Last year the budget deficit remained stable at 3 per cent of GDP, while the 2.2 per cent primary surplus was the largest in the Eurozone, along with Germany’s. Yet public debt rose from 127.0 to 132.6 per cent of GDP (Banca d’Italia 2014b). In practice, Italy has to borrow even if it does not run any net-of-interest deficit. In broad numbers, every year it spends 800 billion euros a year, borrows 50 billions to cover deficits due to 85 billions in interest on a 2 trillion debt, and borrows 400 billions to roll over its maturing debt. By raising taxes to cut the deficit, Italy’s GDP has stopped growing in nominal terms six years ago, while debt has kept growing since.

Even if this situation were financially sustainable, it makes it impossible for Italy to grow out of its problems. The economy is straightjacketed. Creating new jobs and reabsorbing mass unemployment will not be achieved only through modest improvements in exports and timid jumps in expectations. Structural reforms (such as in justice, education, governance, and doing business), while necessary to modernize the country and improve the economic environment, won’t jumpstart any recovery any time soon, if at all.

Which options for Italy?

Which policy options are available for the country to exit stagnation and accelerate recovery?

The recent ECB move amounts to too little too late. The hope that negative interest rates and incentives to lending provide stimulus to the crisis economies of the Eurozone does rest on weak premises. Negative interest rates are a tax on bank reserves. If the Danish experience in this regard is of any guidance, it suggests that deposit and lending volumes might even be falling after the introduction of negative rates (Coppola 2014). In fact, the Danish policy was successful since its objective was not to increase lending, but precisely the opposite. The Danish central bank imposed negative rates to relieve pressure on the currency to appreciate and to stem capital inflows (Stella 2014).

More broadly, it is hard to believe that the ECB decision will alter the economic outlook that so far has caused Italian banks and firms to stay away from credit. By the way: why would anyone take on new risks when wealth can be protected from negative rates simply by hoarding cash?

(Buiter (2009a, b) identifies the conditions for effective removal of the zero lower bound: cash would have to be suppressed or taxed (stamped), or a new currency would have to replace the one in circulation at a depreciated exchange rate vis-à-vis the unit of account, say, the dollar, which would remain the numéraire. Kimball (2013) proposes to remove the zero lower bound by demoting paper currency from its role as unit of account. Paper currency could still continue to exist, but prices would be set in terms of electronic dollars (or electronic euros or yen), with paper dollars potentially being exchanged at a discount compared to electronic dollars. Of course, none of the above conditions are contemplated in the Eurozone as the ECB is introducing negative interest rates.)

Alternatively, the ECB could opt for boosting inflation through quantitative easing (QE). As QE in Eurozone countries would arguably be less effective than in the US or UK, due to their different financial market structure (Odendahl 2014), the ECB should either pursue a higher inflation target, tie QE to unemployment or economic growth, or commit to “price-level targeting”, say, by setting a 2 per cent inflation target on average for the foreseeable future, implying that the ECB would have to induce higher-than-targeted inflation to compensate for any target undershooting. Also, the ECB should be willing to supply whatever reserves it takes to reach the given target. None of these options seem to rank high among the preferences of the Eurozone policy elites.

Italy, therefore, cannot expect much inducement from monetary policy. A radical alternative would be for Italy and all other Eurozone highly indebted countries to regain fiscal space through debt monetization by the ECB, as suggested by Pâris and Wyplosz (2013, 2014). But again, while such measure would set these countries for a fresh new start, allowing their budgets to be less austere and yet compliant with the euro fiscal rules, there does not seem to be political appetite for it. Even less palatable are the overt monetary financing of government deficit proposals reviewed by Woodford (2012) and Turner (2013), and variously articulated by others (see Bossone 2013a).

Short of adequate monetary and fiscal levers, the option left to Italy is for the government to draw on what Germany did in the ’30s to fight the Great Depression.

German (successful) heterodoxy in the ’30s

Frustrated with the extremely painful deflation imposed by the domestic policy response to the Great Depression, Germany in the early thirties was in an even worse situation than today’s crisis Europe: financial market collapse, large external debt, stagnating demand, and mass unemployment. Hjalmar Schacht, then president of the central bank and minister of economics, understood that the country needed a large public spending program financed by central bank credit. But how could he avoid losing control of monetary policy?

