I know the feeling behind these questions. It is the same as I get when I go to an opera sung in an unfamiliar language. If you are among those who ask such questions, what you need are some program notes to help you understand the Cyprus drama, and by extension, other banking crises like it.

Act 1, Scene 1. How can we tell if a bank has failed?

System-wide banking crises like that in Cyprus always begin with the failure of individual banks. In principle, it ought to be easy to tell when a bank has failed. In practice, that is not always the case.

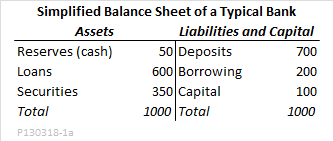

Let’s start with the simplified balance sheet of a representative bank. The bank’s assets include all the things of value that it owns. This bank has $50 worth of reserves in the form of deposits at the central bank, currency in its ATM machines, and other items that we loosely refer to as “cash.” Next come loans to consumers and businesses, which are the largest item for most banks, $600 in this case. The bank also holds securities, such as government bonds or mortgage backed securities, worth $350 dollars. A real bank balance sheet would have other smaller items, including buildings and business equipment.

The bank’ liabilities include all the things it owes to others. Deposits are the biggest category for most banks. Banks also borrow funds from other creditors, for example, by selling bonds and through short-term interbank markets. Some of this borrowing is secured by specific collateral and some is unsecured.

We define the bank’s capital, which represents the shareholders’ stake in the bank, as total assets minus total liabilities. Businesses like industrial corporations or retail stores often have capital equal to half or more of their assets. This bank has capital equal to just 10 percent of assets, which is typical of the banking sector. We say that a bank with a low ratio of capital to assets has a high degree of leverage.

It is clear from these definitions that any loss in value of the bank’s assets, while its liabilities remain unchanged, will reduce a bank’s capital. The most common reasons for a loss of asset value are failure of borrowers to repay loans in full (credit risk) and decreases in the market price of securities the bank owns (market risk). If the losses are big enough, capital falls to zero or below, and the bank fails. The technical term for bank failure is insolvency.

In the case of Cyprus, banks’ biggest losses came from investments in Greek government bonds, which lost value as the Greek government struggled with its own financial crisis. The following before-and-after balance sheets show what happens to our simplified bank when the securities it holds fall in value by $100. (Items that change are shown in color.) After the loss, the bank’s assets have fallen to just $900 while its liabilities of $900 remain unchanged. Its capital—assets minus liabilities—has fallen to zero. It is insolvent.

In practice, it is not always easy to tell whether a bank is solvent or not just by looking at its balance sheet. There are two main reasons for this.

First, not all bank assets are marked to market. That means that the book value that the assets are given on the balance sheet does not always reflect the value at which they could be sold.

Second, some balance sheet items are assigned values for regulatory purposes that are different from the values they would have under ordinary accounting standards. As a result, capital, as measured by regulators, can be much greater than capital as measured by simple subtraction of liabilities from assets. (For a long wonky discussion of this point, see this earlier post.)

For these reasons regulators are often the last to declare that banks have failed, even long after the fact is apparent to everyone else. That is exactly what has happened in the case of Cyprus. By any common sense measure, they are insolvent, but as of this writing, the European Central Bank (ECB) has not yet officially declared that to be the case.

Act 1, Scene 2. Bank Runs

A loss of asset value is always the proximate cause of bank failure, but bank runs can be a contributing cause. The classic form of bank run occurs when depositors line up to withdraw their money from a bank because they fear it will become insolvent. Sometimes, as in the case of Cyprus, regulators try to stop a run by temporarily closing the banks, but even when the banks were closed, Cypriots drained every euro they could out of their ATMs. Runs are not always limited to depositors. They can also take the form of a refusal by non-deposit creditors to renew the bank’s short-term borrowing. For example, other banks may cut off interbank loans to a bank that looks at risk of failure.

If a bank had unlimited reserves of cash or if it could always sell its loans and securities at the full value listed on its books, a run could not cause insolvency. It would simply reduce liabilities and assets by equal amounts, leaving capital unchanged. However, not all of a bank’s assets are fully liquid, that is, capable of being converted to cash at their full value on short notice. What often happens is that a bank faced by a run quickly exhausts its reserves of cash. After that it may be forced to sell assets at “fire sale prices.” Remember, the assets are not marked to market, so that the price they bring from a quick sale may be well below what they would be worth if the bank could hold them until they mature. When a run forces a bank to sell assets for less than their book values, total assets fall by more than liabilities, and capital quickly falls toward zero.

