We all know the story by heart. Without intervention by China’s central bank, market forces would push the value of the yuan higher, making it easier for U.S. producers to compete with Chinese goods. Instead, the People’s Bank of China (PBoC) manipulates the exchange rate by making massive purchases of U.S. dollars for its foreign exchange reserves. The result: huge current account surpluses that enrich China’s politically powerful exporters at the expense of American workers. If we just had a president with the courage to tell them to stop, we could get America moving again.

Unfortunately, although it still sounds great in a stump speech, the story may be out of date. Let’s look at it piece by piece.

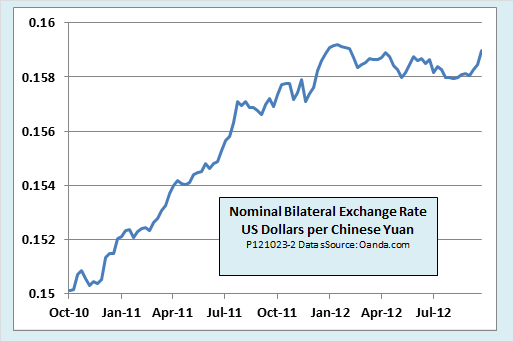

Exchange rates

First, what’s been happening with exchange rates? The first chart below shows the closely-watched nominal bilateral exchange rate of the dollar vs. the Chinese yuan (or renminbi, if you prefer the official name). For most of the past two years, the yuan has been appreciating relative to the dollar. The more U.S. importers have to pay for each yuan, the more expensive Chinese goods become for American consumers, and the cheaper American goods become for Chinese buyers. So far, so good.

The next chart shows a version of the exchange rate that is more important for China—the so-called Real Effective Exchange Rate (REER). It differs from the nominal yuan-dollar exchange rate in two ways. First, it is adjusted for differences in inflation rates between China and its trading partners. Inflation can make a big difference for international competitiveness. Second, it is a weighted average of exchange rates with the dollar, the euro, the yen, and all of China’s trading partners. The REER gives a broader picture of the overall competitiveness of the Chinese economy. It, too, has been appreciating, with some ups and downs, over much of the past several years.

Appreciation of the yuan is what you want if you are interested in selling goods to China or competing with goods from China. So far so good. But a closer reading of the charts suggests that not all is well for U.S. and European exporters and import-competitors.

First, although the yuan has been appreciating, there is good reason to believe that intervention by the PBoC has kept if from appreciating as fast as market forces would have dictated. Second, both the nominal and the real measures seem to show that the trend toward appreciation ended around the first of this year. True, both charts have a lot of volatility, so the apparent flattening of the trend could just be a statistical blip. But it could be something else. It could even mean that Chinese currency manipulators have redoubled their efforts and are no longer allowing even the gradual appreciation of previous years. For a better understanding of what is going on, we need more data.

China’s foreign currency reserves

The next chart shows what has been happening to China’s foreign currency reserves. Until mid-2011, they were rising steadily. That is the smoking gun behind the accusation of currency manipulation. Throughout all those years, the PBoC was letting the yuan appreciate only grudgingly. It was constantly fighting against market forces by buying up excess dollars and locking them up in T-bills so that they wouldn’t drive the exchange rate higher. Doing so was an expensive operation, but an effective one. China’s exporters, by all accounts, were very grateful to the PBoC for its services.

However, something odd happens after mid-2011. The steady increase in foreign currency reserves flattens out. In some months, reserves even drop a little. That is the opposite of what we would expect if the halt to the earlier appreciation of the yuan were driven by an intensification of manipulation. If that were the case, the flattening of the exchange rate curves in the first two charts would have coincided with an upturn of the reserves curve to an even faster pace of accumulation.

Instead, it looks like something else—market forces!—were what stopped the appreciation. It looks like the PBoC took its hands off the controls and the yuan just went into free flight, neither gaining nor losing altitude.

Just what are the market forces? The new trend has been going on for less than a year, so we can’t be sure. However, two prime suspects are the first trickles of capital flight from China and a slowing of demand for Chinese exports as the economies of its trading partners cool off.

China’s current account

To round out our understanding of the state of China’s currency manipulation, we need to look at one more chart. This one shows China’s current account surpluses. As everyone knows, those surpluses exploded out of nowhere in the early 2000s, reaching a towering 10 percent of GDP in 2007. The giant sucking sound of American jobs disappearing down the Chinese toilet was heard around the world, or at least, all around the Washington Beltway.

Then another odd thing happened. The surpluses began to shrink. That is what we would have expected during the global crisis of 2008 and 2009, but more surprisingly, they did not return even after the Chinese economy bounced back in other respects. Economists at the IMF, where the data in the chart come from, don’t see them coming back any time soon.

So, is China still a currency manipulator, or not?

The PBoC still buys and sells U.S. dollars on a daily basis in order to manage its exchange rate. In that sense, it could perhaps be called a “currency manipulator,” provided we were willing to apply the same term to Switzerland, Denmark, Bulgaria, and more than half of the other countries we trade with. However, if we want to use “currency manipulator” to mean something more sinister—some kind of rogue nation that steals our jobs and refuses to play by the rules everyone else has agreed to follow—then, increasingly, it looks like Chinese currency manipulation is a thing of the past.

Of course, the currency manipulation monster may not be dead, it may only be napping. It could be that Chinese leaders are so terrified at the prospect of being “labeled” by Mr. Romney that they have given up in advance, rather than risking the loss of face that would come from backing down to an American president. Or it could be, if there is no break in current trends, that Mr. Romney will be the one who suffers a loss of face on inauguration day, either quietly abandoning his pledge or making a spectacle of himself by “labeling” an obviously dead currency dragon.