Now Basel III has reached the crucial phase of writing the technical rules to implement the agreed principles. Many observers are worried that each round of rule-making will provide an opportunity for watering down the regulations until what is left is no more effective than Basel II was. This post looks at one key aspect of the new rules, the regulation of bank capital, as an illustration of the broader difficulties facing the effort to regulate banking risk more effectively.

Why regulate capital?

The single most important measure of banking risk is the ratio of capital to assets. Conceptually, calculating such a ratio is a simple enough. You start by adding up a bank’s assets, including all of its cash, the loans it has made, securities it owns, its office equipment and its buildings. Next you add up its liabilities, including deposits, interbank borrowing, bonds it has issued, and the rest. You subtract the liabilities from the assets and the difference is capital, which represents the shareholders’ stake in the bank.

The smaller the ratio of capital to assets, the greater the bank’s leverage. Increasing leverage concentrates the bank’s profits on a smaller base, thereby increasing shareholders’ return on equity. At the same time it exposes shareholders to greater risk. The greater the leverage, the smaller the loss of asset value required to reduce capital to zero or below. When the bank’s capital hits zero, it becomes insolvent. Normally an insolvent bank would have to cease operation and its shareholders would lose their entire investment.

In an ideal world, the government would not have to regulate leverage or capital. We could leave the implied tradeoff between risk and return to the discretion of shareholders. In the real world, however, things are not so simple. Several considerations bias banks toward greater leverage and greater risk than may be desirable from the point of view of public policy.

First, insolvent banks are not, in practice, always forced out of business, nor are their shareholders necessarily wiped out. Yes, that sometimes does happen to small banks, but shareholders of the banks that really count—the ones that are too big to fail—can expect the government to step in and protect them, at least partially, in case of insolvency. Not only shareholders but also unsecured creditors and other counterparties of banks can expect to be shielded from the consequences of insolvency. Protection from the consequences of failure increases one’s appetite for risk. Economists call that the problem of moral hazard.

Second, even if shareholders did have to worry about being wiped out by insolvency, they are not the ones who make day-to-day decisions about risks. The real risk takers, from CEOs to individual traders, may be worried less about the long-run solvency of the institution than about their own short-run bonuses and golden parachutes. They can end up faring much better than shareholders even if their bank fails. Economists call the resulting misalignment of incentives between executives and shareholders the agency problem.

Finally, neither a bank’s officers nor its shareholders may be much concerned about the damage to the economy at large that bank failures can cause. Economists refer to the impact of Wall Street failures on Main Street’s innocent bystanders as the problem of contagion. Contagion, like moral hazard, is a bigger worry when there are a few very large banks than where there are many small ones.

Concerns about moral hazard, agency problems, and contagion provide the motivation to regulate bank capital.

Which measure of capital?

In order to regulate bank capital, if first must be measured. The example given above makes that sound easy—add up assets, subtract liabilities, and you get capital. In the real world, things are not so straightforward. The closest we come in practice to the simple concept of capital is a measure called tangible common equity or TCE.

Many economists like the ratio of TCE to tangible assets as a regulatory tool, but banks tend to find it too restrictive. Basel II rules were instead based on a concept of regulatory capital that, in two respects, was both more complex and more lenient toward banks than TCE.

First, the numerator of the regulatory capital ratio was broader than tangible common equity because it included not just tangible assets like securities, but also intangible assets like goodwill and tax losses carried forward. It also counted certain hybrid capital items, such as preferred stock, along with common stock. Hybrid capital combines some properties of equity capital with some properties of debt. It does not always provide as strong a safeguard against insolvency as pure common equity.

Second, the denominator of the Basel II regulatory capital ratio consisted of risk-weighted assets rather than total assets. The idea behind risk weighting is that the probability of loss on some assets is greater than on others. For example, a mortgage loan secured by real estate might have only half the default risk of an unsecured loan to an industrial corporation. Suppose a bank has $100 million in loans of each type, giving it total assets of $200 million. Under risk weighting, the unsecured corporate loan would be counted at full value, but the mortgage loan would be assigned a weight of 0.5, so that the bank’s risk-weighted assets would be $100 + (0.5 X $100) = $150 million.

