“Nihil sapientiae odiosius acumine nimio“ (Nothing is more hateful to wisdom than excessive cleverness)

Petrarch, “De Remediis utriusque Fortunae”

Like Leo Messi charging his way through a packed Real Madrid defense, twisting now this way, now that, never stopping without being stopped, so did the Spanish sovereign debt surge forward, breaking directly into the red zone near the penalty box, provoking confusion and consternation amongst horrified EU officials and regulators forced to look on as it blindly sought to touch down somewhere well beyond the authorised 100% finishing line.

Spain’s deficit has been much in the news in recent days. Both the target for this year and actual details of last year’s outcome have been the source of much comment, scrutiny, and consternation, but the deficit itself will not form the primary subject matter of this post. What we will be concerned with here is debt, sovereign debt, and the current trajectory of the Spanish variant. In a recent article in the Financial Times Victor Mallet draws attention to the situation and shows how an excessive emphasis on deficits may sometimes mislead people into missing the bigger picture, since at the end of the day deficits are only interesting as they add to debt, and in the long run what matters – as we have seen in the Greek case – is whether or not the debt itself is sustainable.

Now Victor quotes me on two counts: the real size of Spain’s debt, and the effectiveness of Spain’s institutions.

“Spanish sovereign debt is already over 80 per cent of GDP,” said Edward Hugh, a Barcelona-based economist. “I think it’s getting nearer 90 per cent”……Mr Hugh also said the situation in Spain could not be compared to the confusion in the public accounts of Greece because much of the Spanish data are public and made available by the Bank of Spain, or can be deduced from official sources. But he added that the centre-right government’s transparency risked curbing Spain’s room for manoeuvre should the crisis deepen further.

Well, while it’s the first claim that is controversial and in need of justification (and believe me Victor Mallet demanded to see the justification for the numbers before putting up the quote) let’s start with the second one first as it forms an important part of the background. I think it is very important to understand that Spain is not Greece, in the important sense that the people in charge do in fact normally know what is going on. They have auditors and inspectors whose job it is to know, and they do do their job. So the Bank of Spain knows virtually everything there is to know about each and every one of Spain’s many banks and savings banks, about the state of their balance sheets, about the level of bad loans, etc etc. Naturally, knowing what they do is one thing and what they tell you is another matter.

Similarly in the case of the public administration, auditors and controllers are in place to constantly measure and follow the execution of the annual budget at all levels, but again what they know is often one thing, and what they actually say publicly is another. When Spain’s bank regulators become worried about specific cases they try their best to put on a brave face and maintain confidence while looking for solutions somewhere behind the curtain. Similarly with the public administration, although in this latter case there may well be political reasons for allowing an overspend to continue, or even for encouraging it.

Let me take another example, from an area outside the financial system and beyond the realm of public finance: migration statistics. Between 2000 and 2008 around 6 million irregular migrants arrived in Spain attracted by the prospects of work in the then (house) booming economy.

We know with some degree of accuracy the number of such migrants present (although not authorised to be) in Spain due to the existence of a system known as the “Padron Municipal” (or Municipal Register) which is managed via an electronic database. So we know how many migrants register, but how do we know that the migrants always register? Well this is the part which is “typically Spanish”, since a far from innocent circularity has been created – all those present in Spain are entitled to free health treatment in the public health service, but in order to have a health card you need to register with the Padron Municipal. In addition, registration adds to the possibilities of being able to regularise your situation later, so the first thing virtually every migrant does is go to register. You see, that way the central administration has all the data at hand.

Well, you may say, that is fine, but how do we know the register doesn’t overstate the number of migrants? In fact, at one point it did, since migrants were only obliged to confirm their continuing presence every two years. That was when the focus was on measuring who was coming in, but since the economic crash and the massive surge in unemployment, for a variety of reasons the emphasis has moved towards measuring who is still here. So the interval for address confirmations and things like that has changed, and most of those who don’t have residence rights are now required to confirm their presence every few months, which means that Spain has some of the most accurate data on migrant flows to be found within the confines of the EU (and possibly anywhere).

Now, you might say, why be so meticulous in collecting all this information, why not follow the UK example, and require all those who lack authorisation to be in the country to leave? Well, this is Spain and not the UK (or Greece) and this is the point of the present rigmarole I am explaining, to give an idea of how things work in Spain, not to offer an analysis of the migration policy. Understanding that you can accurately measure something that officially doesn’t exist is the key to understanding how the financial and public administration systems work, and unless you “get” this part, you will be lead astray by almost everything else.

