While the headline all-items CPI fell, measures of underlying inflation remained in the very low positive range. The core CPI from the BLS, which covers all items less food and energy, rose at a 2.10 percent annual rate in November, up from 1.69 percent in October. The Cleveland Fed’s 16 percent trimmed mean inflation rate came in an an annual rate of 0.99 percent for November, down a little from 1.36 percent in October.

All of these are very low numbers to be seeing at a time when the world economy is slowing. The EU, by all indications, is already in recession and is likely to stay there next year, even if the latest euro rescue plans succeed. At the same time, the Chinese economy is slowing as that country’s housing bubble unwinds, exports slow, and direct foreign investment turns negative. Brazil has just reported its first quarterly GDP decrease in several years. India’s central bank has put interest rates on hold, despite high inflation, as industrial output falls. The U.S. economy itself, according to Q3 data, is growing just enough to prevent its large output gap from getting even larger.

It is interesting to compare the latest U.S. inflation data with those from November 2007, the last month before the economy entered its previous recession. Headline inflation that month was 10 percent and core inflation 3.7 percent. The economy thus entered the last recession with enough inflation momentum to keep the CPI rising through the first half of 2008. Falling energy prices pushed headline inflation into negative territory in the second half of 2008, but during the whole recession, there was only one month of negative core inflation. There were six scattered months of zero core inflation, but no more than two in a row. Deflation was never a real threat.

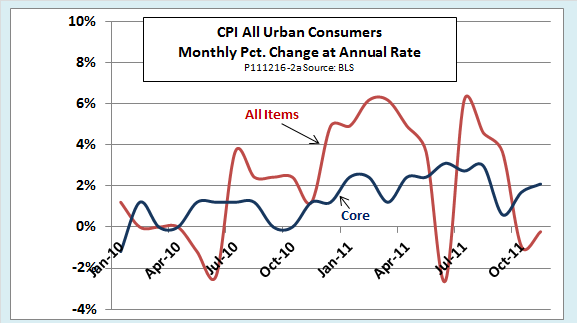

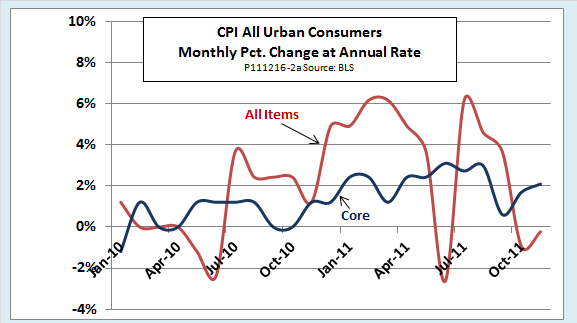

There would be a much thinner cushion of inflation momentum to protect the economy now if global troubles were to derail the weak U.S. recovery. As evidence that the economy is still far from deflation, some people might point to the fact that annual average inflation rates are still running above the Fed’s implicit 2 percent target. The all-items CPI rose 3.4 percent from November 2010 to November 2011, and the core rate rose 2.2 percent over the same period. However, those are backward-looking indicators. Over the last several months, reported year-on-year inflation data has been held above the corresponding annualized monthly numbers because they were rooted in very low base rates of 2010. (See the following chart for annualized monthly figures for the headline and core CPIs.)

Beginning with next month’s report, the year-earlier base for the y-o-y CPI will jump upward. The November 2010 figure that was dropped from the y-o-y calculation for this month was 1.21 percent, below the November 2011 rate. Next month, the figure dropped will be the 4.91 annual rate of increase recorded in December 2010, which will surely be higher than that for December 2011.

Furthermore, when the U.S. economy entered recession at the end of 2007, the Fed had a lean balance sheet and a full arsenal of monetary policy tools. Although it may be an exaggeration to say that the Fed is out of ammunition, the current near-zero interest rates and a balance sheet swollen by two rounds of quantitative easing clearly give it a lot less room for maneuver. Needless to say, stocks of fiscal munitions are even lower.

It is too early to say the economy is doomed to enter a deflationary free fall. We still can hope that “it” will still not happen here. The probability is growing, though, that the next few months of inflation data will put deflation worries back on the national agenda.