Accounting for inflation

As in many discussions of macroeconomics, we first need to deal with the effects of inflation. Economists use the term nominal to refer to quantities stated in the ordinary way and real to quantities that are adjusted to for inflation. Real wages are the most familiar example: We all understand that if our boss raises our nominal wage from $10 per hour to $12 per hour, but at the same time inflation adds 20 percent to the price of everything we buy, our true purchasing power has not changed.

A similar principle applies to exchange rates. Other things being equal, a change in the nominal exchange rate of the ruble would mean change in the competitiveness of goods the country produces for export and those it produces for sale at home in competition with imports. However, inflation also has an impact on competitiveness—one that can either amplify or offset changes in the nominal exchange rate.

For example, a nominal depreciation of the ruble from 20 rubles per dollar to 25 per dollar would, by itself, make it easier for Russian exporters of steel and wood products to compete in world markets. At the same time, if would make it easier for Russian farmers and automakers to compete with imports. On the other hand, inflation that raised prices and wages within the Ruble economy would undermine competitiveness of Russian exporters and import-competitors, even if the nominal exchange rate were unchanged. If the nominal exchange rate depreciated at exactly the rate of inflation, competitive relations would remain unchanged. The ruble price of wood or steel exported from Russia would rise, but the dollar price to foreign buyers would not change. On Russia’s internal market, depreciation of the ruble would drive the ruble prices of imported cars and butter up at the same rate that inflation raised up the prices of their domestic competitors.

To deal with the combined effects of inflation and nominal exchange rate changes, economists calculate a real exchange rate that adjusts a country’s nominal exchange rate for any inflation that takes place in its own economy or that of its trading partners. Here are some illustrations, using Russia and the United States as examples. (Follow this link for a more detailed discussion of real exchange rates.)

- If there is no inflation in either country, or their rates of inflation are equal, then any nominal appreciation or depreciation of the ruble relative to the dollar results in an equal real appreciation or depreciation.

- If Russia experiences faster inflation than the US, but the ruble depreciates in nominal terms at a rate just equal to the inflation differential, then there is no change in the real exchange rate.

- If there is no change in the nominal exchange rate but Russian inflation outpaces US inflation, then the real exchange rate of the ruble appreciates. Russian producers find it harder to compete both on international and domestic markets, while Russian consumers find that a week’s wages will buy more imported goods than before.

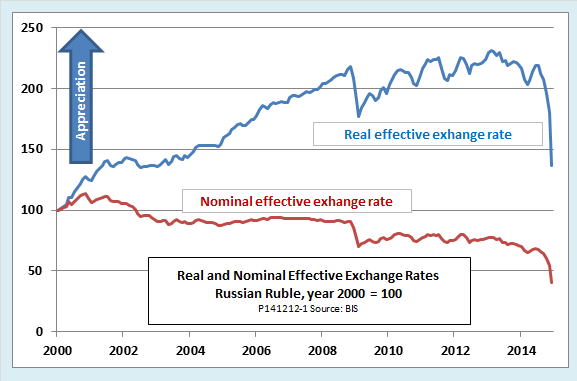

To extend the concept beyond just two countries economists look at a country’s real effective exchange rate (REER), which averages the real bilateral rates of its currency with those of all of its trading partners. The next chart shows the evolution of Russia’s real and nominal effective exchange rates since 2000.

The chart falls into several periods, which illustrate different relationships between real exchange rates, nominal rates, and inflation:

- In 2000, both the real and nominal rates appreciated. The real rate appreciated faster than the nominal because Russian inflation of more than 20 percent was faster than that in its trading partners.

- From 2001 through 2003, and again from 2009 through 2013, the nominal rate held roughly steady. During these periods, inflation pushed the REER steadily higher.

- During the global financial crisis, from June 2008 to February 2009, the real exchange rate fell by 17 percent and the nominal rate by 23 percent. The faster depreciation of the nominal rate reflected an uptick in the inflation rate. The crisis of 2014 has followed the same pattern, but this time the REER fell by about 25 percent over the course of the year while that of the nominal rate was more than 40 percent.

