Growth was revised upward for all major sectors of the economy.

- The contribution of consumption to the quarter’s growth was revised up to 1.52 percentage points form 1.45 in the advance estimate. Strong sales of motor vehicles led the way.

- Investment growth contributed 2.42 percentage points to growth, rather than the 2.35 points reported earlier. The growth of private inventories accounted for the biggest share of the increase in investment. The rapid increase of inventories appears at least in part to have been a rebound after the strong decrease in the previous quarter.

- The government sector continued to shrink. Total government spending made a negative .89 percentage point contribution to growth in the quarter. The decrease in government spending was broadly based, affecting both defense and nondefense components of federal spending as well as state and local government.

- Export growth remained strong, although it contributed slightly less than reported in the advance estimate (.59 percentage points rather than .64 percentage points). However, imports were revised downward by slightly more, so on balance, the contribution of net exports to real GDP growth was a negative .06 percentage points rather than a negative .11 percentage points.

Nominal GDP grew at a 3.9 percent annual rate in Q4, up from 3.3 percent reported in the advance estimate. That included 3.0 percent real growth and an implied 0.9 percent inflation. The upward revision will be somewhat reassuring to NGDP targeters. The CBO potential real GDP series has grown at an average rate of about 2.3 percent over the past 10 years, although it may not be growing that fast now. Adding the Fed’s 2 percent inflation target brings that up to 4.3 percent. It would appear that NGDP targeters could still make a case for a somewhat more expansionary policy stance.

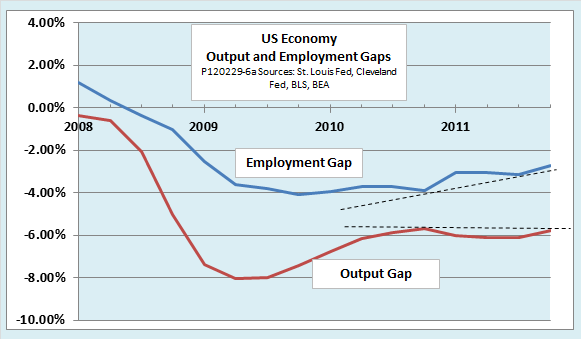

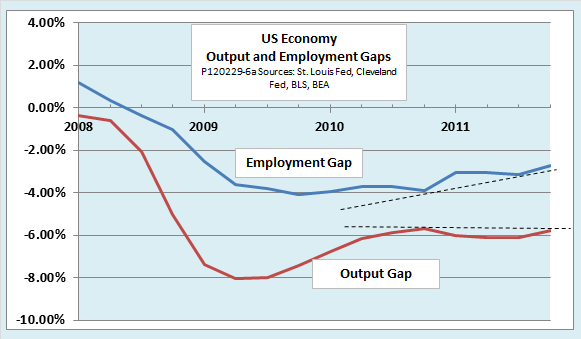

It is important to remember that potential real GDP is not an observable variable. There has been considerable recent controversy as to whether the widely-publicized CBO estimate overstates potential real GDP, and therefore also the output gap between current and potential real GDP. (See this post by Menzie Chinn for an excellent summary of the methodological issues and links to some recent Economonitor commentary.) With that in mind, it is interesting to compare the estimated output gap with the employment gap, as in the following chart:

The output gap in the chart is the difference between quarterly real GDP and the CBO estimate of potential real GDP, stated as a percentage. Similarly, the employment gap is the difference between the unemployment rate in the middle month of each quarter and an estimate of the natural rate of unemployment supplied by Murat Tasci of the Cleveland Fed. (See this paper and others Tasci has written on the topic for a discussion of his methods.)

What we see is that although both the output gap and the employment gap remain wide, the latter has been closing more rapidly over the past year. One interpretation would be that the persistently bad job market and unusually high rates of long-term unemployment are causing unemployed workers to take jobs that have relatively low pay and contribute relatively little to GDP. If that is the case, the employment gap would disappear long before the output gap did, which is just another way of saying that CBO-based output gap is, after all, overstated.

The bottom line: The economy is getting better, but it still has a long way to go. It is not hard to make a case that it would be premature to tighten monetary or fiscal policy at this point. Looking farther ahead, it appears that the economy may be gradually approaching a “new normal,” with unemployment settling down to a natural rate of around 6 percent and real output growing along a path significantly below its pre-recession trend. If that is the case, we will eventually reach a point where continued efforts to push the economy back to the low rates of unemployment and the real output trend that prevailed in the mid-2000s would do more harm than good.