The Omnipresence of “Dinero B”

Now, on the public accounts issue itself , I actually started digging into all this in the summer of 2010, and indeed posted an interim “report” at the time. So it is something of a mystery to me why all the hedge funds, journalists and bank analysts have taken so long in waking up to the existence of “Spain’s regional and local debt problem”, especially since all the information on the topic is freely available on the Bank of Spain website. It seems to me that people see what they want to see at any given point in time, and this is the point of the Petrarch quote which starts this post. It comes from an Edgar Allen Poe short story, the purloined letter, and to cut a long issue short, a letter goes missing which no one can find, and the reason they cannot find it is precisely because it is lying there, right before them, on the living room mantelpiece.

“Nothing” remember, “is more hateful to wisdom (astucia) than true cleverness”, which means if you try to go rummaging round Spain for Goldman-Sachs-style interest-rate-swaps you will almost certainly leave empty handed. Handiwork here is all much simpler, and more artisenal than that, and therein lies the beauty and the sophistication of the thing.

Hence, if you are someone who is really interested in trying to answer the question about just how high the present level of Spanish sovereign debt actually is (officially it was to have been 67.8% of GDP in December, but that estimate was made before the latest set of budget deficit “revelations” and when the estimate of 2011 GDP was rather higher than it turned out to be, so it is probably nearer to 70% now, even on the official Eurostat EDP measure) you should start here, with the Financial Accounts of the Spanish Economy. The part you really need is Chapter Two the “Financial Accounts” – actually, I will add in a small but revealing personal anecdote here, since when I sent all these links off to the IMF Spanish Mission Head back in the spring of 2010 he mailed me back saying “thanks a lot” – he plainly didn’t know that this sort of thing existed, although the Spanish head of Global Financial issues for the IMF – ex Bank of Spain man José Viñals – most surely did, but he simply hadn’t seen fit to brief his colleague. As I say, this is how Spain works, you have to ask the right person the exactly right question, and make sure you don’t get sidetracked. Otherwise you will learn nothing apart from a lot of useless and most likely thoroughly misleading information.

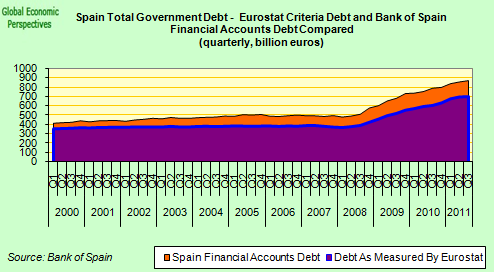

But before we dig down any deeper, just to let us all see where we are, why don’t we make a small detour to Chapter 11 of the Bank of Spain’s Statistical Bulletin, on General government liabilities. Excessive Deficit Procedure (EDP) debt. Now if we examine section 11.3 Liabilities outstanding and debt according to the excessive deficit procedure. Absolute values, we will find this most illuminating table.

Two important points should be drawn to the attention of the studious reader immediately, the fact that the right hand section refers to the Excess Deficit Procedure (EDP or officially recognised Eurostat) debt, and that the totals at the bottom of columns one and 15 are different. The number at the bottom of column one is approximately 877 billion Euros (or around 85% of Spanish GDP) while the number at the bottom of column 15 is 706 billion Euros, and this is the official Eurostat debt. So what makes for the difference? Well, as we will see, there are three main items – unpaid bills, public company debt, and Spanish sovereign bonds which are in the hands of the Social Security Reserve Fund. Now before going into all this further, I do want to make clear that I am not saying that this 877 billion euros is the total Spanish debt which should be counted as such. The number is simply orientative – a lot, but not all, of this is debt which will need to be consolidated – but in fact, and in addition, there are other “contingent liabilities” which will also need to be added in to get a complete reading..

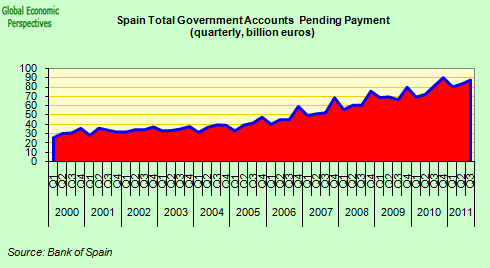

But let’s go one step at a time, and why not start with those famous “unpaid bills”. Well, according to the Financial Accounts, at the end of the third quarter there were 72.9 billion Euros in unpaid bills (around 7% of GDP) which were more than 30 days overdue owed by the entire public administration (see this file here, bottom right second page – in fact there is a total of 87.5 billion Euros owing, but 14.6 billion is still within the term of normal trade credit). This breaks down as 27.7 billion Euros on the part of central government, 20.8 billion Euros from the regional governments, and 14.9 billion Euros for the local authorities. Much of this debt has been pending for months, if not years. It also makes the number of 35 billion Euros which is being bandied about in Spain for the credit lines to local authorities and regional governments seem quite reasonable and realistic. Of course, the central government itself still will need to put its own house in order.

