Poland’s Failed Fixed Exchange Rate

All economies that made the transition from the Soviet-style centralized-administrative model to a market economy in the early 1990s experienced significant inflation. The peak inflation rate for countries in the short-lived ruble area exceeded 1000 percent. Poland’s inflation, which peaked at over 500 percent in 1990, was the highest among transition economies outside the ruble area.

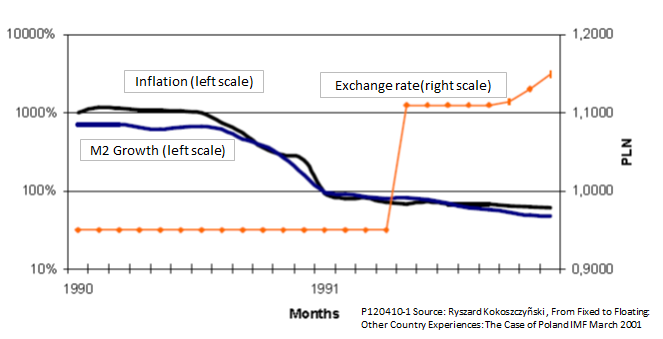

To bring inflation under control, Poland, like several other transition economies, turned to a fixed exchange rate. Unlike the neighboring Baltic states, however, Poland did not institutionalize the fixed rate through a currency board or similar arrangement. With neither a strong institutional framework nor large foreign currency reserves, its fixed-rate disinflation strategy lacked credibility. We can read the failure of the fixed-rate policy from the following chart, adapted from a paper that Ryszard Kokoszczynski prepared for a 2001 IMF seminar.

The first thing that stands out is that the inflation rate did not immediately decrease, as it has done in countries that undertook more firmly anchored exchange-rate based stabilization programs.

Second, during most of the period the chart covers, the inflation rate exceeded the growth of the M2 money stock. A well-known rule of thumb tells us that the rate of inflation is equal to the rate of money growth plus the rate of increase of velocity minus the rate of growth of real GDP. Real GDP was falling in 1990 and 1991 at a rate of about 7 percent per year, enough to explain only a small part of the gap between the inflation rate and the money growth rate. The remainder of the gap must be attributed to an increase in velocity, which in turn implies a reduction in the willingness of households and firms to hold the domestic currency as a store of value. When people are spending their domestic currency as fast as they earn it, or exchanging it for foreign currency, we have a sure sign that the exchange rate regime lacks credibility. In contrast, a rapid decrease in velocity is the hallmark of success for a well-executed exchange-rate based stabilization policy, for example, that of Bulgaria in 1997.

The third thing we see from the chart is that those who doubted the sustainability of the fixed exchange rate were vindicated. In May 1991, the government sharply devalued the zloty and switched the peg from the U.S. dollar to a five-currency basket. By October, the end had come for a fixed exchange rate that everyone had to admit was not working,

From Fixed Rate to Crawling Peg and Crawling Band

Starting in that month, the Polish authorities replaced the fixed exchange rate with a crawling peg. Under that system, the exchange rate of the zloty was fixed in relation to the five-currency basket on a day-to-day basis, but at a rate that steadily depreciated. The rate of depreciation, initially 1.8 percent per month, was kept below the prevailing rate of inflation and gradually slowed as the economy stabilized.

As the next chart from Kokoszczynski’s paper shows, the crawling peg was an improvement over the fixed exchange rate, but it still did not provide enough flexibility. Trade imbalances and limited reserves forced two unplanned devaluations, one of 12 percent in February 1992 and one of 8 percent in August 1993. In May 1995, in an effort to provide greater room for maneuver, the Polish authorities changed from a crawling peg to a crawling band. Under the new policy, the exchange rate was allowed to vary plus or minus 7 percent around a central target rate that continued to depreciate according to an announced schedule, which by that time was 1.2 percent per month.

This second chart shows a significant gain in credibility. Soon after the crawling peg came into effect, the rate of inflation began to fall below the rate of money growth, indicating a slowing of velocity. The gap between inflation and M2 growth widened during the crawling band phase. By 1998, inflation finally dipped below 10 percent.