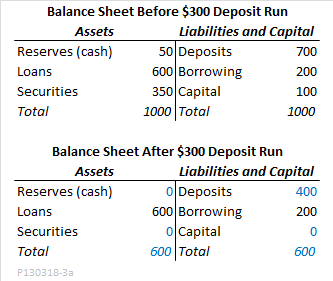

The next set of before-and-after balance sheets illustrates how a run can cause an apparently solvent bank to fail. In this case, imagine that depositors suddenly withdraw $300. The bank meets the first $50 of withdrawals out of its cash reserves. When those are gone, it tries to sell some of its securities. However, when it tries to sell them on short notice, perhaps at a time when the market is nervous because other banks are also threatened with failure, it has to accept fire-sale prices. In this case, we assume that it needs to sell all of its securities, previously valued at $350, to gain the remaining $250 it needs to pay to depositors. In the end, although the bank’s liabilities fall by just $300, the value of its assets fall by $400 and it becomes insolvent.

Act 2, Scene 1. Liquidation and haircuts

If regulators permit it, an insolvent bank may manage to stay open at least for a time. The ECB has allowed that in the case of the insolvent banks of Cyprus, at least for the time being. However, insolvent but operating banks, sometimes called “zombie banks,” are dangerous. Since their shareholders no longer have any capital to lose, they may be tempted to take extreme risks in the hope of restoring solvency. In other cases, seeing that the end is near, owners or managers may simply steal the bank’s remaining assets and disappear. Even if managers act in good faith, as long as the banks stay open, their losses are likely to continue. As their capital falls farther into negative territory, any eventual restructuring becomes more and more costly. In short, good regulatory practice dictates that insolvent banks not be allowed to continue operations.

Suppose regulators decide to follow good practice and liquidate a failed bank. We can see how this works by continuing our earlier example, starting from the last balance sheet shown above. Liquidation means selling remaining assets for whatever they will bring and then distributing the proceeds of the sale among those with claims against the bank. In this case, the bank’s remaining assets consist of loans with a book value of $600, but since the loans are not marked to market, so it may not be possible to sell them for that much. Suppose that when regulators sell them as part of the liquidation process, the best price they can get is $500. They must then decide who gets the money.

Normally, liquidation gives highest priority to depositors. In this case, sale of the loans produces enough cash to pay off the remaining $400 of depositors’ claims in full. The next highest priority goes to other creditors, who have $200 in claims. Since there is only $100 left after paying off depositors, those non-deposit creditors get just 50 cents on the dollar. In financial slang, they are said to receive a haircut of 50 percent.

In practice, assignment of haircuts is complicated by the fact that some of the bank’s borrowing is usually secured by claims on specific collateral like government securities. The secured creditors are legally beyond the reach of haircuts. Suppose, for example, that the $200 of borrowing of our simplified bank consisted of $75 of secured borrowing and $125 of unsecured borrowing. The secured creditors would get their full $75. Distributing the remaining $25 among the unsecured creditors would then amount to a haircut of 80 percent on their $125 of claims.

Some banks, including those in Cyprus, have very little by way of unsecured borrowing. Their liabilities consist almost entirely of deposits. In such a case, liquidation could easily not realize enough cash to pay depositors in full, so they, too, may be subject to haircuts. That is exactly what EU authorities initially recommended for Cyprus: Large depositors were supposed to take a 9.9 percent haircut, and small depositors a haircut of 6.75 percent. Cypriots were furious. Wealthy Russians, who have a lot of money deposited in the banks of Cyprus and a lot of behind-the-scenes clout in its parliament, were even more furious. Even the President of Russia, Vladimir Putin, jumped into the fray, calling the proposed restructuring plan “unfair and unprofessional.” Even after the plan was changed to protect small depositors, the Cypriot parliament rejected the proposed haircut, deepening the crisis.

Act 2, Scene 2 Tools of restructuring

In practice, regulators do not always liquidate insolvent banks. They are especially likely to avoid liquidation if they think a bank is too big to fail (TBTF). They may see a bank as TBTF because of a fear of financial contagion, for example, the fear that failure of a large bank might start a panic that would damage the whole financial system or might cut off a vital source of credit for nonfinancial businesses. In other cases, the perception of TBTF may reflect political capture of the regulators by banks, though cronyism, a revolving door of appointments between bankers and regulators, campaign contributions, or other forms of corruption.

If, for whatever reason, regulators think a bank is TBTF, they must carry out some kind of restructuring that will restore it to solvency. Several tools are available to do this.

The simplest tool is to loan the bank some cash. Such a loan can give the bank time to sell off assets at better prices and to shrink its balance sheet to a manageable size. If the loan is made at a below-market interest rate, it may help stem losses or even make the bank profitable again.