The second main area of non-consolidated debt is the money owed by public companies, many of them loss making, and often entities which have been created without rhyme or reason at both regional and local authority level. As of the end of the third quarter of 2011 this debt amounted to 57 billion Euros (or 5% of GDP – see the memorandum item on the far right in this file), of which 32 billion Euros was attributable to central government, 15.5 billion Euros belonged to regional governments, and 9.4 billion Euros came from companies created by local authorities. There is no plan at present for dealing with all this accumulated debt.

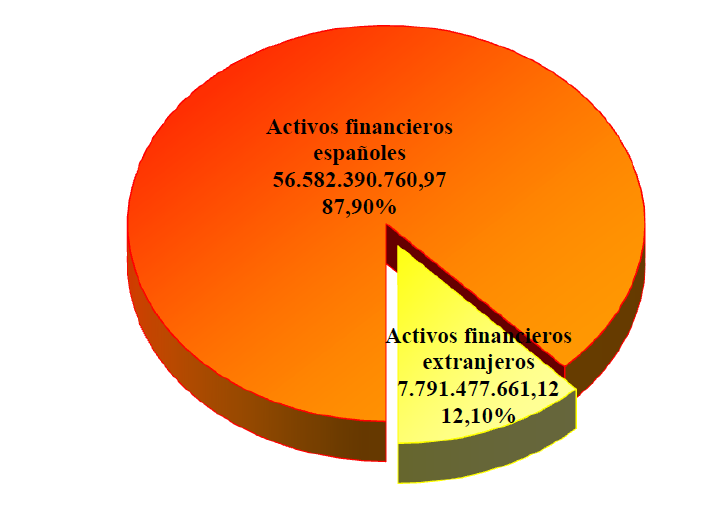

Then, thirdly, we come to the social security reserve fund. Ai, the social security reserve fund! This is where the Spanish are supposed to be accumulating resources to help pay for their pensions. But the Eurostat accounting system being what it is, this is the last thing that is happening. Now according to this last report from the fund managers, at the end of 2010 the fund had assets valued at just under 65 billion Euros under its charge. Of this sum 56.6 billion Euros (or over 5% of GDP) were invested in Spanish government bonds, while 7.8 billion Euros were invested in bonds of other EU states (principally Germany, the Netherlands and France).

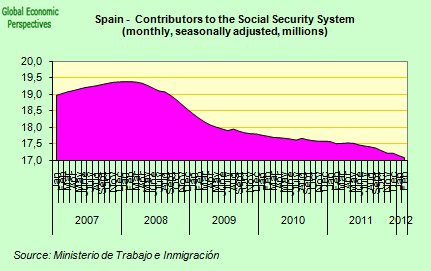

Now doubtless the only reason the fund decided to invest the money it was holding in Spanish government bonds wasn’t to help the administration hide some debt, probably the fact that risky Spanish bonds pay more than less risky German ones was also a consideration. But this whole thing is a farce, since while the Spanish people innocently believe that they have a partially funded pension system, nothing could really be farther from the truth. In general accounting terms the whole security area comes under the general budget, as was brought to light in the recent deficit numbers the new government brought to light at the start of January. Out of a total of 2.5% of GDP in unexpected deficit, 0.5% came from issues associated with the social security fund – which anticipated a surplus of 0.4% of GDP but finally turned in a deficit of 0.1% of GDP, as can be seen in the nice chart provided by the Ministry (below).

The shortfall was due to a number of factors. In the first place those newly entering the system are paid far more than those who are leaving (due to death or other reasons) – 35% more in fact, since the average monthly payment in 2010 was around 800 Euros, while the average payment to new entrants was 1,100 Euros. Secondly Spain’s demography is working against the fund, since as the number of those working falls, and the number of elderly dependents rises, the ratio between the two falls. It is currently at around 2.4, and many experts estimate that the pension system will turn critical when the figure drops below 2.

