Here’ s what was left out of today’s Hurriyet column, which was also posted at the blog.

The Usual Suspects

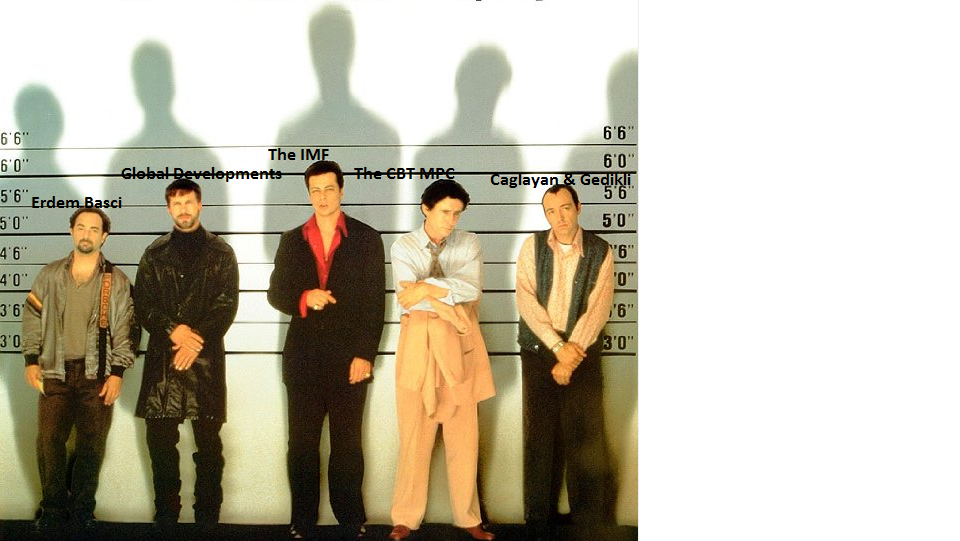

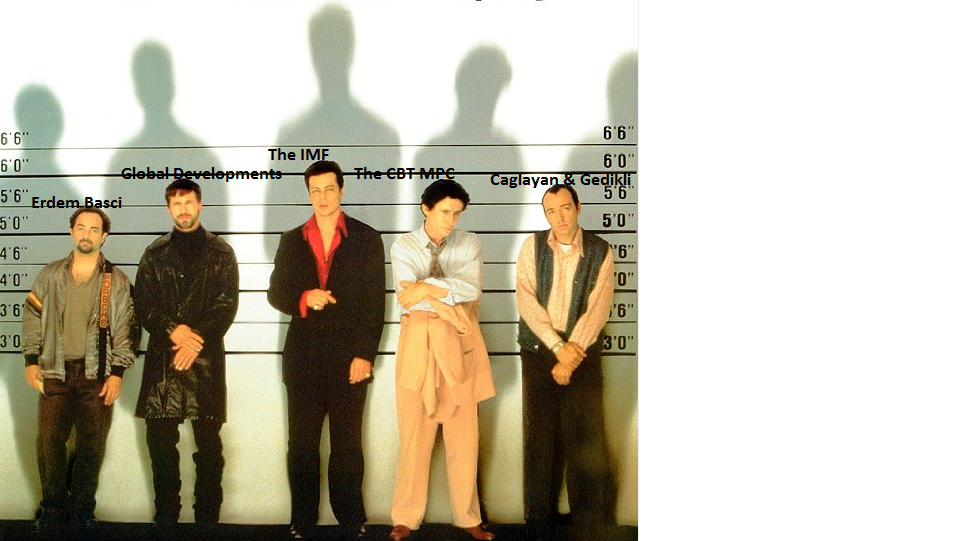

First, let’s start with who the usual suspects are, i.e. who rattled Turkish markets last week:

- The IMF: All the IMF-related events were detailed in the column.

- Global Developments: It is natural that Turkish assets are being affected by the U.S. debt ceiling and Euro Area debt issues. While these could account for some of the lira weakness today, neither issue was a factor last Thursday or Friday.

- Fitch: As mentioned in the column, Fitch issue a warning on Turkey’s current account deficit last week, but as I note there, it was the IMF paper rather than Fitch that affected Turkish markets on Thursday.

- The Central Bank Monetary Policy Committee: You could also argue that the tone of the MPC last week was deemed too dovish by markets.

- Erdem Basci: As I note in the column, CBT’s Governor Basci’s comments on open positions (not particular for Turkey) were interpreted as the CBT warning against a looming currency depreciation. Also, Basci was interpreted (I won’t say “sounded” because he did not sound like that to me at all) as saying that the Bank was comfortable about the lira.

- Government officials: I think the star was Zafer Caglayan, saying first that the current account in not a problem, and then responding to Fitch’s warnings as “Fitch has become a Fitch again”- Turkish speakers would know that replacing “f” with “p” would result in a word sounding like “bastard” in Turkish- that’s a wordplay even I wouldn’t dare. The papers are reporting Caglayan saying today that he has thrown the word “crisis” down the drain. Such ostrich mentality won’t help a bit, but neither will AKP topbrass Bulent Gedikli’s remarks warning consumers to save and not to consume.

So, here’s my take on the usual suspects:

As at the end of the column, you can see who I think the real guilty is…

The IMF G20 Report

While I concentrated on the IMF G20 report’s Turkey projections at the column, the report has other goodies on the Turkish economy: The fund notes that cyclically-adjusted balances are still negative in a number of economies (e.g. Brazil, India, and Turkey), even though demand is at or above capacity. In these emerging markets, the task is to avoid overheating and prevent the build-up of financial imbalances. Therefore, in these countries, there is room for further consolidation. This will take pressure off monetary and prudential policies and create fiscal space to respond to future shocks.

There is nothing radical in these remarks, except that statements like these were probably the reasons the ill-fated IMF Staff Report never made it to the public So the Fund has in fact releases the Staff Report:)

So the Fund has in fact releases the Staff Report:)

BTW, the IMF’s Turkey projections did not come from their multi-country models, as some Turkey economists were claiming; they came from the Fund’s Turkey desk. A multi-country model would never come up with such an accurate picture of the economy in the short-run (i.e. this year and the next) anyway.

BTWW, Roubini’s David Rogovic discusses the projections and the Turkey-related parts of the report at a recent blog post.

The Turkish Banking Sector

I explained in the column that Turkish banking vulnerabilities in the IMF Euro Area spillover paper were blown way out of proportion. Markets chose to concentrate on one single chart among 50, one that was a simple exercise utilizing one Turkish bank, as I note in the column.

But that’s not to say that that Turkish banks are immune from Euro Area woes. For one thing, Greek banks’ Turkish subsidiaries could be affected, but I think the worst that could happen would be change of ownership, as any cash/ transfers, interbank lending and the like would have to go through the banking regulator. Moreover, Turkish banks have almost no exposure to Greece.

But the more imminent danger is foreign funding for Turkish banks. The big chunk of the syndicated loans mature in the last quarter of the year, so if there are ongoing problems at the time, Turkish banks could face rollover difficulties. But who knows how the global environment will look like then?

A Couple of words on markets & traders

So if the IMF report was not really pointing to dangers in Turkish banking, how come markets became so jittery. Two observations are in order: 1. Your average trader will not spend an hour (or even a minute) reading the report; by then, it will be too late. He will (I will not retort to my usual “she” here, as we are talking about testosterone-packing traders) shoot first and ask questions later. Besides, as I note at the end of the column, once markets are unsettled by all these scary remarks coming from government officials, they will react at the smallest sign of trouble, whether it be a chart in a paper, a misquoted IMF rep or a misunderstood Central Bank president…