Yesterday Greek voters overwhelmingly rejected the policies of extreme austerity favored by its Eurozone partners. Yes, Greece’s problems are, at least in part homemade. No outside powers forced it to run the excessive deficits that fed an overheated boom in the years leading up to the global crisis. But the draconian fiscal consolidation to which the country has been subjected since 2009 came largely from outside. It has both deepened the slump and shredded the social safety net that might have allowed the Greek public to live through it without revolution at the ballot box.

The US economy is much healthier, but that has not stopped many American economists from arguing that fiscal policy here has been little better than that of Greece (see this post by Paul Krugman, for example). US policy, too, allowed the precrisis boom to overheat and then unnecessarily prolonged the recession. And we, unlike the Greeks, have no one to blame but ourselves.

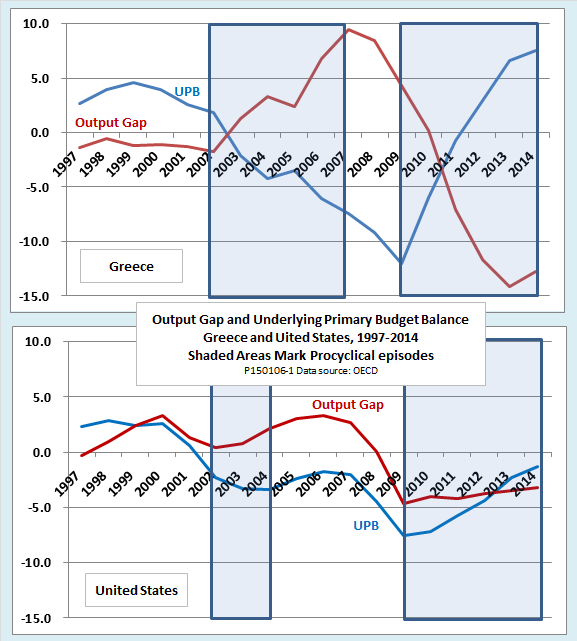

Economists use the term procyclical to describe policies that amplify the business cycle rather than moderating it. The following charts show just how procyclical the two countries’ budgets have been.

The first indicator in each chart is the output gap. The gap is the amount by which real GDP is above or below a long-run trend, known as potential real output, that is estimated to be consistent with full employment and price stability.

The second indicator is the underlying primary budget balance (UPB). The UPB is the surplus or deficit of the budget that is adjusted for the effects of the business cycle on tax revenues and cyclically sensitive spending like unemployment benefits. It also omits interest payments on government debt, and one-off measures like privatization or tax amnesties. (Without the adjustment for one-off measures, the UPB is called the cyclicaly adjusted primary balance or structural primary balance. One-off measures are insignificant for the United States but important for Greece.)

Because it eliminates the tendency of recessions to move the budget toward deficits and booms to move it toward surplus, the UPB reveals the effects of policy changes. An increase in the UPB signifies fiscal restraint, while a decrease indicates stimulus. A UPB close to balance is consistent with long-run stability of the ratio of government debt to GDP. (See this earlier post for a more detailed discussion of the structural primary balance and debt dynamics.)

Shaded areas in each chart indicate periods in which fiscal policy has been procyclical, that is, when policy changes have added stimulus when the economy was already booming or restraint when it was slowing or in a slump.

Look first at the episodes that begin in 2002, when, in both countries, the UPB moves toward deficit, providing fiscal stimulus, even though the output gap is positive and rising. In Greece, this procyclical episode continues until 2007, when the output gap reaches nearly 10 percent of GDP and the UPB is -7.4 percent. (It is worth noting that the chart shows revised data; according to a European Commission audit, the budget figures reported by the Greek government at the time were manipulated to show a smaller deficit.) In the US, the procyclical episode lasts only until 2004. After that time, although the UPB remains in deficit, it moves back toward balance providing at least a slight degree of fiscal restraint as the boom approaches its peak.

The arrival of the global financial crisis is marked in both countries by a sharp downturn in the output gap. Both countries initially responded with orthodox countercyclical measures in the form of spending increases and tax cuts. Without that fiscal stimulus, the initial phase of the recession would, presumably, have been even sharper. However, by 2009, fiscal policy in both countries turned procyclical again.

Under pressure from bond markets and EU authorities, the Greek government undertook a massive austerity program that, by 2014, moved its underlying primary balance toward surplus by nearly 20 percent of GDP. The result was a catastrophic collapse of output and employment, with the output gap reaching a negative 14.2 percent in 2013. The pattern of fiscal policy in the United States was also procyclical after 2009. Congress began to push the underlying primary balance toward surplus while output and employment were still near their cyclical lows. Although the degree of austerity was not enough to send the country into outright depression, as happened in Greece, it made for a very sluggish recovery. In fact, OECD forecasts that a negative output gap will persist in the US at least through 2016.

The bottom line? Greece wins the prize for the OECD’s worst fiscal policy over most of the past decade. However, the Greeks can at least say it was not entirely their fault. Yes, they positioned themselves badly with irresponsible policy in the years leading up to the boom, but they have had very little room for maneuver since the global crisis. Political pressures from deficit hawks among their fellow EU members has been only one factor. Membership in the euro, which takes away control over monetary policy and subjects them to strict fiscal rules is a more serious constraint. The most limiting factor of all in the first phase of the crisis was the impossibility of borrowing from international markets at any affordable interest rate.

The United States, in contrast, has only itself to blame. American fiscal conservatives helped to set up their problems by turning a blind eye when the Bush administration was cutting taxes and hiding the costs of the Iraq war in off-budget accounts, but no outside powers forced the US Congress to impose sequesters and government shutdowns in the middle of the worst recession since the 1930s. The US has an independent currency that gives if full freedom to operate as it wants on both fiscal and monetary fronts. And throughout the crisis, federal borrowing costs have remained at historic lows.

We know how Greek voters have reacted. Now we much wait and see how European governments react to the election results. In America, where the next election cycle is just beginning, the situation is less predictable. What would Republicans do if they took full control of the government in 2016? By that time, the economy is likely to be close to full employment. Would the GOP remain true to its rhetoric of fiscal responsibility, or would it slash taxes and boost military spending just as the economy enters the next boom, just as it did a decade ago? What would Democrats do if they reverse the GOP’s recent electoral momentum? Would they return to the big-spending ways that their opponents accuse them of, but which they have, in practice, largely abandoned? We, too, will have to wait and see.