Currently there are just under 17 million contributors, but the position is worse than it seems, since three million of these are unemployed, with their contributions being paid by another department, and these contributions will terminate when the individuals concerned exhaust their unemployment entitlements. According to Spanish public pensions expert José Mario Paredes Rodríguez, “the data on contributor pensioner ratios is totally misleading” given that the government continues to count as contributors those for whom it is making payments the “calculation is completely unreal since what we need to know is how many people are actually working per pensioner being supported”.

So we really have a clear “robbing Peter to pay Paul” type situation, where the numbers are juggled but the debt remains. The risks associated with this situation was brought to light in the recent Greek debt restructuring, since one of the key issues driving Greek politicians to the negotiating table was the threat of seeing their pension fund reserves going up in smoke in the event of a hard default.

According to the Wall Street Journal:

“The total portfolio of Greek bonds that the Greek pension funds hold is EUR27 billion,” Venizelos said. “That portfolio is being replaced with cash, with new, better bonds of much higher net present value and, further, the parliament has already approved the creation of a special public body through which to transfer public assets to the funds,” he added.

“The dilemma we are faced with is cuts so that we can stand on our own two feet, to save the country’s pension system and pensions, or economic collapse,” Finance Minister Evangelos Venizelos told opposition party lawmakers in Parliament today. Without the debt swap, the country’s pension funds would be wiped out, he said. The country’s central government debt, which doesn’t include debt from local government organizations, state-run companies or pension funds, was 368 billion euros at the end of 2011, the ministry said today, amounting to 171 percent of the economy, according to Bloomberg calculations”.

So just what is the current level of Spanish debt? Well, if we do a rough-and-ready back-of-the-envelope type calculation, and start from the fact that Eurostat debt is currently about 70% of GDP, then add on 7% for unpaid bills, and 5% for state company debt and 5% for debt held by the pension fund, then we come to a total of around 87%, which looks un-nervingly like the 877 billion Euros we noted in the Financial Accounts in the first place.

And Then There Are The Contingent Liabilities

The trouble is, this still isn’t everything. We also have the contingent liabilities of the state to think about. This – a groso modo – comes in four forms: bank debt guarantees, exposure to the financial system via FROB, the government Instituto de Credito Oficial (ICO) and the Electricity Tariff Fund FADE.

On the guarantee side, the latest data we have is for a total of 88.6 billion Euros at the end of the third quarter of 2011, but this number is almost certainly higher now, since the government has been guaranteeing debt on a number of fronts with the unique and exclusive objective that they could be taken over to the ECB to post as collateral in the LTROs. In any event, it is the Spanish state (and not the ECB) that is finally responsible for these loans should the relevant bank or other entity be unable to live up to its commitments.

In the case of FROB (Fund For Orderly Bank Restructuring) the true extent of the government’s exposure is hard to measure, since while the quantity actually provided by the fund to date is not large (14.8 billion Euros – see this presentation – and 9 billion Euros of FROB debt has been pre-capitalised) a number of savings banks are effectively nationalised while others that are dependent on FROB for loans may well need further intervention. So all we can safely say here is that the number involved is hardly trivial, and on just how “non trivial” the final number is the whole future of Spain’s sovereign debt will ultimately depend.

As far as the ICO goes, the organisation currently has an exposure of 27 billion Euros, all guaranteed by the state. Now much of this money has gone out in lending, and much of that lending will be returned, which is why this is a contingent liability. At the same time the present administration clearly see an enhanced role for ICO (helping the regional governments clear their backlog of unpaid bills, for example), and it is likely that the volume of debt will continue to grow.

Finally, we have the so called Tariff Deficit fund, or FADE (Fondo de Amortización del Déficit Eléctrico). Now despite the name, one thing the debt generated by this body doesn’t do is fade (away), since it is growing month by month and year by year. The position is described in the literature as a debt being accumulated by consumers (some 24 billion Euros of it) which is guaranteed by the government. Like the state of their savings in the pension system, most electricity consumers are totally ignorant of the fact that they are acquiring this debt, or better put, that it is being acquired on their behalf. Essentially the situation arises since the government is reluctant to charge an economic price for electricity. Naturally, in a country running an energy driven current account deficit this is a highly questionable practice, but then, there you are.

