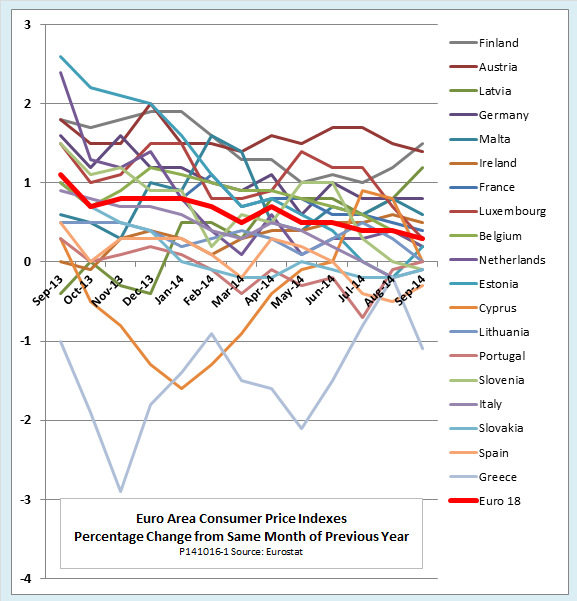

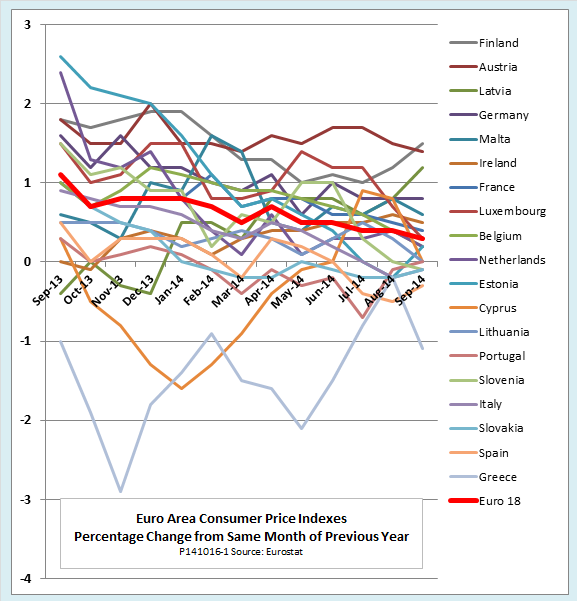

Europe is fearful as it teeters on the brink of deflation. As the chart shows, September consumer prices in the eurozone were just 0.3 percent higher than in the same month a year earlier. That is far below the 2 percent inflation target set by the European Central Bank (ECB). Five countries were already experiencing deflation, and inflation was at zero in three others.

Still, despite all the gloomy deflation headlines, the most common question I get about deflation is, “So what?” If inflation is bad, why isn’t deflation good? Why should we do anything but celebrate if the prices of goods and services fall steadily year after year, and the value of our money rises accordingly? In this post, the first of two parts, I will try to explain just why a majority of economists think deflation is bad. In the second part, I will look at the views of a minority who think that deflation is actually a good thing, at least sometimes.

Delayed consumption—the wrong answer?

Probably the most frequent explanation of the harm done by deflation is that it gives consumers an incentive to delay consumption. A recent article in Salon puts it this way:

When prices fall people stop spending, hoping things will get even cheaper. In response, businesses cut production and lay off workers. That means even less demand, and prices drop further. . . By then, your economy’s in a vicious downward spiral.

This reasoning seems superficially plausible, but it has one big flaw. Although it is true that it pays to delay spending when prices are falling, it can also pay to delay when prices are rising.

Consider an example. You need a new dishwasher, which would cost $500 if you bought it today. You read that the economy is experiencing 2 percent deflation, which suggests that the dishwasher will cost $490 if you wait a year. If you hold your $500 in cash, which may be the best savings vehicle you are can find in a deflationary economy, you will gain $10 by waiting a year

Now think back a few years to when 3 percent inflation was the norm. That would mean your dishwasher would go up in price to $515 if you waited a year, but remember also that back in those days, your bank would probably have offered a 1-year certificate of deposit with an interest rate of something like 5 percent. If you put your $500 in a CD for a year, you’d have $525 when it matured. That means delaying your purchase would give you exactly the same $10 net gain as it would with cash saving and 2 percent deflation.

The point here is that the decision of whether to delay consumption depends not just on the rate of inflation, but on the difference between the rate of inflation and the rate of interest you can earn on the money you set aside for your later purchase. Economists call that the real rate of interest on consumer savings to distinguish it from the nominal rate of interest, which is the interest stated in loan contracts and advertised in the window at your local bank. So long as nominal interest rates rise by enough to keep ahead of inflation, as they normally do, the real interest rate remains positive and there is still an incentive to delay purchases.

