“Deflation is like cholesterol”, Economy Minister Luis De Guindos told CNBC at the WEF in Davos, “There are two kinds…..The bad one and the good one. In Spain, you know, we have the good kind,” So appealing was the story he told I’m surprised many of those in his audience didn’t immediately get on a plane to visit the country to try to discover what the secret was. After all, sounds like the next best thing to a free lunch. Wouldn’t anyone want some of that?

Or again, we have Bloomberg’s Maria Tadeo, who temptingly informed her readers last week that “Madrid is ready to party again”. “A strengthening economy and a pickup in consumer spending,” she said, “are energizing nightlife in the Spanish capital after a perfect storm of record unemployment, tax increases and a smoking ban put more than 400 venues out of business since 2008.”

“Madrid is a great place to be,” said Javier Bordas, owner of Opium, which he plans to open seven days a week. “You’ve got the football players, celebrities, and people love to party. We’re optimistic.”

It makes you wonder why on earth support for the radical Podemos party is surging at the polls. Surely there must be a catch here somewhere?

{kind=link}

Of course, Maria is only covering a story, an upside-bullish Spain-recovery one, and she does point out that Spain’s 23.7% unemployment rate is the second highest in Europe after Greece, but still, it couldn’t be that all the intense talking-up of Spain’s recovery in domestic demand is also helping to sell some of that 3.34 billion Euros worth of retail commercial property that went under the hammer in 2014, now could it?

Certainly the story must be a lot more palatable to the clique of property consultants who are currently doing the selling than it is to one of the 4 million Spaniards currently on the credit blacklist run by credit consulting firm ASNEF, who normally can’t get hold of credit under any circumstances and will have a hard time joining in the current consumer “boom” even if they have a job. Spain’s Economy minister Luis De Guindos put it even more graphically:

“It’s hard not to defer purchases when you’ve got no money for them in

the first place. In the case of Spanish unemployed I think they’ve got

more worries than waiting for a new sofa suite to drop by €50.”

Nor is the “good deflation” argument especially convincing to anyone with sufficient economic common sense to understand that deflation in a heavily indebted economy can NEVER be unequivocally “good”. I doubt there are too many mortgage holders out there busily applauding the ongoing fall in house prices.

If there is such a thing as “good deflation” it surely comes from falling prices in the wake of productivity gains rather than from “downward stickiness” in wages and pensions. But this is not the Spanish case since employment is growing faster than output. Spain’s economy grew by 1.4% during 2014, yet employment was up 2.5%, suggesting that labour productivity actually fell during the year. So Spain’s drift downward in prices is being fueled more by a demand shortfall than by supply side improvement: it’s hard to see what is so “good” about that.

My intention here, however, is not to argue that Spain’s economic recovery has been hopelessly one

sided, which it has, but rather to try and pick my way through the

ideologically-loaded minefield of arguments which are currently being

advanced about the significance and meaning of the deflation phenomenon in Spain.

So, Is Deflation A Problem?

“Deflation is a protracted fall in prices across different commodities, sectors and countries. In other words, it is a generalised protracted fall in prices, with self-fulfilling expectations. Therefore, it has explosive downward dynamics.” – Mario Draghi

One of the reasons the arrival of deflation in Spain has generated so much controversy, I think, is that many doubt the country is actually suffering the phenomenon at all (see Bank of Spain Governor Mario Linde, “deflation risk in Spain continues to be low – November 2014 – or Economy Minister Luis De Guindos, “Spain is not at risk of sliding into deflation” – December 2014). Beyond policy makers and those whose job it is to “talk up” the Spanish recovery there is also little perception that it is a real issue, possibly because many have come to doubt so many of the things the administration says that they aren’t even sure yet prices are falling. Beyond petrol and house prices the fall is so small it’s not easy to perceive, especially when reductions are not shown in the form of like for like changes, but in the form of more complex “offer” and “discounts”.

In fact statistics show that consumer prices were down in January by 1.5% over January 2014, while the GDP deflator for the whole of 2014 (the figure that is used to estimate the impact of inflation on overall output) was estimated at minus 0.7%, meaning that the inflation corrected rise in GDP of 1.4% was only half that number, so, statistically speaking at least, it is important.

