As the following table shows, personal consumption expenditure was the most important component of the acceleration. Consumption contributed 2.24 percentage points to the Q1 growth rate, compared to just 1.28 percentage points in Q4. Nearly all of that came from the service sector. Housing services and utilities, recreation, and financial services all showed strong gains. Growth in consumption of goods slowed slightly.

The growth of investment also increased, but not in a way that necessarily points to continued growth later in the year. Total investment contributed 1.56 to Q1 growth, up from just .17 in Q4, but fixed investment slowed. Most of the increased investment was in private inventories, with seasonally adjusted growth of farm inventories especially strong. Coming after a decrease in Q4, that may represent no more than a delayed adjustment to normal inventory levels, rather than more aggressive inventory building based on optimism about future sales growth.

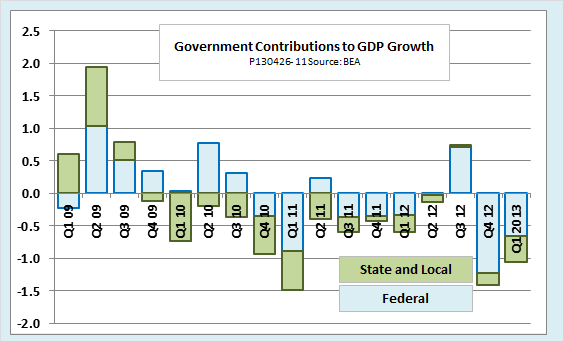

The contribution of the government sector to GDP growth was again negative in the first quarter, as it has been for most of the past three years. Government is represented in the GDP accounts by an item called government consumption expenditure and gross investment, which includes spending on goods and services at all levels of government, but excludes entitlements and other transfer payments. A decrease in federal spending accounted for three quarters of the decrease, but every other component, federal, state, and local, fell at least slightly. Although the United States has not gone to the extremes of austerity of some European countries, still, the procyclical drag of a shrinking public sector has been a consistent factor slowing the recovery.

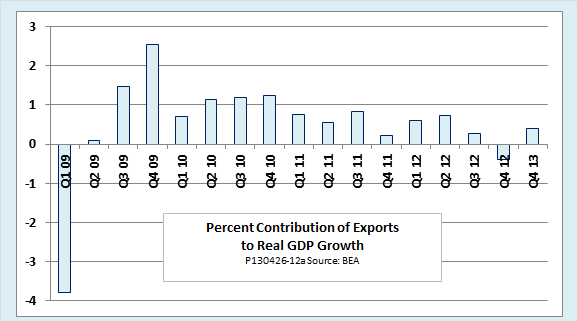

Turning to the foreign sector, the BEA reported that exports made a moderate but positive contribution of 0.4 percentage points to GDP growth in Q1. That was welcome news after Q4 data had shown exports decreasing for the first time since the recovery began. However, export growth was more than offset by a rebound in imports. Imports enter into the GDP accounts as a negative number, so the reported -0.9 percentage point contribution of imports indicates a greater volume of imports that more than offset the 0.4 percent contribution of exports.

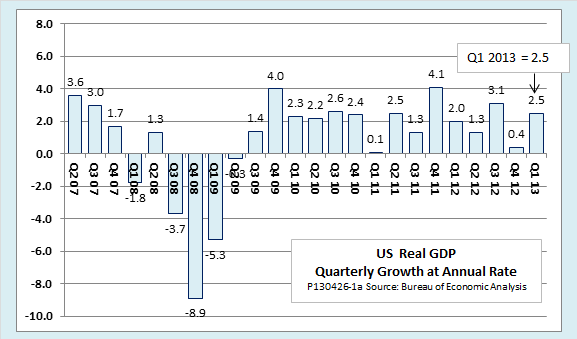

The advance estimate of GDP is based largely on data from early in the quarter, supplemented by extrapolations of historical trends. The rebound in growth is consistent with the strong job market performance reported earlier for the first two months of 2013. Advance estimates of GDP growth are subject to substantial revision. The average revision between the advance and third estimates, without regard to sign, is 0.7 percentage points. If the third estimate of Q1 GDP growth, due out in June, is revised by no more than the average amount, it should fall in the range of 1.8 to 3.2 percent.