It is generally agreed that public debt continues to pose a major problem for Greece. The IMF expects debt to decline to 124% of GDP by 2020, while annual rates of growth are projected at a little less than 3%. To achieve this target Greece has been forced to adopt highly restrictive fiscal policies, including the requirement of achieving a primary surplus of 4.5% by 2016. It is remarkable that policies of such severe austerity have been applied to a country that has suffered an economic depression since 2010. The resulting fall in GDP brought the ratio of debt to GDP to 174% in 2014, much higher than 130% in 2009, when the crisis started.

Nonetheless, the rescue packages implemented since 2010, and funded by the EU, the IMF and the ECB, have dramatically changed the characteristics of public debt in Greece. First, the composition of the debt has been altered dramatically since 2010, when debt comprised primarily bonds governed by Greek law. At the end of 2013 Greek public debt comprised mainly long-term loans provided by official lenders under the terms of the two bail-out programmes in 2010 and 2011, and governed by English law. Second, the weighted average annual cost of Greek debt fell precipitously from just over 4% in 2009 to just over 2% in 2012, though it seems to have crept up above 3% in 2013. And third, the weighted average maturity of Greek debt has been extended significantly, rising from a little under 8 years in 2009 to 16 years in 2013. [1]

In this context the fundamental problem posed by public debt in Greece is not merely the annual burden of servicing it but also the constraint that it imposes on economic policy. To service public debt the country is obliged to pursue a very restrictive fiscal policy, aiming for primary surpluses of 4.5% of GDP in 2016, based on high taxes and reductions in public expenditure, including public investment. Meanwhile, monetary policy is completely in the hands of the ECB and the parlous state of the private banking system means that credit is in short supply. The implication is that the country is unable to adopt policies that are urgently needed to boost demand, reduce unemployment and support growth.

Greece urgently needs debt relief to generate additional fiscal space for the government, allowing it to adopt fiscal policies that could quickly facilitate recovery and growth. This is imperative in a country with adult unemployment currently standing at the extraordinary level of 27%. The real question is not whether but how to effect debt relief. In this light, there are two fundamental options for Greece.

First, there is the ‘soft’ option of consensually extending the maturity of debt and lowering the average interest rate, thus reducing the annual interest outlay. This form of debt relief is preferred by the EU and the current Greek government because it would leave the nominal value of the debt intact, thus avoiding major conflict with the official lenders.

Second, there is the ‘hard’ option of writing off the nominal value of the debt (haircut) thus also reducing the annual interest outlay. This is advocated by several opposition parties in Greece and appears to have some support from the IMF, though there is no agreement regarding the extent of the write-off. It would face severe opposition from the official lenders and almost certainly necessitate some unilateral action by Greece, including default.

We consider the two options from the perspective of freeing up fiscal space to allow Greece to lift austerity and support its economy. Fiscal space is calculated as the savings from reducing the annual payment of interest, and thus relaxing the extremely restrictive targets for primary surpluses, while stabilizing the debt to GDP ratio. In effect, fiscal space measures the room that would be opened to a government to follow more expansionary fiscal policies without running increased deficits, provided that debt relief was available. It indicates the margin for alternative policies that would place growth and employment at the forefront, which is what Greece requires, rather than servicing the debt, which is what current policies do.

The main conclusions from the study are as follows:

i) The ‘soft’ option would have a negligible impact on the ratio of debt to GDP, improving it by barely 5% by 2019 versus the baseline scenario. The reason is that Greek debt was significantly restructured in 2012 and the average interest rate has already been lowered to around 3%.

ii) The fiscal space gained through the ‘soft’ option of reducing the interest rate by 0.5% would amount to just 0.8% of GDP per year from 2014 to 2019; if the reduction was 1% the fiscal space would average 1.6% of GDP per year. These are insignificant gains particularly in view of the current state of the economy (Figure 2).

iii) The ‘hard’ option would have a decisive impact on the ratio of debt to GDP since it would directly reduce the nominal value of the debt.

iv) The ‘hard’ option would generate substantial fiscal space averaging 4.8% of GDP for the period between 2015-19. This corresponds to nearly 10bn EUR a year that would become available for public investment and welfare expenditures. The gain would be between six and three and a half times greater than that from the ‘soft’ option, depending on the interest rate reduction in the latter. Over 2015-9 the sum would become enormous for the depressed Greek economy (Figure 2).

v) The ‘hard’ option would make fiscal stability easier to achieve than the ‘soft’ option, even though there would be much more space for fiscal expansion. Under the ‘hard’ option government deficits could be reasonably maintained at low levels (say, under 3% of GDP) while also stabilising the ratio of debt to GDP.

