Why We Like Policy Rules

Economists prefer rules to unlimited political discretion because they improve the chance that policy will be appropriate and timely.

Some of the reasons are technical. Lags in data collection and decision making make it hard to take monetary or fiscal policy actions until well after a problem begins to develop. In addition, it can take a year or more for the effects of interest rate or tax rate changes to work their way through the economy. These long lags create a risk that measures to restrain a boom may be implemented just as the business cycle approaches its peak, making the subsequent downturn worse. Similarly, expansionary policy applied just as the cycle approaches its trough risks overheating the economy during the subsequent expansion. The limited accuracy of economic forecasts aggravates these problems of timing. One IMF study found that forecasts made a year in advance accurately predicted a turning point in the business cycle only 11 percent of the time and only half the time three months in advance.

Other problems with discretionary policy stem from political and behavioral factors. Economists are wary of what they call time inconsistency. Time inconsistency means doing something that has short-run advantages while disregarding known long-term disadvantages. Classic examples from everyday life are taking one more drink before you leave a party or postponing a visit to the dentist until you need not just a filling, but an extraction. In economics, time inconsistency tempts policymakers to apply excessive stimulus just before an election or to postpone needed fiscal consolidation until after the votes have been cast. This problem is especially acute for the United States, with its uniquely short two-year election cycle.

When we put all three factors together—lags, forecasting errors, and time-inconsistency—discretionary policy becomes chronically destabilizing. The 1960s and 1970s in the United States were a glaring case in point. Following those two chaotic decades, when the economy swung back and forth from excessive inflation to excessive unemployment, economists began to look for rules that would improve the prospects for lasting stability.

Rules for Monetary Policy: Ryan and Inflation Targeting

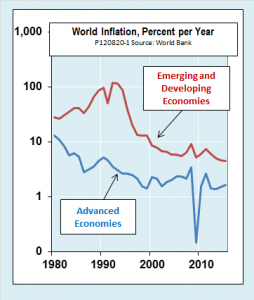

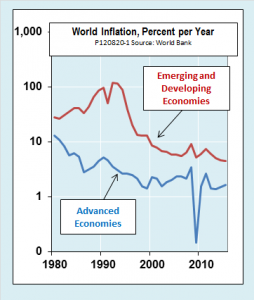

By the 1980s, inflation had become the number one threat to stability in both advanced and developing economies, as the chart shows. In that situation the idea of policy rules began to take root among the world’s central bankers in the form of inflation targeting (IT).

Under IT, monetary policy aims for a specific rate of inflation, or range of inflation, averaged over a period of a year or two. The specific measure of inflation, the time horizon, and the policy instruments used to hit the target vary from one country to another. Some countries have adopted inflation targeting as a matter of law; in others, the rule is more of a statement of intent on the part of central banks that retain broad legal discretion. No central bank aims for a zero rate of inflation. Most of them consider inflation of 2 or 3 percent to be consistent with price stability since it leaves a cushion against deflation and allows for possible upward bias of price indexes.

That brings us to Paul Ryan’s views on monetary policy rules. In 2008, he signed on to the idea of inflation targeting as the lead sponsor of HR 6053, titled the Price Stability Act. The introduction to the Act contends that inflation erodes the value of Americans’ income and savings, distorts efficient resource allocation, hampers long-term planning and raises the effective tax rate on capital, thereby impeding investment, all propositions with which most economist would readily agree.

The Act, which never came to a vote, would have required the Fed to establish an explicit definition of price stability. Since that time it has done so, declaring that rate to be 2 percent per year. It would have required the Fed to “maintain a monetary policy that effectively promotes long-term price stability,” which it has also done. Since 2008, the rate of inflation, measured by the year-on-year change in the core deflator for personal consumption, has averaged 1.6 percent, never exceeding 2.5 percent in any month or falling below 1.1 percent. Statistics for the consumer price index are almost identical. It is hard to see how even the most hardline inflation hawk could call that anything but price stability.

So, what is the big deal about Ryan’s Price Stability Act, if it would only have required that the Fed do what it has done anyhow? The answer lies not in what the Act would have added to the Fed’s mandate, but in what it would have taken away.

The Federal Reserve Act, as amended in 1977, requires that the Fed pursue “maximum employment” as a goal co-equal in importance to that of price stability. The Fed construes that to mean “maximum employment consistent with price stability,” or what economists call the natural rate of unemployment. The natural rate varies over time, in response to structural changes in the economy. The Fed currently estimates it to be in the range of 5.2 to 6 percent, which is lower than the actual unemployment rate has been at any time in the last five years. Ryan’s Price Stability Act would have abolished the employment mandate, on the grounds that multiple targets “cause confusion and ambiguity about the appropriate role and aims of monetary policy, which can add to volatility in economic activity and financial markets.”

To understand why the difference between a single and a dual monetary policy mandate matters, we need to look back at the evolution of economic thinking about inflation targeting. Many countries that adopted IT in the 1990s did so in the midst of, or following, inflation emergencies. There is evidence that the policy has worked. Its widespread adoption is, arguably, one of the reasons that world inflation slowed sharply after the mid-1990s. Since that time, however, economists have come to understand that IT does not always work so well once price stability becomes the norm.