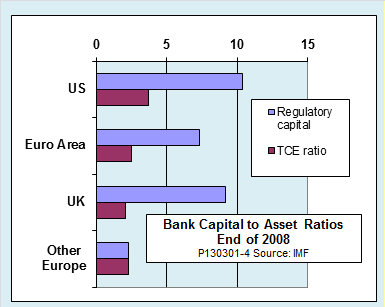

One of the major criticisms of Basel II was that regulatory capital ratios made banks look strong when in fact, they were weak in terms of their ability to withstand adverse market conditions, as measured by TCE. The following chart, based on IMF data, shows that at the time of the global financial crisis in 2008, the gap between regulatory capital and TCE was very wide, especially for banks in the United States, the UK, and the euro area.

The Basel III negotiations took many of the criticisms of regulatory capital to heart. The new regulations tighten up significantly on the treatment of intangible assets and hybrid capital, so that the numerator of the regulatory capital ratio is now much closer to TCE than it was under Basel II. However, the denominator, risk-weighted capital, turns out to pose greater problems.

A closer look at risk-weighted capital

The concept behind risk-weighting is a sound one, but the devil is in the details of how to assign the weights. Over time, the Basel process has tried three approaches.

The first, used in Basel I, assigned each asset to one of four broad categories. Loans to consumers and nonfinancial corporations had a weight of 1.0, mortgage loans a weight of 0.5, loans to financial institutions in OECD countries a weight of 0.2, and loans to sovereign governments a weight of 0. That approach failed for two reasons. One was that the weights themselves were unrealistic—loans to financial institutions and sovereign governments turned out to be far riskier than the Basel I weights implied. Another problem was that banks increased their overall exposure to risk while reducing their risk weighted assets by selectively loading up on relatively risky assets within each category. Gaming the risk weightings in that way has come to be known as regulatory arbitrage.

The second approach, tried under Basel II, was to base risk weights on the ratings that credit rating agencies assign to various assets. For example, a security with a BBB rating from Standard & Poor’s was giving a risk weight of 1.0, one with an A rating had a weight of 0.5, and one with a AAA rating had a weight of 0.2. That approach also failed. As we now know, many of the ratings issued by credit rating agencies on the eve of the financial crisis were unrealistically generous. It appears that the use of ratings for regulatory purposes made matters worse because it created pressures on agencies to purposely overrate certain securities in order to facilitate regulatory arbitrage by banks.

The third approach, first tried under Basel II and continued under Basel III, was to base risk weighted capital not on the work of credit rating agencies, but on the mathematical models that banks themselves use for their internal risk management. The idea was that instead of assigning risk weights directly, regulators would examine the banks’ own risk models and either certify them as accurate or, if not, require changes.

Controversies over risk-weighting under Basel III

The regulatory use of banks’ internal risk modeling lies at the heart of today’s controversies over the measurement of bank capital. The risk models are complex and are subject to a number of conceptual difficulties. For example, most such models make use of a technique called Value at Risk (VaR), which attempts to estimate the size of the bank’s loss for a given probability threshold over a given number of normal trading days.

The reliability of VaR has been criticized on several grounds. For one thing, VaR violates the principle of subadditivity, which means, roughly speaking, that the risk estimates for two assets held together in a portfolio may not be properly predicted by combining separately estimated risks for the two. Furthermore, for regulatory purposes, VaR suffers the more fundamental flaw that it focuses on the probability of losses under normal trading conditions, whereas regulators are more interested in “tail risk,” that is, the maximum losses that may occur under the abnormal conditions of a financial crisis.

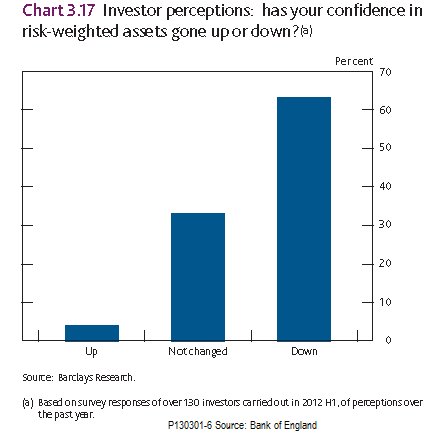

A recent report from the Bank of England uses the following terms to expresses concerns about estimates of risk-weighted assets based on banks’ internal models:

There is increasing doubt among investors over the robustness of these estimates due to their complexity and opacity. Investors find risk-weight calculations particularly difficult to scrutinise and appear to be losing confidence in the accuracy of risk-weighted assets (RWAs) as a result.