As the crisis in Cyprus deepened, the ECB continued to make loans to the country’s troubled banks. That is one of the reasons it refrained from declaring those banks insolvent, since its charter permits it to loan money only to banks that are solvent, or that it can at least pretend are solvent.

Knowledge that the government stands ready to act as lender of last resort to the bank may be enough to stop a run. However, because the immediate effect of a loan is to raise liabilities and assets by the same amount, it does not immediately increase a bank’s capital. For that reason, although loans can help weak banks that face temporary liquidity problems, they are not by themselves enough to save banks that are already deeply insolvent.

A more powerful tool of bank restructuring is for regulators to exchange some of the bank’s bad assets for good assets supplied by the government. For example, suppose the bank holds securities backed by subprime mortgages that have a face value of $100 million, but a market value of only $50 million. Swapping the mortgage-backed securities for $100 million of safe government bonds would add $50 million to the bank’s capital. This kind of asset swap is sometimes called a carve-out. Regulators then move the bad assets to the balance sheet of some agency that has the job of selling them or managing them to extract as much value as possible. Such an agency sometimes goes by the colorful name of a bad bank.

Another powerful tool of restructuring is to supply cash or safe government bonds to the bank in exchange for shares of stock. Such an operation, which increases the bank’s capital even more directly than a carve-out, is called a capital injection.

Act 2, Scene 3. Bailouts and bail-ins

Sufficiently large capital injections or carve-outs can bring even the most troubled bank back to solvency, but they can be very costly. In the case of Cyprus, the cost of the rescue plan proposed by EU authorities was roughly 40 percent of the country’s GDP. When regulators rescue an insolvent bank, they must not only decide what tools to use, but who will bear the cost.

The first question is what to do about a bank’s shareholders. One possibility is a full nationalization of the bank that wipes out the original shareholders altogether. The government can then use a carve-out or capital injection, or both in combination, to restore the nationalized bank to solvency, and eventually reprivatize it.

At the other extreme, the government may use a combination of loans and carve-outs that leave the shareholders in place as owners of a newly solvent and profitable bank. It is that kind of restructuring that most accurately deserves the term bailout.

In between, the government may decide to recapitalize the bank through an issue of new shares that leaves the original shareholders in place but dilutes their stake in the bank’s capital. Such a case, where shareholders suffer losses but are not fully wiped out, amounts to a partial bailout.

The next question is what happens to the bank’s unsecured creditors. As explained above, if a bank’s capital falls below zero, a simple liquidation will result in losses (haircuts) for unsecured creditors. However, restructuring through a carve-out or capital injection may leave unsecured creditors untouched, bailing them out in full even when shareholders suffer losses.

Bailouts of bank shareholders and unsecured creditors are not popular. They are often an object of popular protest, and equally, of criticism by financial specialists. Both ethical and practical reasons lie behind the unpopularity of bailouts.

The ethical case against bailouts rests on the notion that shareholders and bank creditors are grown-ups. They willingly put their money at risk by investing it in banks that they should have seen, through due diligence, to be far from risk free. If the gamble of buying shares in a shaky bank or making unsecured loans to it pays off, investors expect to keep their profits. Accordingly, if the gamble does not pay off, it is only just that they should take their losses.

The practical reason for not bailing out unsecured creditors is that doing so creates a situation of moral hazard. In finance, that term means a situation in which people who are protected from risk are tempted to take greater risks. If people know that the government will bail out the shareholders and unsecured creditors of banks that are TBTF, but not those of banks that are small enough to liquidate safely, they will provide funds to TBTF banks more cheaply than to smaller banks. That gives large banks a competitive edge over smaller ones, so they grow ever bigger, making the TBTF problem worse over time. Critics like Richard W. Fisher, President of the Federal Reserve Bank of Dallas, think that is exactly what has happened in the U.S. banking system since 2008

To avoid the ethical and practical problems of bailouts, regulators may insist that unsecured creditors, as well as shareholders, take haircuts as a condition of the restructuring. Our earlier example showed how haircuts work for a bank that is being liquidated. When the bank is being restructured instead of liquidated, the same logic applies. Every dollar of haircut that creditors are subject to means one less dollar that regulators must inject into the bank to restore its capital to an adequate level.

For example, suppose a bank has $200 million in unsecured borrowing and needs $100 million in capital to become adequately solvent. Regulators might agree to inject $50 million of government funds into the bank on the condition that creditors agree to a 25 percent haircut. The haircut reduces the value of the bank’s liabilities by $50 million, so that the combined effect of the haircut and the capital injection is to increase the bank’s capital by the necessary $100 million.