Schacht established the Metallurgische Forschungsgesellschaft (Mefo). This company, which had no employees, equipment, organization or operations, could stipulate public procurement contracts and could pay contractors by issuing state-guaranteed bills of exchange at variable maturities. These so called Mefo bills could be discounted at the banks into Reichsmark on demand, although the Raichsbank could temporarily suspend convertibility on monetary policy considerations. Large emissions of Mefo bills paid for actual deliveries of goods. The bills circulated as money and succeeded in revitalizing the economy. Output rebounded, full employment was attained, and the new fiscal revenues enabled the State to redeem maturing Mefo bills (see Stucken 1953, and Schacht 1967).

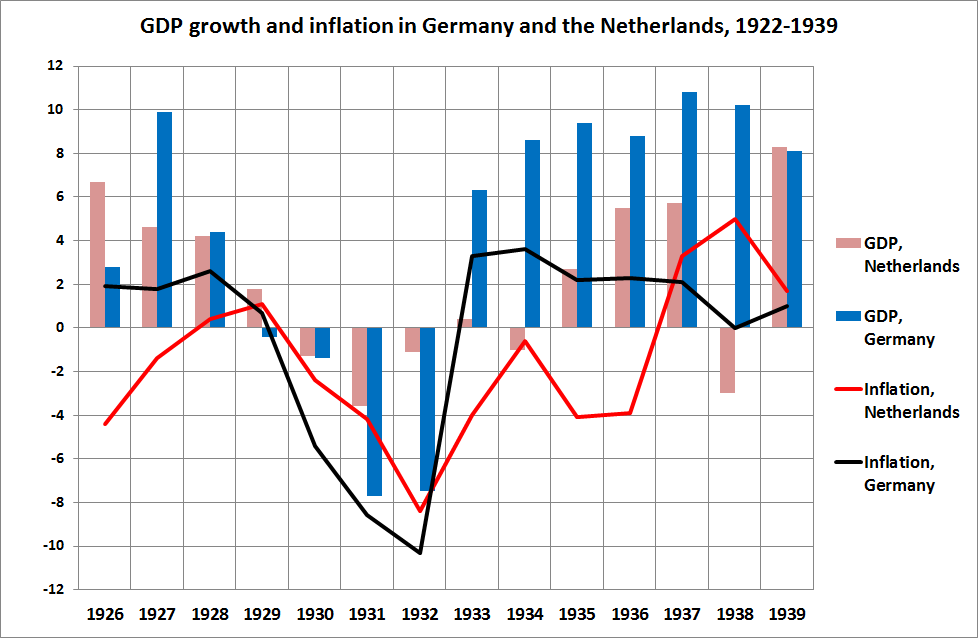

The Mefo system was abandoned when peak output was reached. Between 1933-1938, notes historian Niall Fergus on (2006), Germany’s gross domestic product grew, on average, by eleven percent a year, with no significant increase in inflation (see chart).

Source: Mahe (2012)

Tax Credit Certificates for Italy

As analyzed in detail by Cattaneo and Zibordi (2014), the Italian government could issue new bills called CCF (Certificati di Credito Fiscale = Tax Credit Certificates) by amounts necessary to gradually close the economy’s output gap, taking into consideration plausible values of the fiscal multiplier for an economy with large unutilized capacity where monetary policy operates under the zero lower bound.

CCF represent government bills of exchange: the government has no obligation to reimburse them in the future. Rather, two years after issuance, they are accepted to fulfill any financial obligation towards the Italian state (taxes, public pension contributions, national health system contributions, etc.). The deferral allows for output to start recovering and generate resources to offset the shortfall of the euro-denominated tax receipts that follows when CCF start being accepted by the State for payments of taxes and other obligations.

CCF are issued free of charge to private sector enterprises and employees. The State may assign an additional CCF allocation to itself, which it will use to implement further demand-support actions (e.g., supplementing income to financially distressed families, improving the national health system, speeding up payments of overdue bills to government suppliers, etc.).

