The International Monetary Fund (IMF) released its Article IV consultation report for Turkey late Dec. 21. These documents are scrutinized by Turkish policymakers before publication. However, reading between the lines can still reveal a lot about where the Fund and the government differ on economic policy.

Here’s the intro. to my latest Hurriyet Daily News (HDN) column, where I summarize the IMF’s (not to be confused with the Impossible Missions Force, sorry for the lame joke in the title) Article IV reports on Turkey. In fact, I concentrate more on the accompanying Selected Issues paper, which is like a background paper for the Staff Report, but the topics discussed there have their special boxes in the Staff Report and are mentioned throughout the Report as well. Anyway, you can read the whole thing at the HDN website.

Since I had to summarize 100 pages or so into 500 words, I have quite a bit of additional points to make, but before that I should note that the column is a very very selective summary- I chose 3-4 different topics and concentrated on those. I wanted to go for the most interesting topics, and those where there was a significant difference of opinion between the Fund and the government- it is my journalistic instinct to go for the controversy:). What I am trying to tell is that there is much more to the Report and the Selected Issues paper than my column, and it is not technical at all, and so I would highly recommend anyone following the Turkish economy to read it.

You may be wondering how I know what government officials think. Of course, I have my little Ankara birdie, which could sneak into the Treasury and the Central Bank:), but there are two legit ways of getting the scoop as well: First, if you’ve read these types of IMF documents, you know that you know:) when government officials disagree with the Fund- after the Fund explains its position, it also reveals the opposing view of the government- they naturally don’t do this for every view, just for the ones they differ. And second, and this one is my little secret, go to the very end of the pack (linked in the column), and you’ll see the statement of the Executive Director for Turkey- this is as close to the government’s position as you can get.