But beyond those who simply – perhaps for definitional reasons – doubt that Spain is experiencing deflation rather than simple disinflation there are those who doubt falling prices really constitute a problem. This is the so-called “good deflation” argument. The FT’s Tobias Buck sums up many of the arguments in his article “Spanish Consumers Defy Deflationary Gloom“,and economist/blogger Shaun Richards has a more theoretical version of the argument here.

The gist of the “good deflation” case is pretty simple: on the one hand countries like Spain need falling prices and some kind of “internal devaluation” in their ongoing attempt to restore international competitiveness, and on the other consumers aren’t “so” rational as to engage in long and complex calculations across infinite time just to work out whether it is better to purchase now-or-later products whose price is falling by only 1% a year.

At this point it is perhaps worth noting what Mario Draghi says deflation is. Deflation, he tells us, “is a generalised protracted fall in prices, accompanied by self fulfilling expectations which has explosive downward dynamics“.

Well in this sense little in the way of conclusions can be drawn from Spain’s initial contact with falling prices, since hasn’t been that protracted (yet) and certainly has not developed self-fulfilling expectations: most people in Spain regard the situation as transitory. The self fulfilling part of the definition relates to the possibility of a downward wage-price spiral which mirrors the kind of spiral we see under inflationary dynamics but in the opposite direction. As prices fall, then wage reductions can be offered – as we have seen in Japan – to maintain real wages constant and these wage cuts then fuel further drops in prices. None of this is very evident in Spain so far, even if wages have fallen at some points in the crisis, and with this being election year, the process is unlikely to take hold in 2015.

As for the “explosive dynamics”, I presume the explosive part refers to the impact of a wage price downward spiral on debt affordability, since debt to income ratios are constantly pushed up.

The idea that economies move into an outright contraction spiral simply because a small fall in prices is repeated over a number of years is a curious one, whose origin isn’t clear, and whose reality is to some extent denied – as FT Alphaville’s Matthew Klein points out in a post entitled “Did Japan Actually Lose Any Decades” – by the fact that Japan’s economy is widely believed to have performed “tolerably well” all through the deflation years, with weaker consumption growth being more due to declining population (a problem which may also affect Spain in the future) than it is to a supposed phenomenon of “purchase postponement”. It’s only when you start to look at Japan’s 245% debt to GDP level that you get to see where there might be a problem.

Even in the case of technological products, where price falls are constant and significant, people seem more likely to look for a combination of price and performance, since improvements are ongoing and unending, yet people do buy.

So if people are largely agreed that small but constant price falls don’t, in and of themselves, produce widespread purchase postponement, and recognize in addition that Spain needs weaker inflation than Germany, then, you might ask yourself, why on earth are policymakers worried by the phenomenon? Yet worried about it they are, since if they weren’t why would the German government be acquiescing in sovereign bond purchases at the ECB (which in principle it is opposed to) to try to stop it digging in for the long haul?

Assuming you don’t write this institutional concern off as yet another example of things only economists worry about, and go on to ask the question you are likely to encounter three basic explanations: i) not all price falls are small, ii) there is an interest rate impact and iii) those who are burdened by debts become even more burdened as time passes.

Purchase Postponement in Housing

Spanish housing offers us a clear example of something whose price has fallen considerably, around 40% since the 2007 peak, and whose price continues to fall (currently in the 3% to 5% per annum range).

Far from this fall in prices having stimulated demand – the deflation “consumption boom” argument – we are witnessing exactly the opposite effect: demand has collapsed, and is not recovering significantly (see my piece from April 2014, “Firmly Anchored Expectations, No Postponement of Purchases?“). This is not surprising, since housing is a special sort of good (combining both use and investment) and the market is one where price movements tend to be self re-inforcing.

The Spanish housing market is still far from functioning normally – the number of new houses purchased in December was just over 7,000 – the lowest monthly level in more than a decade.

True, the number of second hand houses being purchased is rising, but even the combined total is far from showing a sharp rebound.

