The story starts back in 1997, when Tony Blair was new to the job of prime minister. The euro was still three years away from realization, but already Blair was an enthusiast. Brown was skeptical, but he had a problem. Political solidarity required him to support the euro in principle, but his stronger sense of economic reality made him realize that it was a bad idea for the UK. His solution was to endorse the euro subject to the following five tests, which together were vague enough and tough enough that they could never be fully met:

- Is there sufficient convergence between the British economy and that of the euro area, especially with regard to interest rates and the business cycle?

- Would membership in the euro give the UK enough flexibility to cope with a major crisis?

- Would the euro stimulate inward investment?

- Would it help the financial services industry?

- Would it help growth and job creation?

Of the five tests, the last three turned out to be makeweights. At one time or another, Brown conceded that if the first two conditions were met, then the third, fourth, and fifth would hold as well. He even saw some (but never enough) convergence in interest rates and the business cycle. That left flexibility as the key consideration.

Here is how Brown put the matter in a key 2003 speech: “The issue at the present time is, however, being sure that there is structural convergence that is sustainable for the long-term, and we also have to be sure that, if real interest rates or business cycles do diverge, Britain will have the necessary flexibility to sustain stability, growth and employment. . . We do not know whether or how shocks will occur but there are risks.”

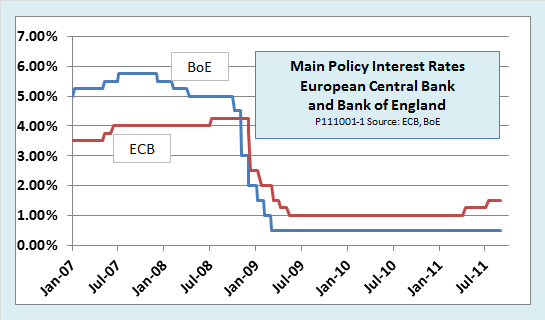

Presciently, he identified the housing market and inflation as two of the greatest risks. Fast forward to 2007. The UK housing bubble collapsed, bringing down several financial institutions, the first of which, in the fall of 2007, was Northern Rock. It soon became evident that the crisis was world wide. With the British financial system teetering on the brink, how did the government use its precious flexibility? The answer is clear from the following charts, which show the development of interest rates, inflation, and exchange rates.

First, interest rates. Within the euro, there can be only one policy rate, set by the European Central Bank (ECB). Until the Greek sovereign debt crisis began to raise the risk of sovereign default, other major interest rates moved closely together throughout the euro area. As the chart shows, the Bank of England (BoE), which had held interest rates above those of the ECB going into the crisis, began lowering them at the end of 2007. At first the easing was gradual, but it accelerated toward the end of 2008. By November of that year, British rates were below those of the euro area, where the ECB was still treating inflation as the main threat.

The decrease in British interest rates, together with other factors, soon began to affect exchange rates. From 2007 to 2009, the nominal exchange rate fell from 1.4 euros per pound almost to par. It has recovered only slightly since. Needless to say, if the UK had joined the euro before the crisis, the nominal exchange rate could not have changed at all.

The decrease in British interest rates, together with other factors, soon began to affect exchange rates. From 2007 to 2009, the nominal exchange rate fell from 1.4 euros per pound almost to par. It has recovered only slightly since. Needless to say, if the UK had joined the euro before the crisis, the nominal exchange rate could not have changed at all.

Policy flexibility also manifested itself in the evolution of the British inflation rate relative to that of the euro area. Both the BoE and the ECB profess adherence to an inflation target of 2 percent, but the ECB has pursued its target much more aggressively. The BoE, in contrast, has allowed lower interest rates and a weaker pound to push inflation higher throughout the crisis. Some British inflation hawks have been alarmed, but Mervyn King, Governor of the Bank of England since 2003, has justified the stimulus associated with above-target inflation, first to combat the immediate financial crisis, and more recently, to offset fiscal austerity. Over at the ECB, Jean-Claude Trichet has been much more of a hard-liner on inflation. In a controversial move, he even raised euro interest rates when inflation crept above the 2 percent target in 2011, despite the threat that the sovereign debt crisis might send the euro area back into recession.

Policy flexibility also manifested itself in the evolution of the British inflation rate relative to that of the euro area. Both the BoE and the ECB profess adherence to an inflation target of 2 percent, but the ECB has pursued its target much more aggressively. The BoE, in contrast, has allowed lower interest rates and a weaker pound to push inflation higher throughout the crisis. Some British inflation hawks have been alarmed, but Mervyn King, Governor of the Bank of England since 2003, has justified the stimulus associated with above-target inflation, first to combat the immediate financial crisis, and more recently, to offset fiscal austerity. Over at the ECB, Jean-Claude Trichet has been much more of a hard-liner on inflation. In a controversial move, he even raised euro interest rates when inflation crept above the 2 percent target in 2011, despite the threat that the sovereign debt crisis might send the euro area back into recession.