Briefly, there are three kinds of circumstance in which single-mandate IT performs poorly:

- When the economy is hit by an adverse supply shock, such as a sharp increase in the world price of imported food or energy, strict enforcement of an inflation target requires the central bank to respond by tightening policy. Doing so reinforces the effect of the external shock; output falls sharply and unemployment rises. If labor markets are flexible enough, the economy can return to full employment as workers change jobs and nominal wages fall. If not, adjustment can be slow and painful. Many economists argue that under these circumstances, partial accommodation can spread the impact of supply shocks more evenly between inflation and unemployment.

- During a productivity-led boom, real output can sometimes grow faster than the rate that is sustainable in the long run, yet still not cause inflation. If so, the pace of money growth needed maintain price stability may be sufficient to touch off asset bubbles. When those bubbles burst, they can send the economy into a deep recession. Arguably, it would be better to begin to tighten policy even in the absence of excessive inflation.

- During the recovery from a deep recession, the condition the U.S. economy is in now, inflation can remain at or just below a reasonable target value while unemployment remains high. When that happens, strict adherence to an inflation target may unnecessarily prolong the recovery.

For all of these reasons, single-mandate inflation targeting has lost its luster. Although it may be premature to announce the death of IT, as Jeffrey Frankel did recently, economists are thoroughly rethinking it. Here are some of the leading alternatives:

- A Taylor Rule is a formalized version of a dual mandate like the informal one under which the Fed now operates. Under a Taylor rule, a simple set of equations would guide the central bank to raise or lower interest rates when either inflation or real output moved away from its target value.

- Flexible inflation targeting is a less formalized version of the same thinking. Inflation remains the primary policy target, but the central bank is free to act as needed in circumstances like supply shocks, productivity booms, or asset bubbles.

- NGDP targeting rolls the targets for inflation and real GDP into one by targeting the growth of nominal GDP. NGDP targeting would automatically allow accommodation of supply shocks, allow temporarily low or even negative inflation during productivity booms, and justify much more strongly expansionary monetary policy during a sluggish recovery.

In the light of all of the above, Paul Ryan’s thinking on monetary policy, as reflected in his Price Stability Act, begins to look less like a bold new vision for the future and more like something left over from the 1990s.

Rules for Fiscal Policy: Ryan and the Balanced Budget Amendment

Ryan’s views on monetary policy rules are not really unorthodox—it is just that they are yesterday’s orthodoxy. His views on fiscal policy, by contrast, depart far from mainstream thinking. If implemented, they could be dangerously destabilizing.

Perhaps the best indicator of Ryan’s views on fiscal policy is his vote in the House last November against a proposed balanced budget amendment. The reason? He feared that the House version of the amendment would not constrain federal revenues and outlays tightly enough. He appears to have been holding out for the much tougher Senate version of the amendment that had been put forward earlier in the year by Senators Orin Hatch and Mike Lee. A Senate vote on Hatch-Lee fell short later in the year, but the proposal was still alive at the time Ryan cast his vote in the House.

Hatch-Lee would have capped federal tax revenues at 18 percent of GDP and required the budget to be in balance every year. As I detailed in an earlier post, the amendment had a number of flaws, of which the most important was the inherently procyclical nature of any rule requiring an annually balanced budget.

The problem with such a rule is that tax revenues rise and fall with the business cycle. When the economy enters a recession, revenues decrease. To keep the budget in balance, spending would have to be cut to match the decrease in revenue. That, in turn, would cause a further contraction of the economy, further reducing revenue, and so on. It would put the economy into the same kind of austerity-driven death-spiral now afflicting Greece and Spain.

Although it is not a good idea to try to trim expenditures to match revenue every single year, more sophisticated rules can avoid the trap of procyclicality. Many countries now have fiscal policy regimes that guarantee long-run balance of the budget while avoiding the destabilizing effects of balancing it annually.

One approach requires annual balance of the cyclically adjusted budget. That means structuring tax and spending laws so that revenues equal spending when real output is at its potential level. During a recession, tax revenues decrease and outlays for unemployment compensation and other forms of income support automatically rise. The resulting deficit moderates the depth of the downturn. During an expansion, taxes increase and outlays for transfer programs decrease. The resulting surplus helps avoid dangerous booms and bubbles. The budget remains in balance over the business cycle. Total government debt remains sustainable and, depending on the exact parameters of the budget rules, can be made to decrease gradually over time. Chile, which is in many ways the most stable and prosperous country in Latin America, uses this kind of fiscal rule.

A different approach requires that the budget be in balance, on average, over the business cycle, but allows countercyclical fiscal policy, within strict limits, on year-to-year basis. Sweden introduced such a rule to get itself out of a budget crisis in the early 1990s. Since then, under both Social Democratic and center-right governments, deficits have remained under control and the debt ratio has fallen steadily.

The Bottom Line

Paul Ryan was right to point out, in his Price Stability Act, that inappropriate rules or excessive policy discretion can “add to volatility in economic activity and financial markets.” The problem lies with the specific rules he has supported. Single-mandate inflation targeting and an annually balanced budget are clear enough in their intentions, but economics is not about intentions. It is about tracing the consequences of policy, both direct and indirect, both intended and unintended. When we do that, we see that Ryan’s proposals would increase the very kinds of instability and volatility that he claims he wants to avoid..

Related posts

NGDP Targeting is the Natural Heir to Monetarism

Yes, the U.S. Needs Fiscal Policy Rules, but Not Hatch Lee

How Intelligent Budget Rules Help Chile Prosper: Lessons for the United States

How Smart Budget Rules Keep Sweden’s Budget in Balance