Perhaps the most worrying thing about the fact that second hand purchases are improving while new ones aren’t is that part of the explanation for this is that properties become reclassified as “used” 2 years after completion (so some of the second hand houses being sold are in fact new), but this makes the situation with new houses deeply preoccupying, since there are more than half a million unsold housing units still classified as “new” (see this article on the Spanish property website Idealista) which means they have been built within the last two years.

The problem with the arrival of deflation in Spain is this is going to create an environment where it becomes even more difficult for the housing market to really recover. In the meantime, constantly falling prices have had one consequence: Spaniards now prefer renting to buying, they have become more aware of the risk involved in owning a property. So perhaps rather than simple purchase postponement process what we should be looking for are a broader set of behavioral changes over the longer term.

In any event, given the importance of the Spanish housing market to the economy in general – 75% of the country’s household wealth is tied up in property – the situation cannot be ignored: ending deflation in Spain would help push house price movements back into positive territory, and in so doing would give a significant boost to the Spanish economy.

Then There Are Borrowing Costs

Moving beyond the issue of the supposed “purchase displacement effect”, Mario Draghi has a rather more powerful argument: the interest rate impact. Consumption growth in modern economies is as much about credit as it is about spending from current income. Too many people are still thinking about economic dynamics in terms of confidence and money stored under the mattress, or as some whit of a Bloomberg journalist put it, burying it beneath bathroom tiles. Credit matters to modern economies, as we have seen during the recent “credit crunch”. As consumer credit accelerates, economies grow, and normally when this happens central bankers started raising interest rates to slow credit growth. In general I think it is fair to say that those who think there is “good deflation” in Spain and those who think Spanish deflation is “not so good” agree about this.

Yet credit, curiously, is all about the temporal displacement of purchases. When credit is cheap, and inflation is expected to be present, consumers tend to advance purchases. I don’t know whether anyone wants to challenge this, but it is the cornerstone of any kind of interest rate policy. It is what gives the central bank, under normal conditions, the ability to apply counter cyclical policies in the face of recession. If this mechanism doesn’t work, then there is a problem in the whole way we have been thinking about things.

Once interest rates reach the zero bound (I think it is impossible to separate discussion of deflation from the issues which arise in the context of a zero bound) then this mechanism hits a limiting factor, since while prices are in negative territory conventional central banking theory makes bankers reluctant to follow by taking interest rates even deeper into negative territory (although, it should be said, we are now increasingly seeing the negative nominal interest rate phenomenon in countries like Sweden, Denmark and Switzerland). As Mario Draghi put it answering questions at the ECBs December 2014 press conference:

“Now, let me make absolutely clear that we won’t tolerate prolonged deviations from price stability, and the main reason is that if these deviations feed into inflation expectations, they’ll cause a drop on medium to long-term inflation expectations, which by the way still are within a range consistent with medium-term price stability. But if these were to feed into inflation expectations, these lower outcomes of inflation, were to feed into lower inflation expectations, we would have a zero lower-bound nominal interest rate. This would be tantamount to an increase in the real interest rate.”

Here we find some key word expressions: prolonged deviations from price stability, lower long-term inflation expectations, increase in real interest rate. This situation is rather different from the one described by the Spanish economist Javier Andrés in the Tobias Buck article I mentioned earlier: “The fall in prices”, Andrés argued, ” is not strong enough, nor is it perceived to last that long, as to make it worthwhile for consumers to postpone the purchase of goods.” In Spain at the moment the deviations from price stability have not been strong enough or perceived to have lasted long enough to have an impact on consumer expectations.

In fact deflation has been settling in for a lot longer than people in Spain think it has. Many still believe that the recent negative inflation is simply the result of a negative oil price shock, but if we look at the EU HICP rate excluding energy it is clear that the deflation issue started a lot earlier.

Another issue which has clouded the Spain deflation issue has been the use of consumption tax increases as a deficit reduction measure.The national statistics office maintain an ex-tax estimated EU HICP inflation rate, rather like the one the Bank of Japan maintains following the consumption tax rise in that country. Obviously if you raise a consumption tax you raise inflation, but this kind of inflation is not thought to be positive (as we are seeing in Japan, the country fell back into recession after the increase) as it weakens consumption (as the various VAT rises have in Spain).

