First a bit about the Tax Foundation and its competitiveness index. The foundation invites journalists to describe it as “a non-partisan research think tank, based in Washington, DC,” but not all agree. For example, Dan Crawford, writing for Angry Bear, says, “Its work is aimed at one purpose–convincing Americans that they pay too much in taxes and that government is too big.” Others point out contributions from the Koch Family foundations and ties to other conservative groups as signs of partisan bias. Paul Krugman says flat-out that “knowledgeable people don’t trust the Tax Foundation.”

In an important way, though, the Tax Foundation’s conservative ties only reinforce its credibility as a monitor of tax system features that are perceived as burdensome by its corporate friends. The foundation is entirely up front about what the Tax Competitiveness Index tries to measure:

A competitive tax code is a code that limits the taxation of businesses and investment. In today’s globalized world, capital is highly mobile. Businesses can choose to invest in any number of countries throughout the world in order to find the highest rate of return. This means that businesses will look for countries with lower tax rates on investments in order to maximize their after-tax rate of return. If a country’s tax rate is too high, it will drive investment elsewhere, leading to slower economic growth.

When the foundation gives the United States a low competitiveness score, then, it is simply saying that there are a lot of things about our tax system that corporate businesses don’t like—the kinds of things they consider when they decide where to locate, how to operate, and where to find funds for their investments.

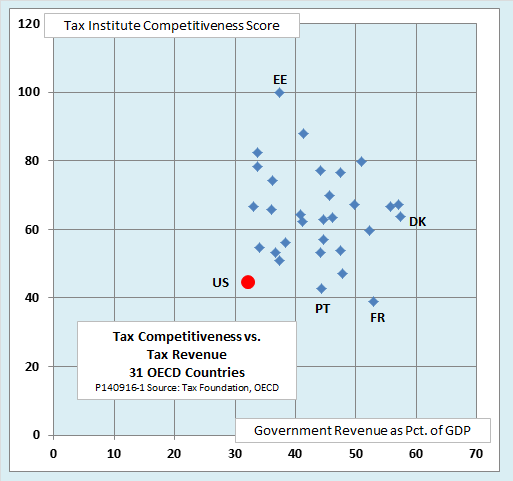

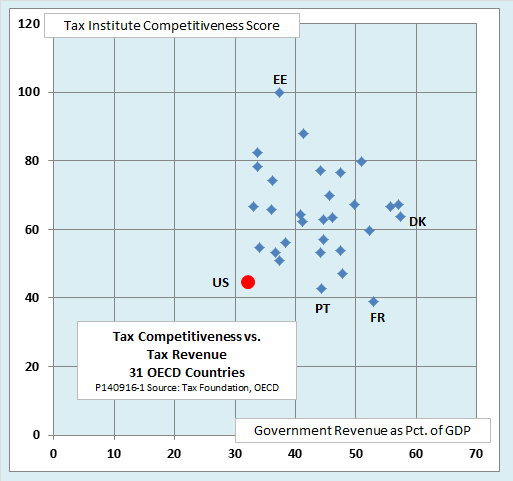

What really strikes me, though, is not just how uncompetitive the US tax system is (in the Tax Institute’s sense of the word), but that it manages to be so uncompetitive while raising so little revenue. Take a look at the following chart, which plots the Tax Institute’s competitiveness score against total government revenue as a share of GDP. The revenue data include both tax and nontax receipts of governments at all levels, central, regional, and local. Rather than trying to label every point in the chart, I have provided a table covering all 31 OECD countries for which both data points are available.

Notice that the United States falls at the extreme south-west corner of the scatter plot. Despite its uncompetitive tax system, US government at all levels collects less revenue in relation to GDP than any other OECD country.

Think about it. It is not surprising that the corporate citizens of France view their country’s tax system as burdensome. After all, France has to feed a huge government sector that swallows up revenue equal to 53 percent of GDP, and still runs a budget deficit of more than 3 percent. Yet the US tax system manages to be nearly as uncompetitive as that of France while raising 40 percent less revenue.

Or compare the United States to Denmark, whose government collects the most revenue of any of its OECD peers—57.4 percent of GDP. You would think such a massive tax take would render Denmark radically uncompetitive, but instead, its Tax Institute score is 43 percent higher than that of the United States, close to the OECD average.

Having read this far, you may be about to raise a frequent objection to the claim that US corporate taxes are excessively burdensome. Yes, the top rates are high, you might say, but few actually pay them. In a recent briefing paper on how to stop corporate inversions, the FACT Coalition makes the point this way:

Lowering the U.S. corporate rate is not the answer because most corporations don’t pay the full rate anyway. Corporate lobbyists and their allies point to the U.S.’s official corporate tax rate of 35 percent as justification for brazen use of inversions and other tax avoidance schemes. In fact, very few American corporations actually pay that rate as a percentage of their profits. Fortune 500 corporations that were consistently profitable from 2008 through 2012 paid, on average, just 19.4 percent of their profits in federal income taxes over that period. Twenty‐six of these corporations paid nothing over the five‐year period while collectively earning $169 billion in profits.

The problem with this argument is that it ignores the financial, administrative, and strategic costs of tax avoidance. Sure, you can lower your tax burden by moving your corporate headquarters to Ireland, but if such a strategy were costless, then everyone would be there by now. In reality, you can avoid taxes only by making locational, operational, and financial decisions that you would not otherwise make—precisely because they are costly.

Suppose your corporation owes $35 million in tax on $100 million in profit, for a net $65 million after tax. By changing your product line, your corporate headquarters, and your sources of financing, you can cut your taxes to $10 million. Unfortunately, implementation of those measures incurs administrative costs of $10 million and cuts your revenue by $10 million. You end up with after tax profit of $70 million.

Yes, that’s still worthwhile in the sense that you are $5 million better off than if you had just paid your taxes. But what is the accurate measure of the burden that the US corporate tax system places on your company? Is it the 11 percent you pay on your remaining $90 million in before-tax profits, or is it 30 percent—the bite that taxes plus tax avoidance costs take out of your original $100 million? Obviously, it is the latter.

In short, the amount of revenue actually paid is not a complete measure of the degree to which a country’s tax system undermines its competitiveness. The Tax Institute makes just that point when it says,

Low rates are not the only component of a good tax code; a tax code must also be neutral. A neutral tax code is simply a tax code that seeks to raise the most revenue with the fewest economic distortions. This means that it doesn’t favor consumption over saving, as happens with capital gains and dividends taxes, estate taxes, and high progressive income taxes. This also means no targeted tax breaks for specific business activities.

If the US tax code is bad, what would be good, in the eyes of the Tax Institute? Here is how they characterize the tax system of Estonia, the only OECD country to earn the maximum possible score of 100 on their competitiveness index:

[Estonia’s] top score is driven by four positive features of its tax code. First, it has a 21 percent tax rate on corporate income that is only applied to distributed profits. Second, it has a flat 21 percent tax on individual income that does not apply to personal dividend income [i.e., no double taxation]. Third, its property tax applies only to the value of land rather than taxing the value of real property or capital. Finally, it has a territorial tax system that exempts 100 percent of the foreign profit earned by domestic corporations from domestic taxation with few restrictions.

Now there’s something for Congress to think about. Why not a revenue-neutral reform of our corporate tax that incorporates some of those Estonian features, makes a big cut in the top rate, and closes a whole bunch of loopholes? I say, Go for it!

Related posts:

What Happened to Corporate Tax Reform?

Controversy over Romney’s Taxes Underlines the Need for Broad Reform