It follows that deflation only discourages consumption when prices fall faster than the usual real rate of interest on consumer savings, say, more than 2 or 3 percent. However, that is more deflation than any euro country is now experiencing, and more than Japan saw even in the worst years of its long deflation. We have to conclude, then, that the tendency of deflation to cause consumers to delay purchases isn’t really one of the big reasons to be afraid of falling prices.

Deflation and banking

The effects of deflation on banks and other lending institutions are a more important reason to fear deflation. Although it might seem that the effects of deflation on borrowing and lending would be the mirror image of the effects of inflation, they are not.

The zero interest rate bound. A big part of the reason for the asymmetrical effects of inflation and deflation lies in the fact that nominal interest rates cannot fall below zero. Economists call this the zero interest rate bound.

Here is the problem: When inflation rises, banks can adjust the nominal rate of interest upward to hold the real rate constant at a level that they think will be profitable for them while still affordable for customers. For example, if they want a 4 percent real interest rate on mortgage loans, they can set the nominal rate at 5 percent when there is 1 percent inflation, at 7 percent when there is 3 percent inflation, and so on. However, if there is deflation, and if the rate of deflation is faster than their target real interest rate, there is nothing they can do to keep the real rate from rising. If there is 3 percent deflation (that is, -3 percent inflation), they can set the nominal mortgage rate at 1 percent to get a 4 percent real rate, but zero is as low as they can go. If there is 5 percent deflation, the real rate rises to 5 percent even if the nominal rate is zero, then to 6 percent if there is 6 percent deflation, and so on.

As a result, when there is rapid deflation, borrowers find that the real cost of borrowing increases, even if lenders don’t want that result. As it becomes more and more expensive to borrow, people build fewer houses, buy fewer cars, and the economy slows down or starts to shrink.

Expected vs. unexpected deflation. Inflation and deflation have asymmetrical effects on banks in another way, as well, which we can understand by distinguishing between expected and unexpected changes in the price level. Suppose that initially, inflation is 2 percent and banks are charging 6 percent on mortgage loans, giving a 4 percent real rate of return, which is enough to cover costs and earn a modest profit. If banks expected inflation to rise to a steady 5 percent, they could protect their real income by raising the nominal interest rate to 9 percent. If borrowers expected their incomes to grow 3 percent faster than before, they would not object.

Suppose instead, though, that the increase in inflation to 5 percent was completely unexpected. Banks that had lent at 6 percent would then find their real return squeezed to just 1 percent. On the other hand, borrowers would enjoy a windfall. With wages rising more rapidly, it would be easier than they expected to repay the 6 percent loan. What is more, inflation would be pushing up the value of their home, giving them more equity if they decide to sell.

Now run the same scenarios for a case where inflation falls from 2 percent to -1 percent, and wage growth slows by the same 3 percentage points. Again, if deflation is expected by both parties, the lenders adjust their nominal interest rate down to 3 percent and no one feels any real effects. But what if the deflation is unexpected?

It might look like unexpected deflation would give banks a windfall gain, since they would now be earning a 7 percent real return, not just 4 percent, on the pre-deflation loans that they had made at 6 percent. Borrowers, stuck with 6 percent mortgages and slowing incomes, would suffer a corresponding loss. However, the windfall gain to banks would be illusory, for two reasons. First, many borrowers would refinance their old loans at lower rates that reflected the new reality of falling prices. Second, as deflation squeezed incomes, some borrowers who had taken out 6 percent mortgages would probably be forced into default. When banks foreclosed, they would find that deflation had depressed prices in the housing market so much that they could not sell the collateral for enough to cover the outstanding loan balance.

The long and the short of it, then, is that the banking system works best when prices are stable or are rising at a moderate and predictable rate. Rapid inflation, especially when it is unexpected, is bad for banks and other lending institutions, but deflation is bad for them, too.

Deflation and monetary policy

The zero bound also causes problems for monetary policy as conducted by the Federal Reserve, the ECB, and the central banks of other countries. The standard practice of central banks is to cut interest rates when they want to stimulate the economy and raise them when they want to put on the brakes. More specifically, the interest rate they use as a target to carry out their policies is typically the nominal rate in some very short-term, low-risk financial market. In the US, the Fed uses the federal funds rate, which is the rate that banks charge to one another for overnight loans of reserves. Because they are short-term and low risk, such rates are among the first to hit the zero bound when the economy slows. In the United States, the federal funds rate has been effectively at the zero bound since late 2008.

When a central bank’s target interest rate hits the zero bound, it can either declare itself out of ammunition and surrender, or it can cast about for another weapon. The Fed, the Bank of Japan, and now the ECB have reached for an alternative policy called quantitative easing (QE), which involves massive purchases of assets like longer-term government bonds and mortgage-backed securities. The hope is that QE will stimulate the economy by lowering long-term interest rates and by increasing banks’ liquid reserves.