The ex-tax consumer price index tries to estimate underlying inflation without the tax, and – as the chart below reveals – if we use that measure Spain has been hovering in deflation territory since late 2012. However Spain’s citizens seem to have a kind of “inflation bias” after many years of highish inflation, and simply refuse to believe that prices really have started falling.

In fact if we now adjust that earlier HICP excluding energy data and produce a constant tax version, we get a chart which looks like this.

This suggests that Spain has been near to deflation ever since the global financial crisis struck, but that the initial recovery produced an inflation surge as wages and prices across the economy reacted upwards (price rigidity, things going back to normal in terms of expectations). Now that shock has passed and the underlying trend towards deflation becomes obvious.

Mr Draghi is worried (although NOT Mr Linde, or Mr De Guindos, as we have seen) that if the current trend is not corrected Spain’s citizens might eventually begin to believe and expect it, which is why he gives more importance to the issue and is taking measures accordingly. Indeed, such is the importance which EU – as compared to Spanish – policymakers give to the issue they are taking the measures even though their mere announcement has started causing a great deal of difficulty for central banks in countries like Switzerland, Sweden and Denmark. Again, it is noteworthy how by and large these central bankers are accepting such difficulties without protesting too much since they understand why Mario Draghi feels forced to implement them.

Mario Draghi argues that falling inflation expectations raise real interest rates by influencing the perceived cost of credit into the future. If consumers anticipate inflation, then that makes borrowing cheaper and people tend to advance purchases. Conversely expected price falls make the cost of borrowing greater, make the desirability of advancing purchases via credit less, and in this sense constitute monetary tightening. I am aware of an ongoing debate about whether interest rates really are a key factor influencing investment decisions, but I have never seen an argument suggesting that the cost of credit does not influence consumption. And so it is in Spain, since the demand for household borrowing is not surging, even though the country’s banks keep telling us they are now “ready to lend“.

Deflation Favors Savers Not Debtors

Deflation obviously favors those with money in the bank (unless the banks start charging negative rates on time deposits) since the value of money steadily goes up. It is not so kind on those with debts, since as prices and incomes go down, debts remain unchanged and the burden of paying them increases.

Spain is an endebted country – the net international investment position (NIIP) is negative to the tune of around 100% of GDP – so it isn’t the first place that comes to mind when you think of some kind of “good deflation” process. Japan, in comparison, has a positive NIIP of around 50% of GDP, making it a very different case.

The various sectors in Spain’s domestic economy are also very highly indebted, and the combined debt of government, households and the business sector comes to about 275% of GDP, not that much less than it was at the start of the crisis. This is because while household and corporate debt has reduced, government debt has increased considerably. All of this means that if deflation sets in it will be a serious problem for Spain.

Spain’s external correction still has some way to go in terms of price competitiveness, but having so called “good” competitiveness recovering deflation is not the way to do it at this point, due to the debt impact. This is why ECB policy is directed towards trying to stimulate Euro Area inflation, since obviously if countries like Germany had 2% annual inflation and Spain and others had 0.5% the correction would be a lot less fraught with problems.

Why Is It Likely Deflation Will Continue In Spain?

There are basically two theories why Eurozone countries are suffering from deflation at the moment. One of these is the idea of debt deflation, whereby over-indebtedness creates a consumption drag leading to a shortage of consumer demand while countries deleverage. This is certainly part of the problem that Spain is experiencing.

But there is second theory going the rounds ever since it was put into circulation by US economist Larry Summers at an IMF research conference in the autumn of 2013. The hypothesis Summers advances is based on ideas developed by Alvin Hansen in the 1930s, and the essential point is that countries like Japan and those in the Euro Area are experiencing some kind of demographically driven secular stagnation. This is not the place to go into this theory in any depth, but basically the idea is that as working age population growth slows, comes to a halt and then turns negative consumer demand starts to weaken and eventually decline. This affects the investment process, and it is the structural “underinvestment” which produces the demand shortfall which means there is constant downward pressure on prices.

