Who said economists can’t have fun:

As loyal readers would know, I have been a staunch critic of Turkish monetary policy. But some key events last week have lifted this veil of ignorance and made me reconsider my position.

Here’s the intro. to my column that was published on April 1 . You can read the whole thing over at the Huriyet Daily News web site. The reason I bolded the publishing date, as well as the title, will be revealed at the very end- and so will the first sentence of this post:)

Turning to more serious matters, despite being two weeks old, the column is not really out of date, and despite the fact that March inflation was released and the April rate-setting meeting took place in the meantime…

I briefly discussed March inflation in an earlier post. As for yesterday’s Monetary Policy Committee meeting, it is officially saying what we already knew: That “exceptional days” will become more common, in a sense unexceptional:)… So markets really have to be on edge all the time, waiting for their funding costs to go up any day? Or should they really?

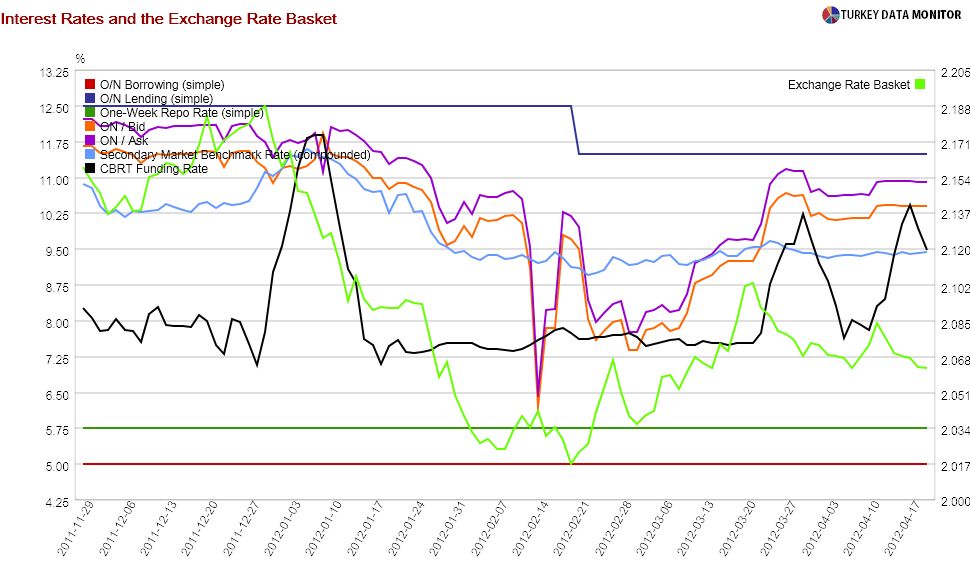

As I was noting here at the blog a couple of days ago, markets think that the Central Bank intervenes in the exchange rate by tightening liquidity and increasing funding costs whenever the exchange rate basket hits a certain threshold. I won’t argue whether they are right or wrong; for one thing, I’d need to do some simple metrics to reach an opinion, which I plan to do for a future column or post. But once markets’ expectations are anchored on the exchange rate, you as a Central Bank are really in a shitload (pardon my French) of trouble. I think this is the main risk of this policy…

BTW, in case you are a follower of the maxim, “a picture is worth more than a thousand words”, here is the summary of my previous 100 words, if not 1000:

As you can see, the funding rate is not really extremely volatile; it suddenly spikes whenever the Central Bank feels the need to raise it, for whatever the reason…