Yes, yes I will come to yesterday’s Central Bank of Turkey direct intervention, but I have a few things to say on the tax hikes and the Medium-Term Program, or MTP, as sort of a complement to Monday’s Hurriyet Daily News column, which was also posted here at the blog.

Let’s start with the tax hikes. Finance Minister Mehmet Simsek presented them as “price updating”, which drew a lot of criticism. In his defense, the Finance Minister meant to say that some of the taxes on alcohol and tobacco are fixed, and that they required updating to make sure revenues do not decrease in real terms. The mentioned price hikes are on the order of 7 to 10 percent, which is line with end-year inflation.

But as Ugur Gurses was arguing in his Radikal column today, such behavior would create a vicious circle, as inflation is a result of government policy, and the tax hikes are enforcing higher inflation into people’s expectations. And one thing the government could not take into consideration is the fact that firms do not update their prices incrementally and all the time, and Phillip Morris ended up doing a huge price increase, which was followed by other companies as well. So the government ended up with an MTP whose forecasts (or at least one of them) was quickest to be proven wrong: There is no way end-year inflation will be 7.8 percent, as projected in the MTP.

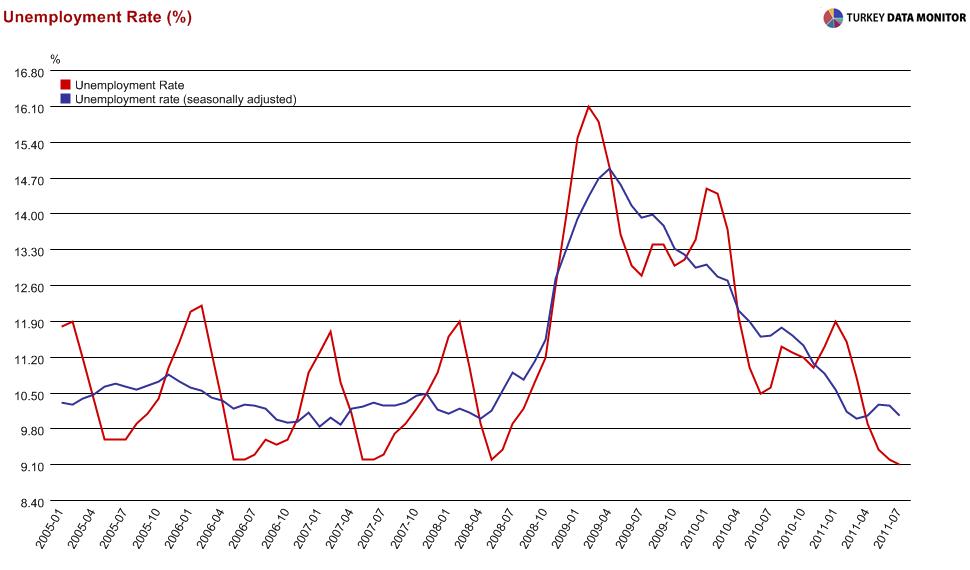

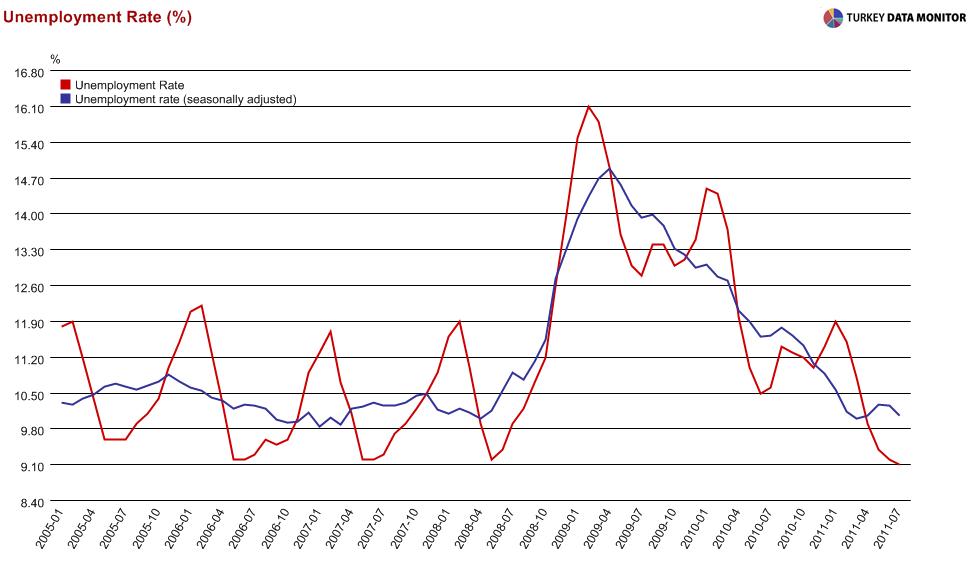

BTW, the MTP is not the only entity that lost face. Right after I claimed that the MTP’s 2012 unemployment projection of 10.4 percent was a bit low, the July figure (actually, average of June-August) came in at 9.1 percent:

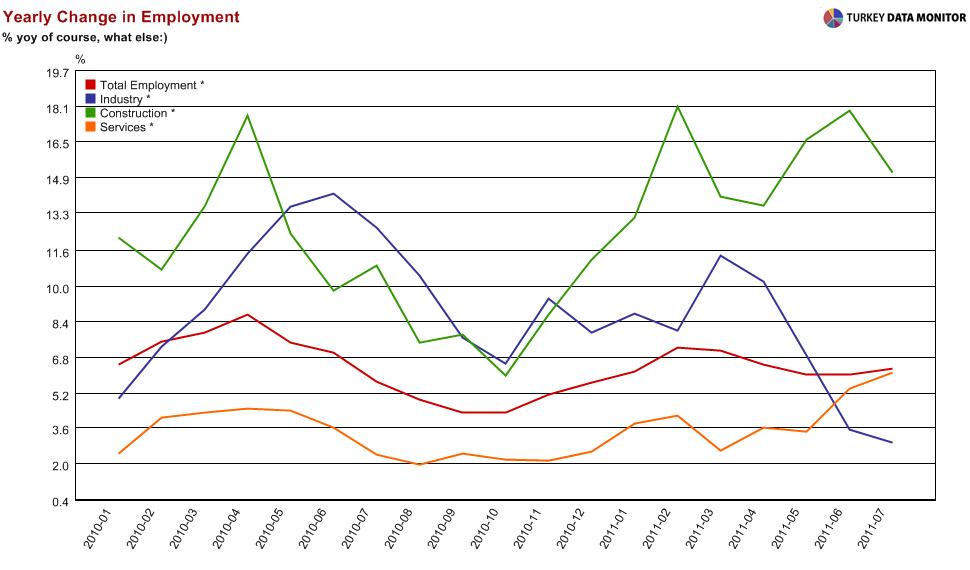

Is this yet another dent to my poor forecasting track record? Luckily, it is not so simple: For one thing, unemployment is extremely seasonal in Turkey, reaching yearly lows in the summer before climbing up rapidly in the fall and winter. Secondly, the increase is mainly coming from services and construction, as well as some decrease in the labor force:

All in all, the latest employment figures are not easy to interpret, as Seyfettin Gursel argues his Radikal column today. One interesting observation he makes is the possibility of an increase in the sensitivity of employment and unemployment to growth, which could be due to the 5 percent decrease in the unemployment insurance as well as other employment incentives. This is certainly a point for further discussion.

Before moving on, there is one final point I would like to make with respect to taxes. As Yapi Kredi research argues in their latest weekly, indirect taxes are distortionary and so are not preferred by economists, unlike there is some negative externality, which is certainly the case in alcohol and tobacco, but even then finding incentives to encourage people not to smoke is a better solution (no wonder my editor hates the long Turkish sentences, to which this last sentence owes its existence). Unfortunately, the share of indirect taxes is extremely high in Turkey, mainly because of the huge tax evasion and grey economy, as I had argued back in April.

Turning to the MTP, it is appropriate to start with inflation. If Turkey manages to grow 4 percent next year, I am not sure how inflation would stay at 5.2 percent. Understandably, the government could not come up with inflation projections other than the Central Bank’s, and it would have been damaging to credibility for the CBT to give up its 2012 targets so early- even though missing another year would be damaging to credibility, as Iceland Central external MPC member Anne Sibert was discussing at the IFS conference in Istanbul last month.

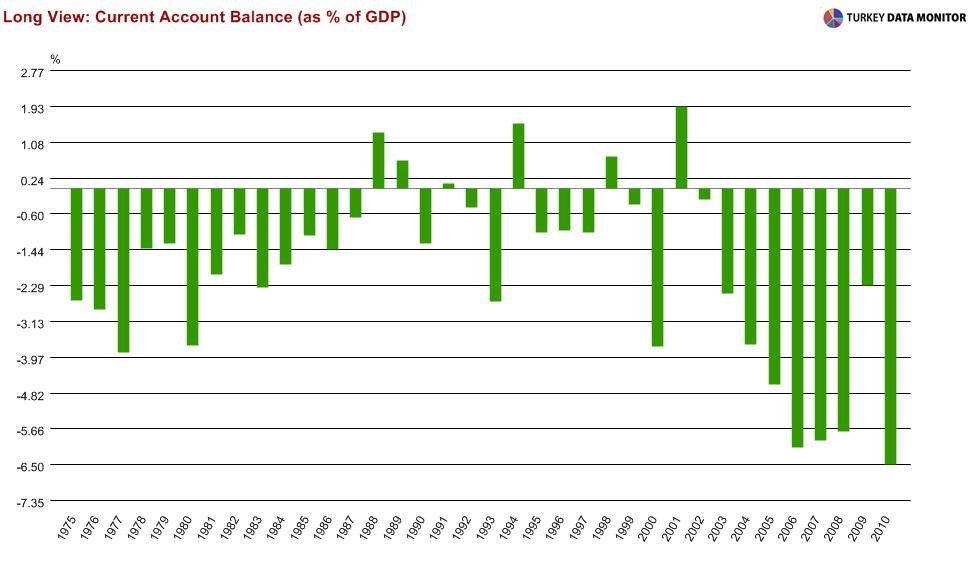

Another question mark is on the current account. The government is basically saying, “We are going to live with a high current account, let’s hope we don’t get a sudden stop”. It is useful to put this approach into perspective. As Fatih Ozatay argues in his latest Radikal column (you probably know by now my favorite Turkish daily), Turkey has never been able to sustain large current account deficits for so long, which is certainly a cause for concern.

