The best way to see what has been going on since the first of the year is to look at the old, the rebenchmarked, and the newly revised data on a sector-by-sector basis, as in the following table:

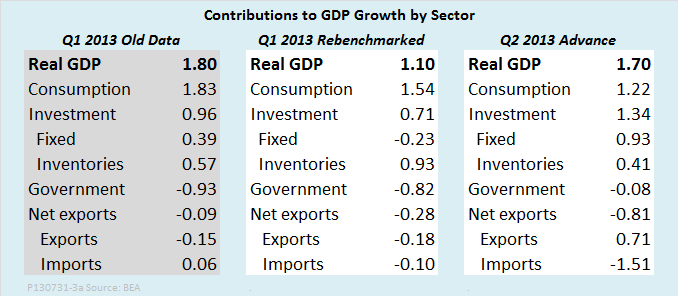

The first thing we see in this table is that the contribution of consumption to real GDP growth slowed from 1.54 percentage points in Q1 2013 to 1.22 percentage points in Q2. Q1 consumption, in turn, was revised downward from a contribution of 1.83 percentage points. Consumption of durable goods picked up slightly in Q2. The slowdown was about evenly divided between services and nondurable goods.

Investment was the strongest performer in Q2, contributing 1.34 percentage points in Q2, up from 0.71 in Q1. A downward revision of Q1 investment explained part of the slow growth in that quarter. Fixed investment contributed .93 points to Q2 growth after shrinking in the first quarter. Residential structures were the strongest component of fixed investment, with nonresidential structures, business equipment, and intellectual property products also making larger positive contributions to growth than in Q1. Inventories grew slightly slower in Q2, with most of the change due to a slowdown in the growth of farm inventories.

Fiscal drag—a negative contribution to growth from smaller government—has been a factor slowing growth throughout much of the recovery. However, the negative contribution of government to GDP growth was very small in Q2, just -0.08 percentage points, compared to -0.82 percentage points in Q1. The federal government continued to shrink, but the contribution of state and local government was slightly positive for only the second time since late 2009. The data shown are for government consumption expenditure and gross investment, a measure that includes all government purchases of goods and services but excludes transfer payments.

Net exports made a negative contribution to growth in Q2, but the news in this sector was not all bad. Exports, which have been a relatively robust contributor to GDP growth throughout most of the recovery, contributed a respectable .71 percentage points to growth in Q2, after making a negative contribution in Q1 for the first time since the first quarter of 2009. In view of the recession in the eurozone and the slowdown of most emerging market trading partners, the positive growth of exports is very welcome. The drag on growth is now coming not from falling exports but rather, from growing imports. Imports are recorded as a negative item in the national income accounts, so the -1.51 percentage point contribution of imports means an increase of imported goods and services. An increase in imports, rather than the small decrease earlier reported, was another factor behind the downward revision of Q1 GDP growth.

The rebenchmarking of GDP data covers all sectors of the economy and reaches back five years. I will discuss some of the changes it makes in the full sweep of the Great Recession and subsequent slow recovery in a subsequent post.