The report illustrates the loss of confidence with the following chart:

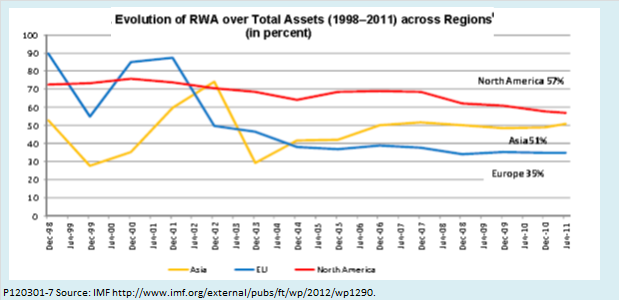

Differences in the methods used to assign risk weights affect the ratio of a bank’s risk-weighted assets to its total assets, that is, its RWA density. The lower a bank’s RWA density, the less capital it is required to hold against a portfolio of assets of a given value. As the following chart from an IMF working paper shows, RWA density varies substantially from one region of the world to another and has been trending down over time in all regions.

Charts like this one and reports that some banks have set explicit targets for reducing RWA density have raised suspicions that banks are using their internal risk modeling to game the regulations in a way that lets them reduce the total capital they are required to hold. Doing so would increase their risk of insolvency, but would also increase their return on equity as long as they remain solvent, and at the same time, could increase the bonuses of bank executives. However, trends and targets for RWA density are not by themselves conclusive.

Although the lower RWA densities could be evidence of regulatory arbitrage, there are also other possible explanations. Some of the variations can be attributed to differences from one jurisdiction to another in the way Basel regulations are implemented. Also, lower RWA densities by countries and over time could be explained by differences in the composition of bank portfolios.

One way to isolate the effects of modeling from other differences is to ask banks to run standardized portfolios through their models to see what kind of risk estimates they come up with. The results of such exercises are not encouraging. For example, a report released in February by the Bank for International Settlements found that different banks’ assessments of the amount of capital required to support a test portfolio varied by more than two to one. Another such study, cited in the Bank of England report, found variations of as much as seven to one between the most prudent and most aggressive banks’ evaluations of a test portfolio of government securities.

The bottom line

So what is the bottom line? Will Basel III regulations, when finally implemented, make banks safe enough? Even though the process is not complete, there are increasing reasons to doubt that it will. The very complexity and opacity of model-based risk weighting is a big part of the problem. As rule making moves deeper into the technical details, banks will have many opportunities to make regulations more lenient, right up to the last equation in the last subparagraph of the final regulations.

Can anything be done? Some observers, including Andrew Haldane, Executive Director for Financial Stability at the Bank of England, think that complexity itself is the problem. In a paper presented at the Fed’s Jackson Hole conference last summer, he compared tackling complex banking through complex regulation to fighting fire with fire. He sees simple ratios like TCE as both more transparent and more effective as tools of regulation.

Even Haldane’s call for simpler and more forceful regulation of risk taking suffers from the objection that it attempts to force banks, against their will, to behave more prudently. Instead, we should be directly attacking the flaws in the system—the problems of moral hazard, agency, and contagion—that encourage banks to behave recklessly in the first place. A few such efforts are already underway. For example, regulators in the United States are trying to force banks to write “living wills.” The idea is that the wills would reduce contagion effects by making it easier to wind up insolvent banks in an orderly fashion during a future crisis. Another approach, which both the EU and Switzerland are in the process of implementing, is to attack the agency problem by limiting excessive bonuses and other compensation devices that drive a wedge between the interests of bank executives and their shareholders.

Even those measures may turn out just to be more fingers in the dyke. It may be time to consider tackling the too-big-to-fail problem head on by breaking up the largest banks into smaller institutions. Meanwhile, even the moderate measures incorporated in Basel III are not scheduled for full implementation for another six years yet. Will we manage to go that long without another global crisis?

Thanks to Sarunas Merkliopas, who served as research associate for this post.

Related Slideshows:

What is Basel III and Why Should we Regulate Bank Capital?

More on Financial Regulation and Basel III: Regulating Bank Liquidity