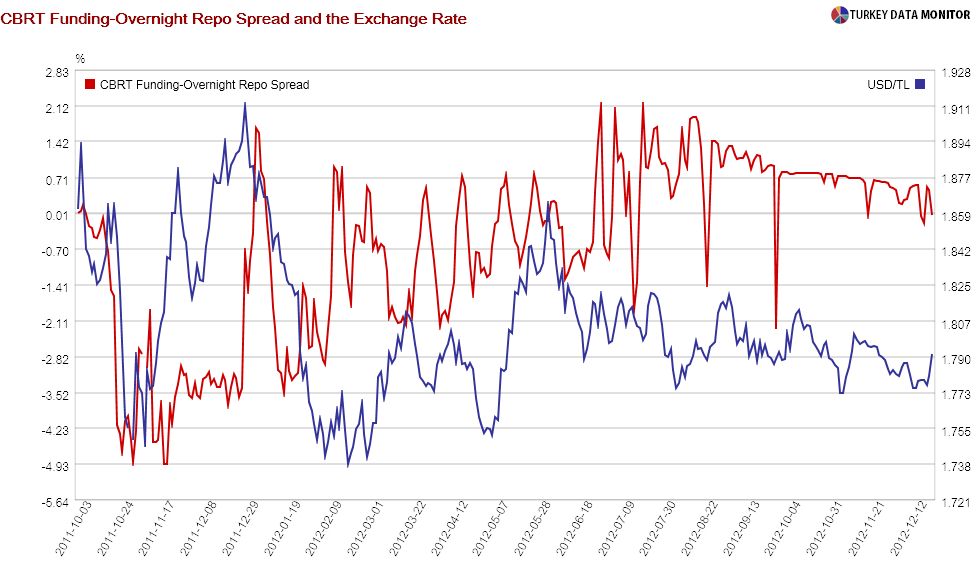

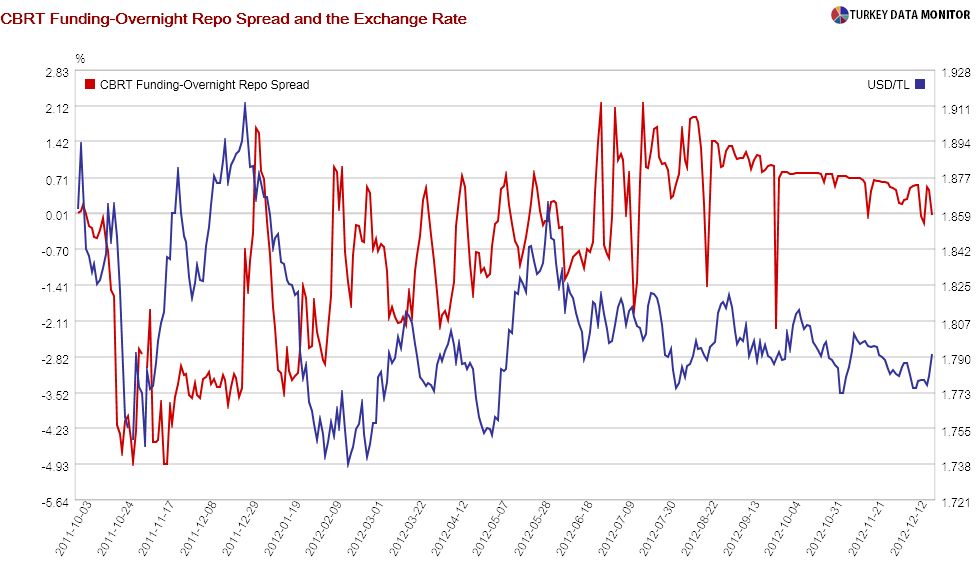

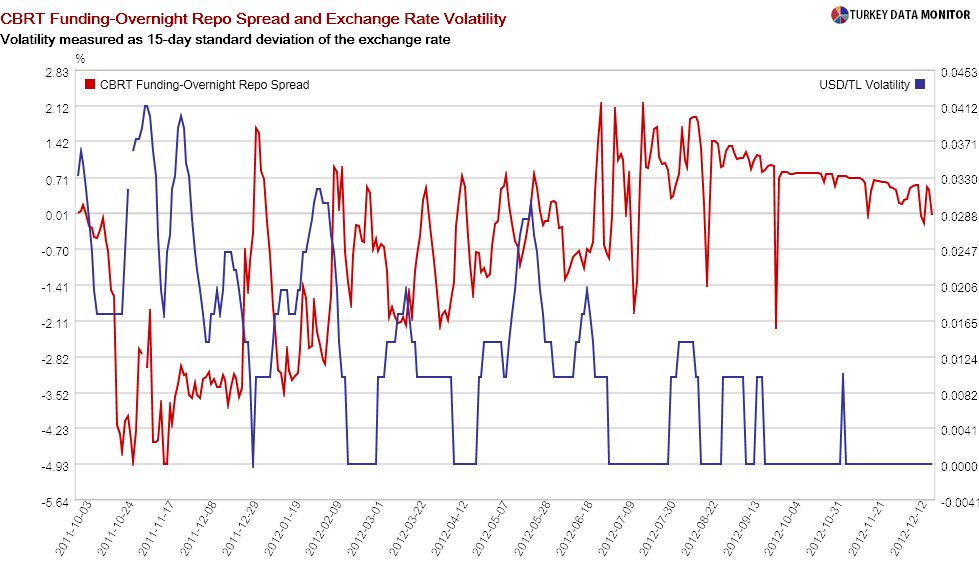

Anyway, now I have got rid of the formalities, I can get on with the addendum. I’ll start with the monetary transmission mechanism. Robert Tchaidze, the author of the monetary policy chapter in Selected Issues, uses quite a novel approach to show that the monetary transmission mechanism has weakened. First, he looks at the spread between the Central Bank’s effective funding rate and the level of the exchange rate…

….and its volatility

You can easily the see that the spread has become higher and more volatile this year after the introduction of the new framework. This should not be a huge shocker; that is one of the goals of the Bank’s framework, after all. As for its relation with FX, I’ll quote from the IMF:

Examining the behavior of the spreads suggests that the behavior of the spread is linked to the strength of capital inflows, which manifest itself in the level and volatility of the nominal exchange rate: when the exchange rate is stable, the spread declines; but with volatile or appreciated exchange rate and low effective rates, the spreads widen, suggesting that markets expect the exchange rate to depreciate and/or the effective rates to tighten

Note that the data for the paper is from late-summer; these relationships have somewhat weakened since then, but it is still quite a compelling idea- I wish we had enough data to test it.

As for the other point on inflation expectations I mention in the column: Until the Central Bank started this unconventional policy, inflation expectations used to be affected by the Bank’s inflation target and actual inflation- which means the Bank had some credibility, but that there was also some adaptive expectations going on. But what the Selected Issues chapter as well as others (Citi economists and the OECD for example) have shown is that right now expectations don’t respond to either- nor do they respond to anything else! Of course, the Bank chooses the benevolent interpreration that expectations have become well-anchored. OK, but the anchor is quite a bit above the Bank’s inflation target:)…

Finally, a couple of words on the bank’s “stable exchange rate policy”: It looks like a great idea, right? At least until you notice that once exchange rate targeting takes precedence over inflation targeting, as may be happening in Turkey- in addition to the “hard” evidence I summarized above, the Fund also provides some anecdotal evidence on this. Then, it will be a no-brainer for a company to borrow in FX, as I explained in a previous HDN column. A stable exchange rate could also attract hot money, as the Fund is noting. Yet another distortion created by the the Bank’s policy framework…

OK, this is more or less what I had in mind for an addendum. However, a reader asked about the sources of disagreement between the Fund and the IMF: What are deeper assumptions underpinning CB approach?

I think I explained the the Fund’s reservations really well and so partly answered this question. On the other hand, the Bank thinks it has to care about financial stability as well, and that inflation targeting is not the best too to maintain both price and financial stability. The Fund agrees on the importance of financial stability- it just doesn’t see the merits of the Bank’s approach over a more traditional policy framework.

Yet another difference between the Bank and the Fund is on Turkey potential output/growth. Historically (I don’t mean 2 millennia ago), the issue was whether the economy was overheating in 2011. The Fund thought so, the Bank didn’t. Of course, this was an important issue, as overheating would mean the Bank would have to raise rates. Incidentally, that “incident” is mentioned in box in the Staff Report. More importantly, it makes a difference whether Turkey will be above or below capacity next year. Again, the Fund is saying 4 percent growth next year could result in a positive output gap, but the government and the Central Bank don’t think so. That’s why they are less worried about the current account deficit and inflation than the Fund…