The combined effect of flexibility in interest rates, nominal exchange rates, and inflation can be seen in one final indicator, the real effective exchange rate. The REER is a measure of a country’s competitiveness in international trade. It is a weighted average of exchange rates relative to all of a country’s trading partners, adjusted for the effects of inflation. Either a depreciation of a country’s nominal exchange rate or an increase in its inflation rate can cause the REER to depreciate.

The combined effect of flexibility in interest rates, nominal exchange rates, and inflation can be seen in one final indicator, the real effective exchange rate. The REER is a measure of a country’s competitiveness in international trade. It is a weighted average of exchange rates relative to all of a country’s trading partners, adjusted for the effects of inflation. Either a depreciation of a country’s nominal exchange rate or an increase in its inflation rate can cause the REER to depreciate.

The following chart shows that since 2007, the UK’s REER has depreciated sharply relative to that of the euro area. That is hardly surprising, since, as shown above, the pound has depreciated relative to the euro in nominal terms and UK inflation has been higher than that of the euro area.

This time additional countries have been brought into the picture to emphasize a broader point about the importance of policy flexibility: Any given international crisis is bound to affect various countries differently, depending on structural characteristics and the state of their economies when the crisis begins, so policy reactions should be able to differ as well.

This time additional countries have been brought into the picture to emphasize a broader point about the importance of policy flexibility: Any given international crisis is bound to affect various countries differently, depending on structural characteristics and the state of their economies when the crisis begins, so policy reactions should be able to differ as well.

Consider, first, euro members Germany, France, and Italy. Germany has been the engine of the euro area during the crisis. France has held up pretty well, although its position is more vulnerable. Italy, however, entered the crisis with a weak economy, poor competitiveness indicators, and a public debt over 100 percent of GDP. Despite these differences, the REERs of the three euro members have marched in lock step. (The slight divergence of REERs stems partly from small differences in inflation rates and partly from differences in the weights assigned to the countries’ trading partners.) Italy, which could desperately use a real devaluation, cannot get it. Germany, meanwhile, free-rides on the euro to maintain an undervalued exchange rate that allows it to challenge a far larger China for world export leadership.

Contrast the behavior of euro REERs with those of non-euro EU members UK, Sweden, and Poland.

The British pound, as the chart shows, began to depreciate the soonest. That is as one would expect, since its economy was hit hard in the earliest phases of the crisis.

Sweden, whose financial system was neither as large nor as vulnerable going into the crisis, did not experience real depreciation so early. However, as the crisis began to hit its real GDP in 2009, the Swedish REER was allowed to depreciate substantially. Swedish real GDP fell by 5.3 percent in 2009, more than the average for the euro area, but due in part to the weakening of its exchange rate, it has recovered more rapidly than the euro area average since that time.

Poland’s case is different still. When the global crisis hit, Poland was still enjoying the post-accession boom that affected all the formerly Communist countries that entered the EU in 2004. A natural part of the convergence process for all of them was a strengthening of real exchange rates. In fixed-rate countries like the Baltic states, real appreciation manifested itself through inflation well above the euro area average. In floating-rate countries like Poland and the Czech Republic, real appreciation mainly took the form of nominal appreciation without a large inflation differential.

When the crisis struck, the payoff to exchange rate flexibility was dramatic. Poland’s nominal rate fell precipitously, allowing it to maintain competitiveness and helping to make it the only EU member not to experience a recession. Meanwhile, its fixed-rate Baltic neighbors were pushed into policies of “internal devaluation,” the term given to the slow and painful process of REER readjustment through deflation of the price level.

The bottom line: Gordon Brown was right. When crisis strikes, flexibility pays off. If Blair had succeeded in bringing the country into the euro before 2007, the effects could have been catastrophic both for the UK and for the euro area as a whole. Without the safety valve of flexible interest rates, inflation, and exchange rates, the overgrown, risk-addicted British financial system could very well have crashed as badly as Ireland’s did. Even the mighty Germans could not have bailed it out, and the euro might already be history.

Of course, the British economy is not out of the woods yet. It managed to weather the immediate shock of the global financial crisis, but now its coalition government has embarked on a new adventure of fiscal consolidation through austerity. The experiment may or may not succeed. Whatever the outcome, Prime Minister David Cameron will owe the greater success or lesser failure of his program to the flexibility preserved by his appalling, brutal, volcanic, and defeated predecessor.

Surely, Mr. Brown deserves at least a little statue, does he not?