We don’t yet know what lies ahead—default? Exit from the euro? Exit from the EU? Some kind of muddling through with a parallel currency and a declaration that any default is “only technical”? Answers to those questions will come only after Greek voters make a choice.

Meanwhile, here are some program notes and links to background material that should help place the Greek crisis in the context of similar episodes elsewhere.

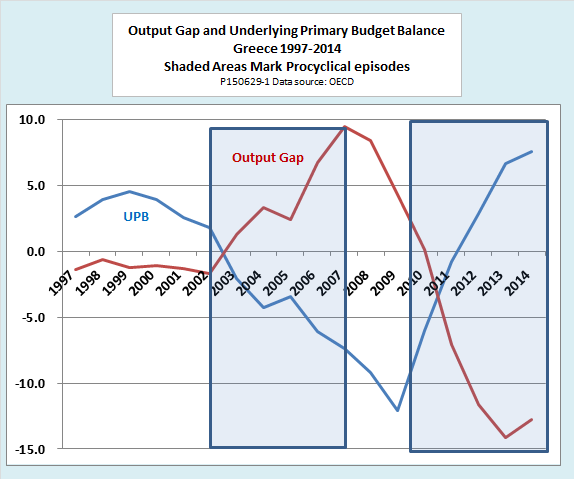

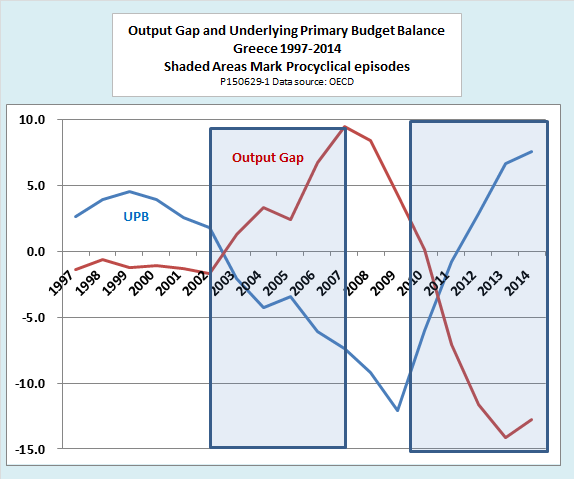

How Tough has Greek Austerity Really Been?

To hear Greeks tell it, their country has undergone a deeper slump and tougher austerity measures than any other European country. Some of their EU partners, on the other hand, portray the Greek government as unwilling to take moderate, common-sense measures that everyone else has already successfully implemented. What do the numbers say?

This post, published at the time of the elections that brought the radical left Syriza party to power, shows that the Greek perception is largely correct. The slump in Greece, as measured by the gap between current and full-employment levels of GDP, has been catastrophic, a plunge of more than 20 percentage points. At the same time, budget cuts and tax increases have moved the best indicator of austerity—the underlying primary budget balance—nearly 20 percentage points toward surplus. Those movements far exceed what has happened in the United States or in any other European country.

In short, Greek fiscal policy has been profoundly procyclical. It is true that in the early 2000s, overly expansionary policy added to the pre-crisis boom. In more recent years, however, stringent fiscal policy clearly deepened the slump and now seems to have reversed the incipient recovery that is visible in the chart. It is understandable why Greek voters want a change

Comparisons to Cyprus

The closing of Greek banks immediately brings the 2013 Cyprus crisis to mind. Cyprus closed its banks to stop a run and, at the same time, imposed capital controls that limited the amount of money that individuals and businesses could take out of the country. These notes on the Cyprus crisis explain all the technicalities of bank runs, capital controls, bail-outs, bail-ins and the rest.

Still, any comparison of Greece and Cyprus reveals differences as well as parallels. The biggest difference is that insolvent banks were the cause of the Cyprus crisis, whereas Greek banks are the victims of the crisis. That said, the tools that Greece will have to employ to keep its banking system from collapsing altogether are much the same.

Could Greece Make a Graceful Exit?

There is a growing likelihood that Greece will leave the euro. Some observers make much of the technical difficulties involved in leaving a currency area, but Greece would not be the first country to do so. Lessons from others who have faced a similar challenge suggest that with proper management, a graceful exit might be possible.

A transitional currency is one device that some countries have used. For example, when the ruble area broke up in the early 1990s, Latvia used a temporary Latvian ruble to ease the introduction of a more permanent currency, the lats. A permanent currency can be introduced with an untarnished reputation after a transitional currency has absorbed some of the shock of inflation or devaluation in the first months after exit from a currency area.

The parallel between the breakup of the ruble area and Greece’s possible exit from the euro is imperfect, however. The ruble was a failed currency that was associated in the public mind with inflation and shortages. The euro, in contrast, is a model of stability. Public opinion polls suggest that a majority of Greek citizens would prefer to keep it if possible, increasingly unlikely though that seems.

In some respects, Argentina’s exit from its currency board, which had maintained a fixed value of the peso against the dollar, is a closer parallel. The transition to an independent currency in Argentina was chaotic, to say the least. It was accompanied by defaults, bank failures, currency controls, and public unrest. One feature of the Argentine transition was a period in which several parallel currencies circulated, including paper notes and IOUs issued by provinces, cities, and even factories. Some observers expect such parallel currencies to appear in Greece at any moment.

This post from 2013 drew three lessons for Greece from earlier crises that could make an exit from the euro less painful: Consider use of a transitional currency; don’t fear the use of parallel currencies; and default early, but not often.

However, that post also pointed out that not all problems associated with exit from a currency area are mere technicalities. The case of Argentina shows that if a change of currency is accompanied by a default, it can take a long time to return to international credit markets. The government of the defaulting country, in turn, may have to make a hard choice between austerity no less stringent than that previously demanded by foreign creditors, or inflationary policies that lead to domestic unrest.

Stay tuned for daily developments.

Related posts

Breakup of the Ruble Area (1991-1993): A Cautionary Tale for the Euro (Slideshow version here.)

On Technical Barriers to Leaving the Euro and Learning from Others’ Experience

Bail-outs, Bail-ins, Haircuts, and All That: Program Notes for the Cyprus Drama

Tutorial on Bank Failures and Bank Rescues