In fact, it could yet be worse. The advance estimate of real GDP is notoriously subject to revision. The BEA tells us that the average revision, without regard to sign, is 1.3 percentage points from the advance to the latest estimate. A downward revision of no more than average size would put us at 0.7 percent growth, well below the anemic 1.3 percent reported in the third estimate for Q2. Of course, an upward revision is, statistically, equally likely, so let’s hope for the best.

Even as we accept 2 percent growth with relief, there are some discouraging details deeper in the tables that the BEA attaches to its press release.

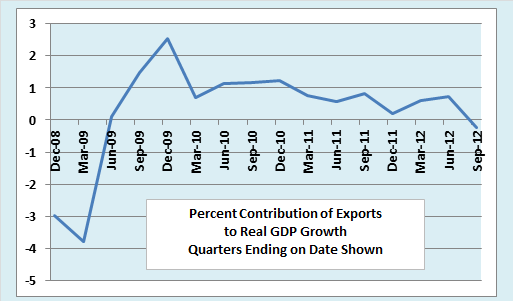

Consider exports. The recovery, such as it has been, has benefitted from solid growth of this key GDP component. Until recently, President Obama’s audacious pledge to double exports in 5 years, starting in January 2010, was close to being on track. Now, though, the BEA tells us that exports decreased at a 1.6 percent annual rate in Q3. As the following chart shows, that breaks 13 consecutive quarters in which exports made a positive contribution to the growth of real GDP. The drop in exports during Q3 occurred despite a 3-percent depreciation of the real effective exchange rate of the dollar from June to September. Even the mighty U.S. economy, it seems, is not immune from the effects of lackluster performance by its trading partners.

The data for the government sector also showed a break in trend, this one of a different kind. For eight consecutive quarters, government consumption expenditures and gross investment (GCEGI) had been pulling GDP downward—the so-call “fiscal drag.” That trend appears to have broken in Q3 2012, as the next chart shows. But is that good news or bad?

At first glance, we might expect conservatives to treat the renewed growth of government as bad news and liberals to see it as a hopeful sign. On closer examination, though, the 0.71 percentage point contribution of GCEGI to Q3 GDP growth turns out to be almost entirely due to a big jump in federal national defense consumption expenditures. That casts a different light on the data. Defense is the one area of government spending that conservatives tout as a sure-fire jobs creator. On the other hand, liberals will ask, where is the contribution to GDP growth from construction of schools, roads, and sewer systems? Where is the contribution from teachers and firemen going back to work? The answer is, nowhere. The contribution to GDP growth from state and local government was a pathetic 0.01 percent of GDP. The contribution from government investment at all levels was exactly 0.00 percent. Even the robust contribution from defense consumption expenditures is unlikely to hold up, what with the war in Afghanistan starting to wind down.

The investment data also deserve a closer look. Gross private domestic investment contributed a mere 0.2 percentage points to GDP growth in Q3 2012, the least since the -0.14 percentage points in Q1 2011. The contribution of fixed investment was even smaller, just 0.07 percent. The biggest factor determining the overall contribution of investment to GDP growth turns out to be a whopping 0.42 percentage point decrease in farm inventories—by far the largest change on that line of the accounts that we can find without going back into the historical data. Presumably, the decrease in farm inventories reflects a drought-induced sell-off of corn and soybeans that were carried over from earlier harvests. Nonfarm inventories, on the other hand, increased. Without more detailed data, it is hard to tell whether that means merchants are optimistically stocking up in anticipation of a strong Christmas rush or whether manufacturers and retailers just aren’t able to sell everything they are producing.

So, you will ask, if the line-by-line data is so full of gloomy news, where is the not-so-bad headline growth coming from? Other than those national defense expenditures, it came from personal consumption, which contributed 1.42 percentage points to Q3 GDP growth. That was up from the 1.03 percentage points of Q2, but it is far from spectacular. In fact, it is slightly less than the average for the past 12 quarters.

To put it all in World Series terms, then, here is the box score. (Note that the totals don’t add due to rounding, and that the positive figure for imports means a decrease in imports, since growth of imports counts as a negative entry in the GDP accounts.)

All in all, things could be worse. The U.S. economy continues to outperform Japan or the Eurozone. It is doing better than the UK, which grew a stronger-than-expected 1.0 percent in Q3, possibly due to a boost from the Olympics. The 2 percent U.S. growth in Q3 provides a thin but welcome cushion against the jolt we could be in for if a post-election Congress decides to let us drop off the fiscal cliff. On balance, the only fair-minded reaction to the latest GDP data is to be thankful for small favors.