Raising the eligibility age is a bad idea. It is based on the false premise that, since Americans are healthier and living longer, they can and should assume greater individual responsibility for their retirement. Unfortunately, the reality is that for all but the wealthiest Americans, self-financed retirement is becoming harder, not easier. A higher eligibility age would only make it still more difficult.

The real demographic realities

First, let’s take a closer look at those “new demographic realities.” Yes, Americans on average are living longer, but the increase in life expectancy has strongly favored higher-income Americans who are less dependent on Social Security to begin with. Social Security benefits account for just 18 percent of income for the most affluent fifth of retirees. By comparison, Social Security benefits contribute more than 80 percent of retirement income those in the bottom two-fifths of the distribution.

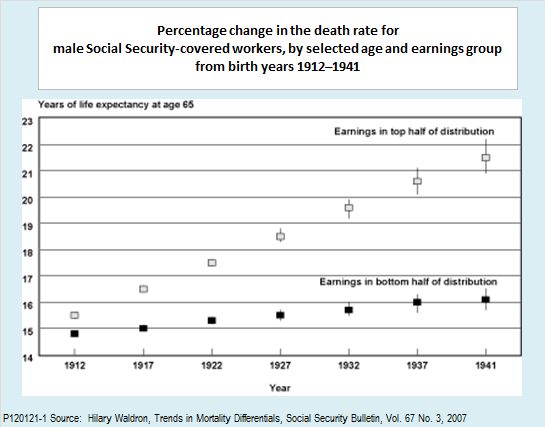

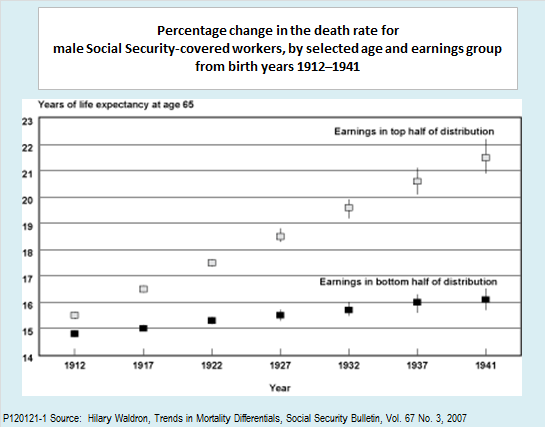

The following chart shows just how skewed increases in longevity have been. Taken from a study written for the Social Security Bulletin by Hillary Waldron, the chart compares the life expectancy at age 65 of male Social Security recipients from various birth cohorts in the top and bottom halves of the income distribution. If we compare the life expectancies of men who reached age 65 in 1977 (the 1912 birth cohort) with those who reached that age in 2006 (the 1941 birth cohort), we see that those in the bottom half of the income distribution gained just over one year of life expectancy, whereas those in the upper half gained six years.

Another way to look at the same numbers is to ask by how much a 3-year delay in eligibility reduces the number of years of benefits. The average lower-income man now receives about 14 years of benefits, if he takes full benefits starting from age 67. That would decrease to about 12 years if full benefits started at 70, a 22 percent reduction. For higher-income men, the reduction would be from about 19.5 years to 16.5, a reduction of just 15 percent.

Either way you look at it, the demographic reality is that an increase in the eligibility age would have a regressive impact on the income distribution of older Americans.

To be fair, the Business Roundtable proposal recognizes the regressive impact of raising the eligibility age and recommends offsetting it with other measures. It suggests setting a new minimum benefit that would be high enough to raise low-income recipients above the poverty line, and at the same time, means-testing benefits for wealthy recipients.

Both ideas are should be adopted on their own merits whether or not the eligibility age is changed. The real worry is that needed adjustments to minimum and maximum benefits would fall by the wayside during Congressional negotiations. Increasing the eligibility age without adjustment of benefit formulas would leave low-income retirees worse off in both absolute and relative terms.

The Financial Realities

Distributional considerations aside, raising the eligibility age for Social Security and Medicare shares a problem that is common to all proposals for shifting the burden of retirement saving from the federal budget to individuals. That is the fact that self-financed retirement has already become significantly more difficult, even without further changes to entitlement programs.