Then, there is the real exchange rate: The government is foreseeing real exchange rate appreciation for the next three years. Then, the question is how the current account deficit would adjust without any support from the exchange rate. I would argue that the exchange rate is only a temporary fix anyway, but we are not seeing a lot of development on reforms, which could reduce the current account structurally. The much-awaited input supply strategy, to be announced in the next few days, might convince me (application is another matter, but nevertheless) if it contained effective measures to support domestic intermediate goods production.

But the MTP hints the government is not very hopeful on the reform agenda, either:) Think about it: All those lists of reforms, and the current account only goes down 1.4 percent:) You could argue that it would take the government some time to implement all those reforms, but most of the things on the agenda are not that time-consuming and besides, there is plenty of time until the end of next year.

Besides, I am not for such extensive reform agendas, which have the look of having been written after an extensive literature review by a couple of junior analysts at the Development Ministry (the institution previously known as the State Planning Organization, as evident from their English web site). Such grocery (laundry) lists, prepared without taking into consideration binding constraints and the biggest bang for the buck, are bound to fail. The government made that mistake with the Strategy and Action Plan for the Istanbul Finance Center project, and it is doing it again. To say the same thing differently, to quote Murat Ucer of GlobalSource and Turkey Data Monitor, “there is no vision” in the MTP.

It is also useful to compare the MTP with the Central Bank of Turkey’s outlook. The big difference between the two is growth. While the CBT does not reveal its output gap estimates, let alone its growth projections, Governor Erdem Basci has been communicating the Bank’s worries of a significant slowdown, mainly based on the global economy, for quite some time now. That is certainly not the MTP scenario, although any forecast is endogenous to policy, i.e. it includes the policy response.

Last but not the least, there is fiscal policy: I was shocked when most analysts deemed the fiscal stance as positive.I am not saying the fiscal genie is out of the box, but the budget is certainly not designed to address the current account deficit. And that’s why the current account deficit doesn’t come down in the government’s MTP projections!

Now you now why an economist who thinks along my lines said that reading remarks like “honest, realistic and internally consistent” for the MTP “sucks worse than a Bulgarian pornstar”!:) I am not that knowledgeable about Bulgarian pornstars, but here is what Atilla Yesilada, of GlobalSource/Istanbul Analytics and Ekonomi Haber Yorum (very useful web site on the Turkish economy and markets if you speak the language) has to say on the positive sentiment towards the MTP:

This is true in the sense of the following example: A panel of medical experts tells a patient that he is morbidly obese and should immediately start a rigorous diet program. After much introspection, the patient calls back to say that he agrees with the diagnosis, but his family was fat, too, and he shall continue to chow down burgers and pizzas all day, thus his weight shall not vary much after the new diet.

Speaking of Turkey analysts, their Turkey bullishness and willingness to accept whatever the Central Bank tells warrants a separate post, as this one is already turning out to be too long, but here’s an excerpt from a recent (well-written and objective, so definitely worth reading) Financial Times article on the Turkish economy:

Some analysts, who prefer not to be quoted, argue that the bank’s insistence on low interest rates mirrors Mr Erdogan’s desire to keep the economy roaring ahead.

Hmmm… I wonder why they would prefer not to be quoted:) But this means that some of the jesters in the court are actually doubters in disguise, or closet-doubters:)

Joking aside, at the end of the day, the government and the Central Bank are going for the very dangerous path of foregoing inflation and the current account in favor of growth, as I was discussing in the column. As a result, I believe that Turkey has turned into a high-beta play. If the plans to save, or at least prolong the suffering of, the Euro Area go through, the economy will be fine, and you’ll see a revival in Turkish assets (and many articles, not only from the likes of Suluman the Economist and Brave Cloud but also from the many market economists applauding the ingenious Central Bank), and I’ll have to put another dent to my poor forecast track record yet again. But if the Euro Area problems linger on and risk aversion continues, Turkey (and Turkish assets) is one of the most vulnerable countries out there.

And to think that the Central Bank’s ingenious policies were implemented to protect the country against Euro Area problems and a major global slowdown. In retrospect, they saw the picture earlier and better than anyone else, with the exception of my host here Nouriel Roubini and a few others, but their response was wrong! In their defense, you could argue, as Murat Ucer did at the ERF Monetary Policy Conference a couple of weeks ago, that the CBT had to respond, with inappropriate tools, because no one else (banking regulator and the government in particular) was willing to.

But that doesn’t take us out of the predicament we are now in:(…