students of economics learn at some point, if you’d like to reduce your debt, you need real rates less than growth, which happened for the first time for Turkey in the global crisis, as interest rates fell sharply, thanks to the Bank’s sharp rate cuts.

Although I am critical of the Bank’s policies in the last two years, I applaud their ahead-of-the-curve cuts in 2009, which allowed a negative r-g for the first time.

And finally here a couple of sentences by Murat Ucer (in Turkey Data Monitor) on what Akat and Akcay talked about:

Asaf Savaş Akat did not make a formal presentation. His talk focused on the exchange rate, arguing that current account debates should always include the real exchange rate, whereas in Turkey it typically doesn’t. Among other issues, Cevdet Akçay, who also didn’t have a formal presentation, complained about the perception and quality gaps between market analysts and CBT, arguing that the former can’t keep up with the latter.

Last but not definitely not the least, I would like to thank BETAM for sending me the video recording of the panel through wetransfer.com. Hakan Kara’s presentation at the beginning wasn’t there, and the recording did not include the Q&A session, but I nevertheless used it a lot.