As a result of my meetings and sightseeing, I have been neglecting the blog. I have a couple of hours before my morning London Walks tour, so I just wanted to do the delayed addendum to Monday’s column. Since some of the recent data releases are directly related to the column, this will also be one of the traditional Turkish economy data & news wrap-up pieces.

First, Governor Basci spoke to two TV channels on Monday; you probably saw my liveblogging. Basci said really important things, like rates were more likely to be cut whether there was a global crisis or recovery on the horizon. You can read the details at my post, but my impression is that Basci did a rather good job explaining himself, or rather the Bank’s policies, which is good news for someone very critical of the Bank’s communication policies like me.

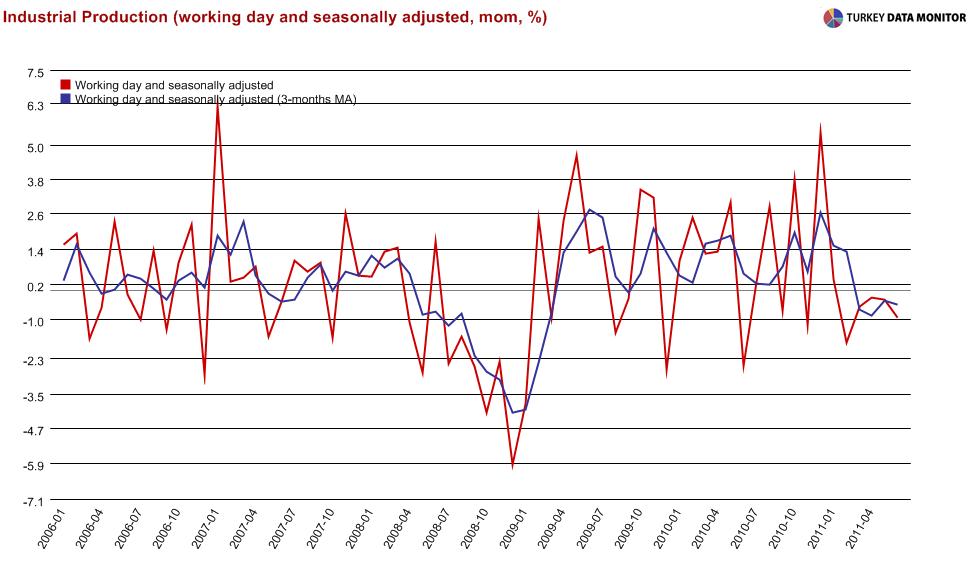

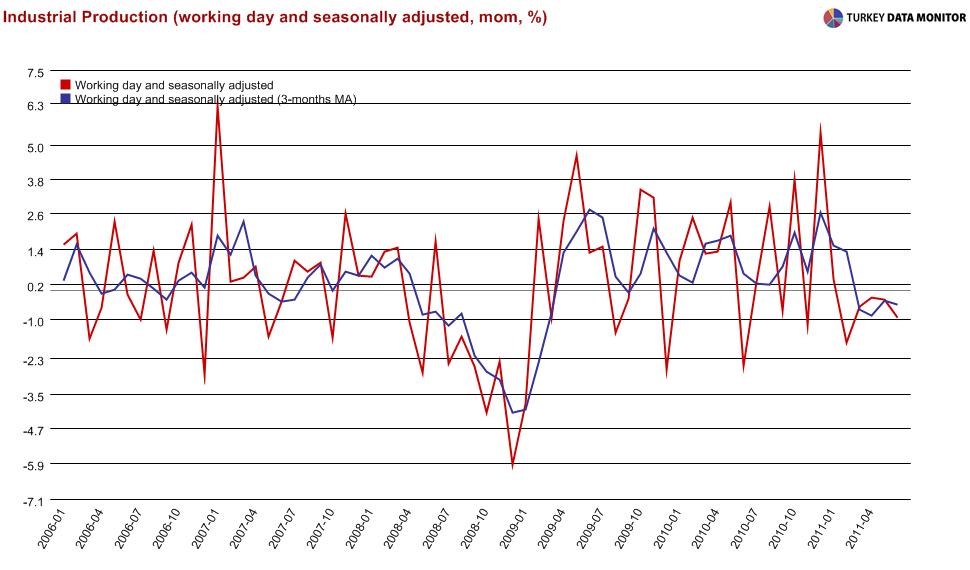

Having said that, some of what he said is open to interpretation, and recent data are painting a mixed picture. Industrial production continues to point to moderation in economic activity, and it now seems that the Central Bank’s projection of 0 percent seasonally-adjusted quarterly growth, with which I agreed, might have been overly optimistic:

Put these figures into a simple model, and you get a slightly negative quarterly growth. BTW, have a look at the Citi note if you want the full details. BTWW, for those of you who have asked me why I always use Citi notes: They are one of the research houses I trust, but they are they are the only ones who provide hyperlinks for their pieces. I mean, if I really want for you to read a particular piece, I’ll share it via SugarSync, but there is no need to go the extra distance if all reports are more or less saying the same thing…