Such an arrangement makes the unsecured creditors partners in the government’s recapitalization efforts rather than beneficiaries of it. For that reason, it has come to be called a bail-in of unsecured creditors, to distinguish it from a bailout, in which creditors benefit from the restructuring without being called on to make any contribution to it.

What about depositors? Most countries protect small depositors through deposit insurance. For example, the Federal Deposit Insurance Corporation in the United States protects deposits up to $250,000 per depositor per bank. A much more controversial issue is whether large depositors, too, should receive full protection. U.S. regulators extended unlimited insurance protection, for a time, during the financial crisis. In contrast, in the case of Cyprus, authorities of the European Union initially insisted that not only large depositors, but small ones, be bailed in.

Act 3. Two final principles regarding bank failures

I am writing this post in the intermission before the final act of the Cypus banking opera, so detailed program notes will have to wait. However, it is worth calling attention to two general principles regarding bank failures and restructuring that will shape the way things will unfold in that country.

Banking losses are real losses. The first principle is that banking losses are real losses. It is easy to forget that. Descriptions of bank crises often focus on exotic financial instruments like collateralized debt obligations and credit default swaps. Some people see decreases in the value of such instruments as “only paper losses.” It seems them that it should be possible to erase all that “funny money” though some kind of accounting trick without touching the real economy.

Unfortunately, that is not how things work. Although some kinds of financial losses may net out against one another, when the dust settles, we find that there are real losses behind all the paper. For example, behind the 2008 financial crisis in the United States, Ireland, Spain and several other countries there were wild overinvestments in real estate. Houses and condos were built that no one wanted to buy, at least not for enough to pay for the bricks and the wages of the bricklayers. In Cyprus, funds supplied by bank depositors were used to buy Greek government bonds, which, in turn, were used to pay the salaries of Greek bureaucrats to do work that critics claim was unproductive and overpaid. There is no way to recapture that wasted labor now..

Because banking losses are real losses, someone always ends up bearing them. The only question is who.

One insolvent sector cannot bail out another. The game of bailout and bail-in is a matter of deciding who bears the losses of bank failure. Unfortunately, the game has a fundamental rule that one insolvent sector cannot bail out another.

For example, life would be easier if all of the losses of failed banks could be loaded on the shoulders of shareholders. Unfortunately, shareholders can bear losses only to the extent of the capital that they have at risk. If a bank were liquidated at the exact moment its capital dropped to zero, then yes, the shareholders would be the only ones hurt. In practice, however, a bank’s capital is often far below zero before it becomes obvious that it has failed. In that case, losses exceed the investment made by shareholders, so someone else must be bailed in.

Creditors, large depositors, and even small depositors are among those in line for haircuts when a deeply insolvent bank is restructured. Often, however, some or all of those parties are politically powerful enough to avoid bearing their fair share of the costs. When that happens, the country’s taxpayers are the ones who pay. The government issues bonds to fund its bailout and taxpayers bear the burden of the interest and principal for years to come.

In some cases, even the country’s government is insolvent. It lacks either the power or the will to sell the bonds or levy the taxes that would be needed for a complete restructuring.

Sometimes that leads to a chaotic outcome. For example, when a banking crisis hit Russia in 1997, the government largely stood aside. Banks simply collapsed, leaving individual depositors and many businesses with huge losses and incapable, for a time, of making any but the simplest cash payments to one another. Meanwhile bank insiders stole billions of rubles, sticking small depositors and poorly connected creditors with huge losses. It is ironic that Russia, always sensitive to others’ interference in its own domestic affairs, is now offering unsolicited advice to EU and Cypriot authorities on the proper way to conduct a bank restructuring.

Iceland provides another example of a country that could not afford to restructure its banking system, which at one time had assets more than ten times larger than the country’s GDP. When several of the largest banks failed in 2008, the government was not able to do more than offer limited protection to domestic depositors. Foreign depositors and other creditors were left to fend for themselves. The situation was not accompanied by the degree of corruption and criminality that Russia saw in 1997, but it deeply shook the Icelandic economy and left a legacy of bitter diplomatic disputes.

In Cyprus, the situation is still touch and go. One thing is sure: The total losses of Cyprus banks exceed the resources of the country’s government. If it tried to absorb the cost of a full bailout, government debt would rise to unsustainable levels approaching 200 percent of GDP. The Cypriot government has sought outside aid from the EU, the IMF, even Russia, but it may be some time before it is clear where the ultimate losses fall.

For a followup, see Further Program Notes on the Cyprus Banking Drama. For more details on bailouts and bail-ins, see this tutorial on bank failures and bank rescues.