Notice also that the crawling band coincided with the beginning of two-way variability of the exchange rate. Two-way variability is important because it deprives speculators of a destabilizing one-way bet on unplanned changes in the target rate. By 1995, Poland was experiencing strong financial inflows, so much of the pressure on the zloty was in the direction of appreciation. In December 1995, both the upper and lower limits of the band were adjusted in the direction of appreciation, but after that, the exchange rate moved up and down within the band as it became gradually wider. The official end of the crawling band policy in April 2000 was a non-event; by then the zloty had been floating freely within the corridor for more than a year.

From EU Accession to the Global Crisis

After 2000, Poland followed a policy that combined a floating exchange rate with inflation targeting. From 2001 to 2011, inflation was respectably moderate, averaging just under 3 percent per year. The floating exchange rate largely absorbed external shocks and changes in financial flows without undue damage to the real economy.

The benefits of the floating exchange rate are starkly evident if we contrast Poland’s performance since its accession to the EU with that of nearby Latvia, which retained a fixed exchange rate. As the next chart shows, both countries experienced significant real appreciation of their currencies following accession. In both cases, the real appreciation was due, in large part, to strong financial inflows.

The real appreciation manifested itself differently in floating-rate Poland than in fixed-rate Latvia. In Poland, it took place almost entirely through nominal appreciation of the zloty while inflation remained moderate, as shown in the next chart. In Latvia, where the lats was firmly pegged to the euro, real appreciation could express itself only through inflation.

Both Poland and Latvia prospered in the years immediately following accession, but their paths diverged dramatically when the global crisis hit in 2008. From July 2008 to March 2009, the nominal exchange rate of the zloty depreciated from 3.25 to 4.26 per euro. With inflation below 5 percent, that meant a sharp real depreciation. The real depreciation was one of the major factors that allowed Poland to make it through 2009 without a recession, the only EU member to do so.

The the relatively stable path of real output in Poland contrasts with the very different experience of Latvia. In Latvia, the onset of the crisis slowed the rate of inflation, but did not immediately reverse it. As a result, Latvia’s real exchange rate kept on rising through the end of 2008. Even after the price level began to fall and Latvia’s chosen policy of internal devaluation began to take hold, real depreciation was much more gradual and much more moderate than in Poland. The sluggish response of the real exchange rate amplified the impact of the crisis on Latvia’s real economy, which, as this last chart shows, ended up experiencing the largest real GDP decrease of any EU member in 2009.

The Lessons

What lessons can we draw from Poland’s experience that are relevant to countries now facing possible exit from the Euro?

The first lesson is that fixed exchange rates aren’t for everyone. They make it more difficult to manage external shocks, whether they originate in the financial or the real sector.

As far as the peripheral euro countries go, one could perhaps say that was something they should have kept in mind before joining the currency union in the first place, but we can’t put the blame entirely on them. European leaders who sold them on the idea of the euro did not go out of their way to present a balanced picture of its costs and benefits. If someone was sweet-talked into a bad marriage, should we later condemn them for seeking a divorce?

Really, the lesson that fixed exchange rates are not for everyone is one the core euro countries should heed as well as the peripheral ones. If fixed exchange rates aren’t for everyone, what sense is there in the mandate for all EU members to join the euro, as all except Denmark and the U.K are sooner or later supposed to do? One would think the euro core countries would realize that expanding the currency area to others for whom it is structurally unsuited would weaken the common currency, not strengthen it.

The second lesson is that there is more than one way to leave a fixed exchange rate. A cold-turkey float is not the only one. Argentina took that path in 2002 and got away with it, but it may not always be the best alternative. Das and Roubini , cited earlier, have been promoting the idea of an exit strategy using an exchange rate corridor that would widen gradually as inflation and currency fears recede. Poland’s experience with its crawling band provides a practical example of that strategy: a gradually widening corridor that created room for two-way movement of the exchange rate and, eventually, an uneventful exit to a free float.

The third lesson is that if a country chooses any kind of managed exchange rate regime, even as a transitional measure, credibility matters. That is true whether we are talking about membership in a currency area, a conventional fixed exchange rate, or an expanding corridor. Lack of credibility led to the failure of Poland’s initial fixed rate, and the establishment of credibility to the success of its crawling band.

Das and Roubini propose that the remaining core members of the euro, acting through the European Central Bank, should help provide the credibility. The idea is economically sound, and it seems only fair, too, that the core countries take responsibility for having seduced unsuitable partners into the euro in the first place. The hard part, as with all divorces, is whether psychology, politics, and personalities will allow such a rational and amicable separation.