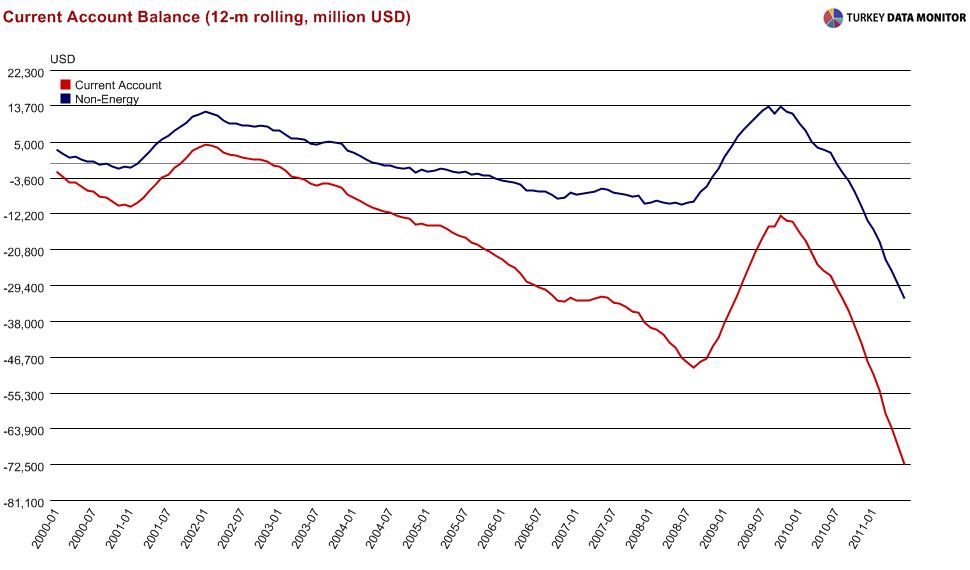

Coming back to the matter at hand, on the other hand, the current account deficit is already over USD 70bn, which was Basci’s end-year projection on the TV (the first time the CBT gave current account forecasts):

Basci again seems to have “verbally intervened” after the high current account deficit release: According to my economist friends in Istanbul, he just stated that the deficit would be USD 5bn in July. I am not sure what data they used to make that forecast, as the public figures are not available yet (I would need VAT on imports and tourist arrivals figures), but I hope he is right. If he misses by a large margin, there will be further loss of credibility, though. But I am sure he knows this, so he wouldn’t be making this statement unless he were sure.

But more worrying is the global picture. In that respect, I find Citi’s title for the current account research note very appropriate. As their last two graphs illustrate (I know, I know correlation is not causation, but please take my word on this), the Turkish growth model is dependent on external financing, which in turn depends on global risk appetite. With such a large current account deficit/ financing need, this will be the Democles’ sword over the country’s head.

But worry no more: The government solved the current account deficit problem at the Economy Coordination Committee meeting this week. Here’s my friend Ozlem taking of Erste securities taking over:

Those include strengthening the fiscal position, improving investment environment, following policies that support employment increase, fighting against unregistered economy, decisively implementing privatization program, completing export oriented production strategy, input procurement strategy and works on differentiating export markets, speeding up the works on making the Istanbul an international finance center and effectively implement to R&D projects. All those will be included in the 2012‐2014 Medium Term Program which is expected to be announced next month.

We’ll see if there is any truth to the fiscal policy remedy at next month’s MTP, but for the others, we just have to wait and see. These are long-term measures, and even if they are in the MTP, we have to see if they will be implemented. BTW, I recently wrote about the Istanbul Finance Center project yet again, this time as part of a book, which will be distributed at the G-20 meetings in Istanbul in November. While I am not allowed to share my article, note that Babacan has disclosed that a large Omnibus Law that will address many issues towards carving a finance center out of Istanbul will be passed by the end of the year.

I have digressed way too much… Coming back to Basci’s speech, I am more worried on what he did not say rather than what he said. For example, as a recent UBS note illustrates, Turkey looks like the first emerging market to have raised rates rather than cut them. That’s why markets are skeptical of the Bank’s policies, and the opposition CHP has used the opportunity to bash the government– you don’t see them talking much about the economy, but I guess they just couldn’t pass on the opportunity:)…

Please note that at this point, the argument is not one of economics, but one of PR: The Central Bank might be right, although it is as easy to make a case for interest rate hikes as cuts. But since you are doing something argauably controversial, you need to do your best at communication. A regular reader, who is “critical” of my “critical” economic policy-making views, has been noting, as comments to my columns that Basci is a genius and that I should have faith. It really doesn’t matter if I keep the faith or not; it is the hedge funds and the like the Bank needs to worry about. If the Bank convinces them, Emre Deliveli’s whines will be like a mosquito’s whizzing.

Just to illustrate: The same reader is aware that the CBT is supporting the lira, and I think he is not an economist/finance professional. So if the CBT is arguing that they cut FX required reserves ratios to increase the maturity of FX deposits, they are taking us for an idiot. Or worse still, they are being very very stupid, at least according to a famous American philosopher.

But communication is an issue with the government as well. Different ministers have been contradicting each other. For example, according to the PM and Economy Minister Caglayan, the crisis will not even pass tangent to Turkey, whereas Babacan is more cautious. And speaking of the economy tzar, he seems to have just said that more measures to curb lending are on the agenda- I think he has the “independent” banking regulator in mind, but I would have found it much more comical if he were talking about the Central Bank:)

I wanted to talk about the Central Bank’s measures from a liquidity perspective as well, but this post is already way too long, so I’ll do that when I come back from my sightseeing tonight.