Basically every month less money comes in in bills than is attributed to the accounts of the electricity companies. The shortfall is made up by borrowing. This borrowing is serviced – you got it – by taking some of the income from electricity bills. But naturally, as the deficit grows – currently it is about 24 billion Euros – more of the income stream is needed to service the existing debt, and – yup, you got it again – the deficit grows. The only real solution to this mess is to raise electricity tariffs, but in an environment of rising unemployment and falling wages there are going to be limits to what the government can do in this regard. So while I am sure that the EU will eventually insist tariffs are raised, it is hard to see them being raised far enough to pay off the accumulated debt, and so the government will almost certainly need to “swallow” this, which means – yup you got it again – another 2% or so on the debt account.

Just to round things off, there are some other little details, like public private collaborations in infrastructure. Take motorways for example, many of these (especially around Madrid) were planned at the height of the boom, when traffic was intense – the private sector are of course paid according to the number of cars who use the motorway. Now with the crisis the volume of traffic has fallen considerably everywhere (this is one of the few advantages I have noticed of all this difficult mess, it is now much easier to move around in Barcelona). And with the fall in traffic, incomes have fallen, to such an extent that the participating companies are no longer able to service their debt. Experts suggest the total quantity involved is around 4 billion Euros – peanuts you may think in comparison with the other things we are looking at, but as they say in Spanish “todo suma”.

Much Ado About The Deficit

Now as Victor Mallet says, the basic motivation behind recent moves on the Spanish administration front would seem to be to start to move this large backlog of debt (especially at the regional and local government levels) onto the table.

Madrid plans to arrange payment of up to €30bn in overdue bills for rubbish collection and other services owed by municipalities, a move that will benefit suppliers but will also help to expose the true size of the country’s public sector debt.

“It’s about restoring order, it’s about knowing what’s there and dealing with it once and for all,” Maria Soraya Sáenz de Santamaría, deputy prime minister, said after a cabinet meeting on Friday that agreed the first part of the programme.

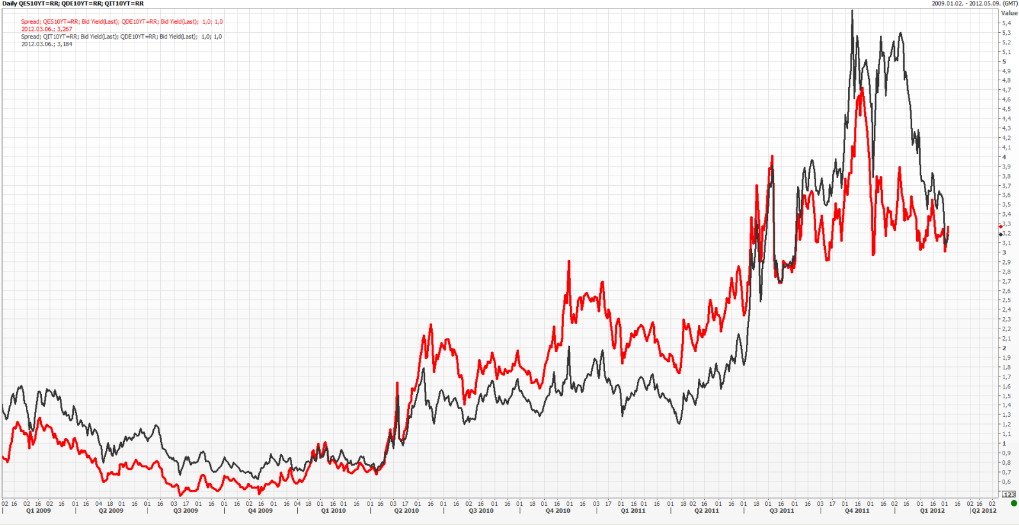

But the great risk they are taking in doing this is raising the acknowledged debt level, up towards the “high risk area” of around 100% of GDP. When you add all the debt up we are already in the high 80% range, and two more years of “normal” deficit plus more funding for the financial sector should take it through the psychological barrier. Naturally investors are noticing this, and Prime Minister Mariano Rajoy’s “gaffes”, and at the end of last week the Spanish ten year bond spread with the Bund equivalent went above the Italian one for the first time since last summer.

So Spain is on a bad course, with recognised debt about to surge rapidly, while investor confidence in the current administration is slipping. Time for another “gamechanger” I think, since otherwise this car is about to crash.

Her mind in torment, wheeling like some lion at bay, dreading the gangs of investors and bond traders closing their cunning ring around her ready for the finish, Angela thrashed around looking for the rules and pacts that would save her embattled army. To no avail, her chariot struck a rock which, like the one to the west of Grosseto which saw-off the unfortunate Costa Concordia along with her Captain, was on no known map, having not previously been measured, and she went hurtling down that crazed path which leads only towards a preappointed destiny with both history and oblivion.