A recent policy brief from the Center for Retirement Research at Boston College succinctly outlines the reasons. Here are the main points, each of which is supported by charts and data in the brief itself:

- As noted above, life expectancy has increased. The increase is not quite as great for women as for men, but then, women lived longer and had lower average incomes to begin with, so it was already harder for them to accumulate enough wealth to last them through their retirement years.

- Changes in private pensions have made retirees more dependent on their own accumulated wealth. As recently as 1983, 62 percent of workers with pension coverage had defined benefit plans, often paying a set fraction of the retirees former salary, and sometimes protected against inflation. Such plans have now largely been replaced by defined contribution plans, under which retirees’ income depends on the earnings from funds deposited in a 401k or similar individual account. By 2010, just 19 percent of workers were fully covered by defined benefit plans, with another 13 percent having plans with mixed features. Over the same period, the number of workers covered only by defined contribution plans rose from 12 percent to 69 percent.

- Out-of-pocket medical costs have risen. For example, between 1983 and 2010, copayments under Medicare Part B, the program that covers physician services, rose from 7.5 percent of the average Social Security benefit to 17.0 percent. That increases the amount of wealth you need to accumulate by the time you retire in order to maintain a given standard of living.

- Real interest rates are falling. (The real interest rate is the nominal rate earned on retirement savings minus the rate of inflation.) In 1983, the real rate was around 8 percent. Since then it has fallen steadily. By 2010, it was effectively zero. The lower the real interest rate, the more you need to save during each year of employment, or the more years you need to work, in order to accumulate a given amount of wealth by the age of retirement. What is more, the lower the real interest rate, the lower the monthly income produced from a given accumulation at retirement.

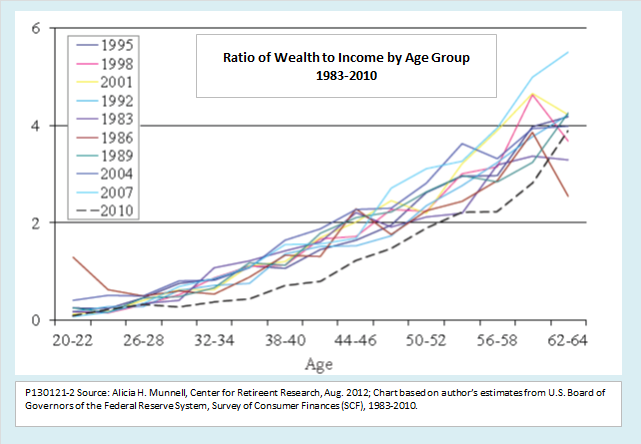

All might be well if people were increasing their efforts to save in step with the greater need to save, but that is not happening. The following chart from the CRS brief shows that from 1983 through 2007, wealth as a percentage of income showed no strong trend for any age group. That in itself is disturbing because Fed’s measure of wealth, on which the chart is based, excludes the value of defined benefit plans but includes accumulations in defined contribution plans. To maintain equal preparedness for retirement as workers became more dependent on defined contribution plans, the wealth ratio would have had to rise steadily from one survey to the next, something that did not happen.

The 2010 data are even more disturbing. Whereas the 1983-2007 data show no discernible trend, the 2010 wealth ratios lie well below the central tendency of previous experience. Notice also that the 2010 survey shows that people in their 50s were less well prepared for retirement than people already in their early 60s. The Fed conducts its survey of consumer finances every three years. If the cohort who were in their late 50s in 2010 continue to lag behind in the 2013 survey, the situation will begin to look really grim.

The Bottom Line

The bottom line is that people are more dependent on their own retirement savings now than in the past, but low real interest rates have made saving harder. At the same time, income disparities have become wider for those who are still working. Raising the eligibility age for Social Security and Medicare under these conditions is one of the cruelest budget balancing ideas out there.

We need to look for better ways to strengthen a retirement system that is not working well, and that will come under even greater strain as the ratio of retirees to workers rises. That will be the subject of the next post in this series.