Paul Krugman provides a useful summary of the argument in his blog post – “Demography and the Bicycle Effect” – and I offer a summary here.Of course, at this point it is only a hypothesis – the worrying thing is that in Spain the possibility that this might be happening hasn’t even been considered, let alone rejected.

So What Is It – Good or Bad Deflation?

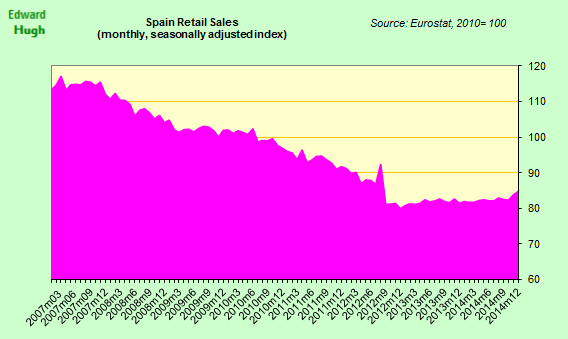

At the moment Spain’s citizens have mainly seen only the good side of deflation: wages and pensions were up while prices fell. Spanish hourly wages rose an annual 0.6% year on year in October 2014 (last date for which we have available data) according to Eurostat, Spain’s pensions were up 0.25% (despite the pension system running a loss of 1.3% of GDP) while consumer prices were down 1.1% year on year in December. In addition 400,000 new jobs were created during the year. It is little surprise then to discover that the statistics office report that price corrected retail sales were up 1% on the year in 2014.

The question is, what happens next? Do workers and pensioners continue to receive above cost-of-living wage and pension increases? This being election year the chances are they do, which means more pressure on profit margins and more withdrawals from the pension reserve fund. And in the longer run, is this sustainable, or will wages and pensions start to fall in line with prices, producing the so called “spiral”?

To get answers to these questions we will need to wait to see in the years to come, but in the meantime important changes may be occurring in consumer behaviour, not only in attitudes towards house purchase, or in terms of any supposed “postponement” activity, but simply in the way people are becoming more sensitive to price movements and bargains. In this context, Justin McCurry’s New York Times article on the Japanese experienece – “Spectre of deflation horrifies bankers, but Japan now has a taste for it – makes interesting

reading. In particular his conclusion:

“Spending habits honed over 20 years die hard. And if Japan’s experience can teach Europe anything, it is that government attempts to haul consumers out of the deflationary abyss are fraught with difficulty. An entire generation has come to embrace the deflationary devil they know. For the population at large, what started life as a reluctant thrift habit borne of necessity has quietly become the economic version of the Stockholm syndrome.”

And here’s another piece of evidence from Japan (The Real Housewives of Japan: Shopping for Bargains … Driving Deflation?) highlighting how years of deflation have lead customers to expect price discounts, and have come to leverage online and social media in the search for ever better bargains.

Could 70,000 Japanese housewives tip this Asian giant into a deflationary spiral?

As farfetched as that sounds, it’s become a major cause for concern in this nation of 128 million, which has been in an economic funk for two decades. These “real housewives” are part of a user-driven, social-networking site called Mainichi Tokubai, which delivers the best prices on specific grocery-store items to the fingertips of Tokyo-region consumers.

To hear frustrated Japanese policymakers and retail executives tell it, these bargain-minded consumers and their equally frugal social-networking site are almost-single-handedly undercutting the Japanese economy.

The above article particularly caught my attention since this is a phenomenon which is increasingly to be seen at work in Spain: people shopping around and expecting bargains, and using online media to help them in their search. In deflationary times the evidence suggests the rise of a kind of “consumer power” where people come to expect permanent sales and discounts and virtually force these on retailers, to the great disadvantage of the small, local shop. This kind of behaviour obviously fuels deflation and when entrenched it is hard to change as Stanley White noted in a 2012 Reuters article.

“A bargain-hunting psychology is so entrenched in Japan — after two decades of stop-start economic growth, 15 years of falling wages and nearly 15 years of deflation — that the government will struggle to convince people that their incomes will improve enough for them to buy more expensive goods.

Spanish policymakers take note, and think twice in future before you say Spain is simply suffering from “good deflation”.