Enterprises and employees receiving CCF allocations can immediately cash them into euros and use them for spending. The market will discount them like any zero-coupon two-year (default-free) government bonds. Those deciding to hold CCF will use them past the deferral date to pay taxes and obligations to the State.

Enterprises are allocated CCF based on their labor cost. CCF allocations primarily aim to reduce the fiscal wedge between gross salaries paid by the enterprises and the net salaries received by the employees. They cut enterprise tax bills and raise employees’ disposable incomes. Higher disposable incomes foster consumption, and labor cost reductions encourage employment and improve competitiveness. The trade balance reflects both the effect of lower labor costs on competitiveness and that of increased spending on imports. By partially offsetting tax-driven excess labor costs, CCF allocations help enterprises recover external competitiveness, thus balancing the effect that CCF allocations have on imports via higher demand.

(In light of this, and since CCF emissions (i) are not aimed to affect international trade balances, (ii) are open to all enterprises, and (iii) pursue an objective of common interest, they cannot be considered as “State aid” under EU law.)

Improving demand stimulates investment and revamps banking. As expectations reinvigorate, private consumption and investment bounce back, and the economy re-approaches full employment, the government reduces and finally terminates new CCF emissions while tax reductions become permanent.

Table I: Macroeconomic Simulation of the CCF Program

A preliminary simulation exercise suggests that the Italian government could issue CCF at a 200-billion annual rate for 2015-2018, and phase out the program during 2019-2023. Assuming a fiscal multiplier effect of 1.5 (Eichengreen and O’Rourke), conservatively spread across three years, and two alternative inflation scenarios, Italy would close the current output gap by 2017, never exceeding the Maastricht treaty 3% budget deficit limit, and steadily reducing its gross public debt/GDP ratio (see Table I). Note that, after CCF phase-out, the higher tax revenues due to GDP recovery allow for making permanent the demand support action (including the lower tax burden) initially financed with CCF.

Under the first scenario, inflation is assumed to remain unchanged in the “with CCF” scenario as compared to the “without CCF” one, since the current output slack is huge and sizable CCF allocations to enterprises reduce gross labor costs, which is in itself deflationary. However, should inflation somewhat rekindle, this would be consistent with what the ECB is currently trying to achieve. Under an alternative scenario where inflation hits 3.0 per cent inflation scenario during the 2015-2017 period when output growth accelerates, and the nominal average interest rate adjusts so as to keep the real interest rates is unchanged (a very conservative assumption since the higher nominal rates would actually be applicable to new debt issues only), the gross public debt/GDP profile would basically be unchanged. Regarding the actual volume of periodic CCF emissions, they could be scaled based on the residual output gaps, as the economy recovers, and the response of private sector spending.

Finally, the Italian state can also refinance, partially or totally, its public debt as it expires by issuing monetary instruments, i.e. liabilities not subject to default risk as they (similarly to the CCF) are accepted at maturity for tax payments. Tax-backed bonds are a possibility (Pilkington and Mosler 2012). This avoids future reoccurrence of 2011-style sovereign debt crises.

An unconventional measure for extraordinary times

The concept of CCF comes very close to that of “helicopter money”, which constitutes a joint act of monetary and fiscal policy (Grenville 2013) – as such the most powerful demand management tool in a liquidity trap (Bossone 2013b). By issuing CCF, the Italian state recovers (partial) monetary sovereignty and does not need to call the ECB into question: it deliberates the amount and timing of CCF issuance and, in its fiscal capacity, determines the criteria under which to allocate CCF through its budgetary process.

The use of CCF should be intended for very critical situations only, such as the economic depression that Eurozone crisis countries have faced for too long now, characterized by huge resource slack, deflationary tendencies, no autonomous monetary policy, and heavily constrained fiscal policy. Obviously, recourse to CCF issuance should not be abused. Issuance should take place under specific law provisions, strict and transparent parliamentary control, and a predetermined framework specifying the target to be achieved and the related timeframe.

Without reducing large debts by either fueling output growth or monetization, the Eurozone can only go one of two ways: a monetary union without sovereign defaults but at the cost of austerity and stagnation for many years ahead and effective policy dominance of surplus countries over deficit ones, or a monetary union without fiscal union but where sovereigns may default. In both cases, political and social costs are high. Of course, there is always the alternative of breaking up the euro, as increasingly evoked by discontented masses of euro citizens.