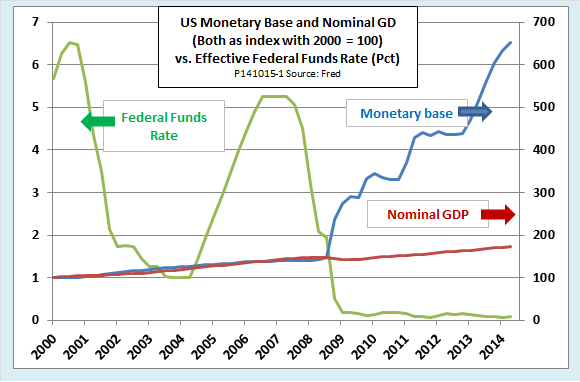

Unfortunately, it is not clear that QE is all that effective. Consider the following chart. The green line shows the path of the federal funds rate (left axis). As early as mid-2007, the Fed reacted to the developing financial crisis by aggressively lowering its target, until, in late 2008, it hit the zero bound. At that point, nominal GDP (red line, right axis) was essentially flat. In an attempt to restore GDP growth, the Fed began buying assets at a rapid pace. The effect of QE on the Fed’s balance sheet was dramatic, measured in the chart by the growth of the monetary base (blue line, right axis), which is the part of its liabilities consisting of currency and bank reserves.

Before the crisis, the growth of the monetary base and nominal GDP tracked closely together. It seemed reasonable to hope that more money in the system would boost GDP growth, but it is hard to see any dramatic effect in the chart. To be fair, this is only eyeball econometrics. Economists at the Fed and some elsewhere who have used more sophisticated statistical methods maintain that QE has had at least a small beneficial effect, and that without it, the modest GDP growth visible in the chart would have been even less. Still, the idea is pretty much dead that the Fed can use QE to froth up the economy at will, as if it were a cup of cappuccino. (For a more detailed discussion of the mechanics of quantitative easing and how well it works, see this tutorial.)

Deflation and labor markets

Inflation and deflation also have asymmetrical effects on labor markets. Labor markets have little trouble adjusting to moderate inflation. As inflation boosts consumer prices, employers earn added revenue. They return some of that revenue to workers in the form of cost-of-living increases that are sufficient to keep real wages from falling. Sometimes union contracts require these cost-of-living increases. Sometimes employers give them because they fear that those who don’t will lose their best staff to others who do. In either case, workers accept the raises without protest. They see cost-of-living raises as something that employers owe them as a matter of simple fairness.

In times of deflation, though, wage psychology works differently. Suppose that consumer prices are falling at a rate of 5 percent per year, squeezing employers’ revenues. In theory, they could tell their workers that they were cutting wages by 5 percent. Employers might see the cuts as entirely fair. They could explain that because prices were falling at the same rate, workers would suffer no loss of real income.

However, it is unlikely that workers would see it that way. They would more likely view falling consumer prices as something they had every right to enjoy. It would not seem fair at all for their employer to snatch back the windfall. Even if workers did not quit or go on strike, they would sulk and productivity would decline. Where workers were unionized, it is likely that the escalator clause in their contracts would require wage increases to match inflation, but would prohibit wage decreases to match deflation.

The fact that wages are flexible upward in times of inflation but sticky downward in times of deflation has consequences for the wider economy. We have already seen that the financial and monetary effects of deflation tend to slow growth or even bring on a recession. The downward stickiness of wages makes matters worse because it means that real wages tend to rise when prices fall. Rising real wages are fine for workers who are lucky enough to keep their jobs, but in a slump, they encourage layoffs and discourage new hiring. Unemployment rises.

The deflationary spiral

To sum it all up, when you put the asymmetries of banking, monetary policy, and labor markets together, you create a risk of a downward deflationary spiral: Banks stop lending. The burden of debts contracted during inflationary times begins to rise. Borrowers struggle to pay off debt and some default. As labor markets stop working smoothly, unemployment rises and even those who keep their jobs feel pinched. At the same time, the zero interest rate bound robs monetary policy of its effectiveness, making it harder to reverse the downward spiral. As deflation accelerates, it becomes ever harder to do anything about it.

More than anything else, the fear of such a self-sustaining deflationary spiral explains why most economists favor doing whatever it takes to stop deflation before it starts. That includes building in a moderate positive rate of inflation (2 percent seems to be the favorite target for advanced economies) that allows a margin of error in case of unexpected deflationary shocks.

Still, not everyone, not even all economists, are aboard the anti-deflation bandwagon. There are some who say deflation is actually good for us and others who more cautiously suggest that it is not always bad. In the second post of this series, we will look at those dissident views.