In a pair of posts [1] [2] last fall, when EZ inflation was merely low, but not yet negative, I explained that there are two kinds of deflation.

The nasty kind of deflation, which everyone rightly fears, is driven by falling aggregate nominal demand. As demand collapses, it drags both real output and the price level down with it. There is a serious risk of a self-reinforcing downward spiral in which debtors can’t repay their loans, defaults and falling asset prices undermine the financial system, zero interest rates render monetary policy powerless, and rising unemployment sparks social unrest.

However, there is also a benign kind of deflation, driven by rising productivity. In that scenario, conservative monetary policy restrains the growth of nominal GDP while real output surges ahead. The rate of inflation is negative, but growing output provides borrowers with the cash flow they need to repay their loans, rising productivity allows real wages to rise, and nominal interest rates, although low, do not need to fall all the way to the zero bound. In the US and UK, such productivity-driven deflation was the norm during much of the nineteenth century and reappeared again, more briefly, in the prosperous 1920s.

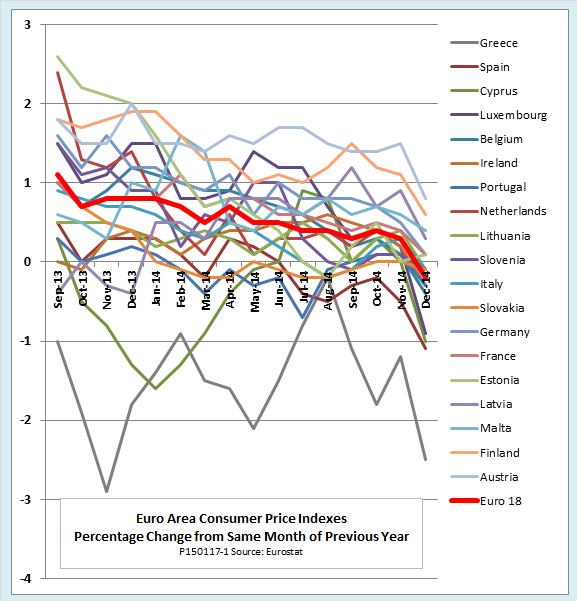

So which kind of deflation is Europe facing now? The bad, demand-driven kind, or the good, supply-driven variety? A little of each, it seems.

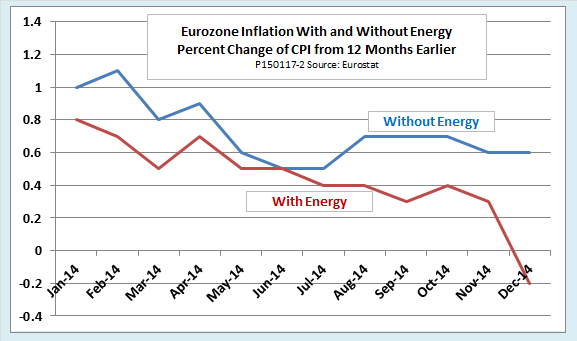

The good news is that the recent transition from positive to negative inflation for the EZ as a whole comes largely from the supply side via falling energy prices. As the next chart shows, core inflation—the CPI with energy stripped out—remains positive.

For an importing area like the EZ, the impact of falling oil prices is much the same as that of productivity growth. To understand why, imagine that the EZ were a closed economy that produced all of its own oil, and that some technological breakthrough doubled the productivity of the oil industry. Only half as many resources as before would be needed to sustain oil output; the rest could go to producing other goods and services. The only difference is that currently we are not looking at a decrease in resources needed to produce oil, but instead, a decrease in the resources needed to produce the goods and services that are traded for oil.

The bad news comes in the form of two big “ifs:” Falling oil prices could theoretically lead to steady growth combined with falling prices, but only if the improvement in terms of trade were sustained, and only if the economy were otherwise healthy to begin with. Unfortunately, we can’t count on either.

Oil imports into the Eurozone amount to about 4 percent of GDP. Roughly speaking, then, the fall of oil prices by half in recent months could be expected to have a beneficial impact equivalent to a 2 percent growth of productivity for the economy as a whole. That is very welcome, but oil prices are not going to fall in half again next year and the year after that. Instead, they are going to stabilize and then rise at least part way back toward the $100 mark. In contrast, the productivity gains that led to growth with falling prices in the nineteenth century and the 1920s continued year after year.

Furthermore, the EZ economy was far from healthy before oil prices began falling. It came into 2014 with inflation under 1 percent and falling, real growth under 1 percent and stagnant, and unemployment stubbornly stuck above 10 percent. Even before oil prices began their plunge in the second half of the year, the Eurozone was already on the brink of a malign deflationary spiral driven by inadequate demand. Several of its members were already over the brink.

So back to our question: Should we call what is happening right now in the Eurozone “real” deflation? Not quite. Right now both the supply and the demand side of the economy are driving inflation lower, but demand is not yet weak enough to cause outright deflation by itself.

In a best-case scenario, Europe’s fiscal and monetary authorities could take advantage of the oil price windfall to reverse their policies of demand restraint. They could, for example, simultaneously ease budgetary austerity and pursue a program of all-out quantitative easing. By the time oil prices inevitably started to rise again, the underlying economy might be on the road to recovery.

In the worst case, the window of opportunity will close again without anything having been done. If that happens, the threat of a “real” demand-driven deflationary spiral will still be there.

Follow this link to view or download a tutorial on deflation in theory and practice