The role of oil

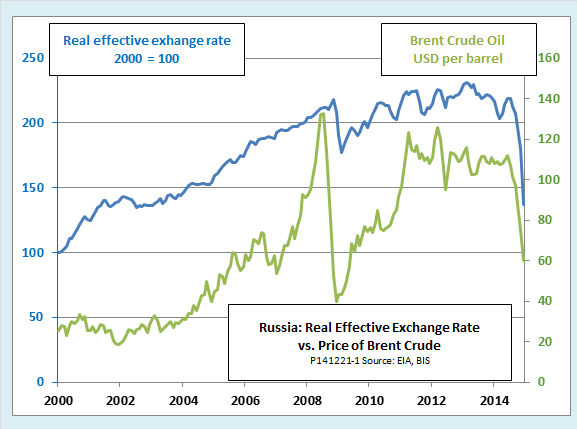

Inflation, as we have seen, explains why the rate of change in the real exchange rate can be faster or slower than that of the nominal exchange rate. However, inflation tells us nothing about what causes the real exchange rate to change in the first place. There is no great mystery about that in the case of the ruble. As the next chart shows, movements in the real effective exchange rate of the ruble are dominated by movements in the price of oil. In fact, over the period displayed in the chart, the simple correlation between the world price of oil and the Russian REER is over 90 percent.

The strong link between Russia’s real exchange rate and the price of oil has, in some ways, been a blessing, and in others, a curse. In the early 2000s, the steadily rising real exchange rate contributed to a rapid rise in living standards that allowed many Russians to move into the middle class and helped to alleviate the poverty of others. During the same period, under the policies of Finance Minister Alexi Kudrin, high oil prices allowed the Russian government to accumulate reserves that permitted it to get through the 2008 financial crisis with the lowest government debt of any G-20 country.

Oil dependence has also had its downside, however. In particular, the doubling of the real exchange rate during Putin’s presidency undermined the competitiveness of sectors like farming and light industry, which faced higher labor costs as living standards rose and tougher competition from imports as the ruble appreciated. As I explained in a post in April, economists call this phenomenon the “Dutch disease.”

In principle, the current decline of the real exchange rate should bring some relief from the Dutch disease, but it will not be quick or easy to develop local replacements for imported food and consumer goods. For one thing, as our charts show, even the recent free-fall of the ruble still leaves the real effective exchange rate well above its 2000 level. Furthermore, Russia ranks far below most of its G-20 peers in terms of the ease of doing business, a factor that weakens the ability of its economy, especially the small and medium businesses necessary for a more balanced economy, to adapt to changing circumstances.

What role have sanctions played?

Putin has lashed out at Western sanctions as a cause of Russia’s economic slump, a reaction that may show they are succeeding in their political objective of imposing pain on people with close ties to the Kremlin. In particular, sanctions are making it more difficult for Russian businesses to roll over their debts to foreign banks. The government is already having to use some of its financial reserves to prop up big banks and energy companies. Meanwhile, consumers are feeling the pain of Russia’s decision to respond with sanctions of their own against food imports from the United States and the EU. Finally, the threat that sanctions could be tightened further may be spurring precautionary capital flight.

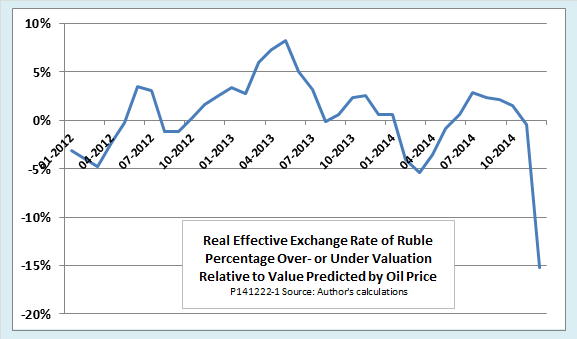

Until we have more macroeconomic data to support this anecdotal evidence, it is hard to estimate accurately how much sanctions have contributed to the fall of the ruble. However, the following chart, which shows how much the real effective exchange rate of the ruble is over- or undervalued relative to the rate that would be predicted by the price of oil alone, does provide some preliminary indication of a measurable effect.

