The CBO’s baseline assumes no changes in current law. Paradoxically, no change in the law would mean big changes in policy. That is because we are facing the so-called fiscal cliff–a set of measures that include allowing the Bush tax cuts to expire as scheduled, making sharp cuts in Medicare payments to doctors, ending extended unemployment benefits, and allowing mandatory cuts to defense and nondefense spending to come into force. The CBO projects that those changes would shrink the budget deficit to about 4.0 percent of GDP, compared with a projected 7.3 percent for 2012. The deficit would decline to 1 percent of GDP by 2016.

The alternative fiscal scenario assumes that Congress will make the kinds of changes to current law that it has regularly made in the past. Tax cuts will not be allowed to expire (except for the temporary reduction in payroll taxes); Medicare cuts will be postponed (the so-called “docfix”); and mandatory spending cuts will be cancelled or postponed. Under those projections, the deficit for 2013 would be 6.5 percent of GDP, never falling below 4.2 percent of GDP.

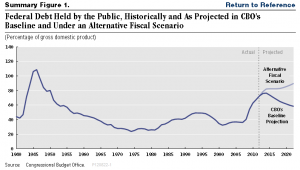

The alternative fiscal scenario—business as usual—is “too hot” in the sense that it keeps the deficit and debt on unsustainable paths. The following chart shows that under business as usual, the debt will reach nearly 90 percent of GDP in ten years; after that it would grow indefinitely. By contrast, the fiscal tightening in the baseline projection is sufficient to begin bringing the debt ratio down almost immediately.

On the other hand, the baseline projection—running the economy off the cliff—is “too cold” in the sense that it is predicted to put the economy back in recession in 2013, with an estimated 0.5 percent decrease in real GDP. That result shows up in the following chart as a temporary widening of the output gap (the gap between actual and potential real GDP) before the gap begins to narrow again.

Clearly, neither path is optimal for the economy. Pursuing the alternative fiscal scenario would mean driving the economy toward eventual default or inflationary monetization of the deficit. Those outcomes could be avoided only by undertaking fiscal consolidation measures that, because of the delay, would be even more painful than those of the dreaded fiscal cliff. On the other hand, an optimal fiscal consolidation undertaken immediately would not be so strongly front-loaded as to drive the economy into recession.

The Goldilocks outcome of fiscal consolidation that begins immediately but is phased in gradually as the economy recovers will require political compromise. The components of compromise are known to everyone:

- Tax reform that increases revenues while broadening the base and reducing the disincentives inherent in high marginal rates.

- Discipline regarding both defense and nondefense components of discretionary spending without compromising growth-enhancing expenditures like education and infrastructure.

- Reform of social security and Medicare that recognizes both budgetary and demographic realities.

Where are we headed? Will our political system deliver us a bowl of porridge that is just right, or will it, like the Mama Bear in this cartoon, throw us into the pot as Goldilocks stew?