Another guest post from Ali G (not the rapper– sorry for the bad joke, but I am just preparing you for Monday’s column). Small edits here and there, I don’t touch the style, just minor grammar stuff… And my comments are at the very bottom…

CBRT ended the latest special days streak as of 18th of April. The market seems to be convinced that the CBRT has set an implicit rate target at 2.10 for a 50% USD 50% EUR basket against the Lira. On the other hand, Governor Erdem Başçı firmly rejects that they’re targeting the exchange rate.

I believe exchange rate targeting has become even more dangerous these days if you are not PBOC with trillions of dollars of reserves. Even the Swiss National Bank’s target has been frequently questioned, but it seems to hold for the time being. So, although speculative action may be limited during these uncertain times, I don’t believe the CBRT would take the risk. Let’s face it albeit having a nice symbol; the TRL does not have the deepest market. In short, I don’t think CBRT has an absolute target.

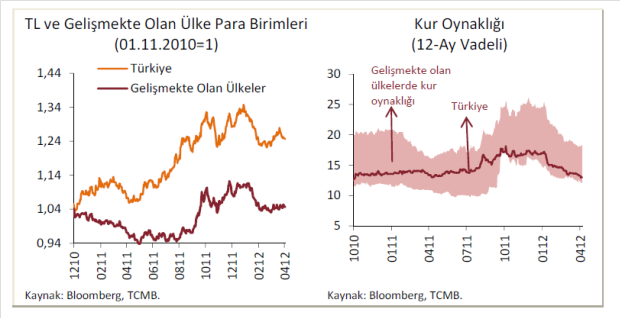

The Bank has been using a lovely set of graphs in its presentations since December. The figures given below are taken from the President’s 80th general assembly opening speech. The figure on the left shows the relative performance of the TRL(orange) and other EM currencies against the dollar. The one on the right shows 1 year vols of USDTRY and the range of EM volatilities. First of all these graphs show that the CBRT is concerned about where the TRL is relative to its peers. Secondly the Bank was emphasizing that they were targeting the volatility of the lira with FX interventions during 2011. Looking at the graph, it seems that they have done a good job.

What I’ve said so far is one, the Bank has relative measures and two it is targeting volatility. With that in mind, I’ll elaborate on the last two special day streaks. I believe the first one in March started on the 22nd and ended on the 29th and the second one started on the 11th of April and ended on the 18th. The first figure shows the performance of peer currencies against the USD. Here we observe that the relative currency level performance level argument works for the March streak, but it does not seem to hold for the April streak.

The second graph below shows the 1 month implied option vols of USD/TRL and other peer currencies against the USD. Here we observe that although in absolute terms TRL vols are low, there are two periods where the TRL vols move against its peers or jump considerably more. These two periods match the two special day streaks so far.

In conclusion, although there are not enough observations to formally check it, a significant upward movement of relative TRL volatility seems to mark a special day streak. I may be wrong, but this seems much more plausible to me than an absolute rate target. It’s just food for thought.

Ali Gökhan is the acting economist at a Turkish conglomerate. The views expressed here are his personal views only and do not represent the views of his company.

OK, I wanted to push Ali’s point further, so I did some regressions (yeah, baby!). Specifically, I took the data in figures 2 and 3 (thanks Ali) and replicated the methodology of Citi Turkey economists. I did not have CDS, as they did, but my controls were lira’s relative level and volatility performance (compared to the other four in Ali’s list). Interestingly enough, 2.07 and 2.12 came out as threshold levels (as determined by R^2 of the regressions) when I used just the level as well as both the level and the volatility.

I am now in the process of doing regular VARs using the same variables: The funding rate, the level and volatility of the exchange as well as the relative performance of both variables with respect to the same four peers. I hope to have some results on this as well as more complete results of the former exercise early next week, but if you just can’t wait, have a look at the earlier Citi note, where they do a similar exercise, but by using open market operations (OMOs) rather than the funding rate.