If we take the chart at face value, it would appear that the first and second rounds of sanctions, imposed in March and April 2014, had little impact. World oil prices were little changed from March to July, yet even in the face of sanctions, the REER of the ruble appreciated by about 6 percent. July saw a tougher round of sanctions, however, targeting not just individuals but major banks and nonfinancial corporations. From July to November, the price of oil fell by about 30 percent. In response, based on the relationship of oil prices to the exchange rate over the whole period of 2000-2014, we would have expected the real effective exchange rate to depreciate by about 15 percent, compared to an actual depreciation of about 19 percent. By mid-December, oil prices had fallen below their November average by enough to cause a further expected depreciation of about 8 percent. Instead, the observed depreciation was about double the predicted amount. However, the data for December are preliminary. Although these observations are consistent with the hypothesis that sanctions are working, we should take them as no more than suggestive.

Policy options

When the ruble’s plunge began to accelerate in early December, one lawmaker called for Elvira Naibullina, head of the central bank, to be arrested for treason. By and large, though, Naibullina, who seems to have Putin’s backing, is doing about as well as we could expect, given the limited options the country faces.

The fact is that when a country is hit by a major external shock, like the oil price slump and sanctions now afflicting Russia, there is not much anyone can do to prevent a depreciation of the real exchange rate. About all policy can accomplish is to shape the form that the damage takes.

One option is to defend the nominal exchange rate. Many countries have done that in crises past. It is tempting to do so, partly out of blind national pride, and partly to stem losses on debts, public and private, that are denominated in foreign currency. Unfortunately, holding the line against nominal devaluation has big drawbacks.

For one thing, it can be costly. The central bank’s main weapon for defending the nominal exchange rate is to sell foreign currency from its reserves (assuming it has any, which Russia does). Unless the crisis is brief and the bank fully holds the line, rather than merely slowing the rate of depreciation, the bank ends up having to rebuild reserves later when the exchange rate is less favorable. The Bank of England’s unsuccessful attempt to defend the pound in 1992 is estimated to have cost it ₤27 billion. Russia’s central bank suffered smaller but still painful losses in failed attempts to defend the ruble in 1997 and 2008.

In addition, defending the nominal exchange rate by selling reserves can touch off destabilizing speculation. Speculators can borrow the threatened domestic currency and invest the borrowed cash abroad. If the exchange rate depreciates despite the central bank’s efforts, speculators will earn a huge profit when they repay their loans. The most they can lose, even if the defense succeeds, is the interest on some short-term loans. The more intense the speculation becomes, the more likely it is to succeed. George Soros is reputed to have made a $1 billion profit from such a one-way bet against the Bank of England during the 1992 crisis.

Instead of selling reserves, a government can try to defend the nominal exchange rate with a policy of austerity. The central bank can raise interest rates and the government can slash its budget. That is the course taken by members of the euro area, for whom simple devaluation is not an option, but it can take the country into a prolonged depression with soaring unemployment.

Wary of these costs, Naibullina declared in November that the central bank would allow the ruble to float freely. She has kept that pledge for the most part. The central bank has undertaken only limited sales of reserves, although the government has intervened indirectly by placing pressure on private corporations to sell some of their own foreign currency holdings. It also raised interest rates sharply when the ruble briefly hit a speculative low of 80 to the dollar in mid-December.

Floating the ruble has probably been a wise distinction, on balance, but it has costs of its own. Inflation is the most obvious. As the nominal exchange rate depreciates, the ruble cost of imported goods increases. Imported substitutes are not available for many goods. Even when they are, limited supply and growing demand pushes up their prices, too. As prices rise, the government comes under pressure to raise the salaries of its workers and benefits of pensioners. If it gives in, it adds to inflationary pressure; if it resists, it risks political discontent.

The inflationary effects of the currency collapse are only now beginning to work their way through the Russian economy. As the next chart shows, gradual reduction in Russia’s chronic inflation, from more than 20 percent when Putin took office to a post-Soviet low of 5 percent in 2012, was one of the signature economic accomplishments of his presidency. Even before oil prices and the ruble began their slide, however, inflation had begun to creep up again. Data for November, the most recent available, show inflation running at an annual rate of about 16 percent. Inflation for the full year in 2015 could easily be that high or higher.

In the short run, the Russian government seems to be managing the negative economic consequences of sanctions and falling oil prices about as well as it could. The long-run outlook is not positive, however. Real prosperity, as opposed to the cyclical booms and bust of a mid-sized petro state, will have to await development of a more diversified economy, a better business climate based on the rule of law, and better political relations with the rest of the world.

Follow this link to view or download a slideshow with additional information about real and nominal exchange rates