The CCF solution is a much better proposition. With it: the euro stays; austerity needs to be no more, growth resumes, and sovereign defaults are avoided; Germany and the other Eurozone surplus countries are not be forced into currency revaluations, and Italian and other euro citizens’ savings, salaries, pensions, etc. are not converted into new, lower-value and unstable domestic currencies.

Mr. Renzi, the CCF can be a way to revive Italy and save the euro.

References

Banca d’Italia (2014a) The Governor’s Concluding Remarks, Ordinary Meeting of Shareholders, 30 May, Rome.

Banca d’Italia (2014b), Financial Stability Report, May, N. 1, May, Rome.

Blanchard O and D Leigh (2013) “Growth forecast errors and fiscal multipliers”, IMF Working Paper WP/13/1, January.

Bossone B (2013a) “Unconventional monetary policies revisited (Part I)”, VoxEu, 4 October 2013.

http://www.voxeu.org/article/unconventional-monetary-policies-revisited-part-i

Bossone B (2013b) “Unconventional monetary policies revisited (Part II)”, VoxEu, 5 October.

http://www.voxeu.org/article/unconventional-monetary-policies-revisited-part-ii

Cattaneo M and G Zibordi (2014) La Soluzione per l’Euro, Hoepli, Milano. (English version forthcoming)

Coppola F (2014) “Why negative rates won’t work in the Eurozone”, Forbes, 6 April.

http://www.forbes.com/sites/francescoppola/2014/06/04/why-negative-rates-wont-work-in-the-eurozone/

Eichengreen B and K H O’Rourke (2012) “Gauging the multiplier: lessons from history”, VoxEu, 23 October http://www.voxeu.org/article/gauging-multiplier-lessons-history

Ferguson N (2006), The War of the World, Penguin, New York.

Grenville S (2013) “Helicopter money”, VoxEu, 24 February. http://www.voxeu.org/article/helicopter-money

Hatcher M and P Minford (2014) ‘Inflation targeting vs price-level targeting: a new survey of theory and empirics”, VoxEu, 11 May. http://www.voxeu.org/article/inflation-targeting-vs-price-level-targeting

Kimball M (2013) “How and why to eliminate the Zero Lower Bound: a reader’s guide”,

Supply-Side Liberal, September 30. http://blog.supplysideliberal.com/post/62693219358/how-and-why-to-eliminate-the-zero-lower-bound-a

Mahe E (2012) “Macro-economic policy and votes in the thirties: Germany (and The Netherlands) during the Great Depression”, Real-World Economics Review Blog, June 12

Odendahl C (2014) “Quantitative easing alone will not do the trick”, Centre for European Reform, 28 April http://www.cer.org.uk/insights/quantitative-easing-alone-will-not-do-trick

Pâris P and C Wyplosz (2014) “The PADRE plan: politically acceptable debt restructuring in the Eurozone”, VoxEu, 28 January

http://www.voxeu.org/article/padre-plan-politically-acceptable-debt-restructuring-eurozone

Pâris P and C Wyplosz (2013) “To end the Eurozone crisis, bury the debt forever”, VoxEu, 6 August http://www.voxeu.org/article/end-eurozone-crisis-bury-debt-forever

Pilkington P and W Mosler (2012), “Tax-backed bonds – A national solution to the European debt crisis”, Policy Note 2012/4, Levy Economics Institute of Bard College.

Schacht H H G (1967) The Magic of Money, Oldbourne, London.

Stella P (2014) “The negative rate chrono-synclastic infundibula” http://stellarconsultllc.com/blog/wp-content/uploads/2014/04/The-Negative-Rate-Chrono-Synclastic-Infundibula.pdf

Stucken R (1953) Deutsche Geld- und Kreditpolitik 1914 – 1953, Tübingen.

Turner A (2013) “Debt, Money and Mephistopheles”, speech at Cass Business School, 6 February.

Woodford M (2012) “Methods of Policy Accommodation at the Interest-Rate Lower Bound”, speech at Jackson Hole Symposium, 20 August.