2.Methodology and data

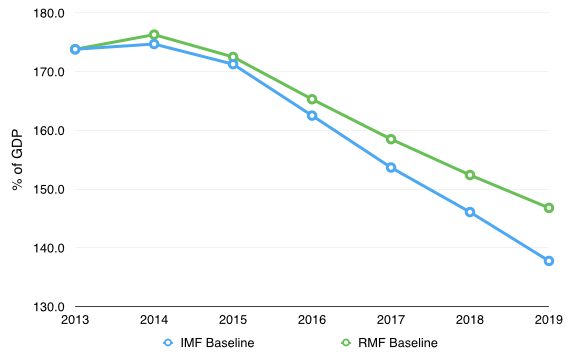

This analysis uses a model of debt sustainability under fairly standard assumptions. [2] It compares a ‘soft’ option of reducing the interest rate by either 0.5% or 1% with a ‘hard’ option of a deep write-off lowering the ratio of debt to GDP to the Maastricht-imposed condition of 60%. The period of comparison is 2014-19. The macroeconomic data used in the model were taken from the latest edition of the World Economic Outlook (WEO) of the IMF. [3] The RMF baseline scenario used to test the impact of the different options closely resembles the official projections of the IMF for Greece (Figure 1):

Figure 1 – Gross Debt as % of GDP; General Government; Greece

Source: IMF (2014) World Economic Outlook; projections made by the authors.

3.The ‘soft’ option

The ‘soft’ option of extending the maturity of loans and reducing in the average interest rate would have a marginal effect on the evolution of public debt. Figur 2 shows that a reduction of 50 basis points in the interest rates would only improve the debt to GDP ratio by 5 percentage points in 2019 relative to the RMF baseline scenario.

Figure 2 – Gross Debt as % of GDP; General Government; Greece

Source: IMF (2014) World Economic Outlook; projections of the authors.

Furthermore, the ‘soft’ approach would not allow for a meaningful relaxation of austerity policies. If the savings generated were to be used to lower the primary balance targets, without a change in the overall strategy of debt reduction, they would create a fiscal space averaging merely 0.8% of GDP per year. If the reduction on the interest rate were to be 100 basis points, the fiscal space would rise to 1.6% per year, which is more significant but barely what the country needs after a recession of such depth (Figure 3).

Figure 3 – Additional fiscal space associated with the “soft” option – General Government Non-Interest Expenditure as a % of GDP[4]

Source: Projections by the authors.

4.The ‘hard’ option

The ‘hard’ option is assumed to include a write off (haircut) of a large part of the debt (possibly with a formal default). For the purposes of this analysis it is assumed that the target would be a debt to GDP ratio of 60% in line with the Maastricht criteria. This would be a very deep reduction, of the order of 200bn EUR, and it would undoubtedly have serious political and other implications, which cannot be analysed here. What matters for the present analysis is to measure the implications for the additional fiscal space available to the country.

To assess the ‘hard’ option it is further assumed that, following the write-off, fiscal policy continues to conform to the Maastricht criteria: government deficit would remain under 3% of GDP and debt would be stabilised at a ratio of 60% of GDP. It also assumes that the government would be able to finance a primary balance deficit of 0.7% per year for 2015-2019;[5] finally, it is assumed that interest rates would remain stable. [6]

Figure 4 – Additional fiscal space associated with a “hard” option – General Government Non-Interest Expenditure as % of GDP [7]

Source: Projections by the authors.

Figure 4 shows that the ‘hard’ option would create a unique opportunity for a dramatic change in the fiscal framework of Greece. Compared to the RMF baseline, the ‘hard’ option would allow the government of Greece to increase non-interest expenditures by an average of 4.8% for the period between 2015 and 2019. This would be equal to an average of 9.9bn EUR per year, which would roughly six times the magnitude of fiscal space achieved through a 50 basis points reduction on the average interest rate.

A deep debt write-off is the best option available to Greece, if it wishes to gain room to implement fiscal policies supporting growth as well as ensuring debt sustainability. It might be observed that, given the political and economic implications associated with such a major sovereign default, the ’hard’ option would be unlikely to materialize. There is no denying the difficulties of such path and the least that would be required would be a determined government and solid popular support. Achieving a debt default of more than 200bn EUR, in part through unilateral action, is certainly a hard task. However, the undoubted difficulties pale into insignificance when compared to the implications of the current policy framework in Greece. The RMF baseline scenario indicates that, under current policies, Greece would reach the threshold of 60% of debt to GDP in 26 years! Effectively, the country would have to have austerity measures of one type or another throughout this period. The issue is obviously political and Greece will soon have to choose between the disastrous current policies and the tough but promising alternative.

[1] See Greek Public Debt Management Agency, http://www.pdma.gr/index.php/en/public-debt-strategy/public-debt/historical-characteristics/weighted-average-maturity

[2] The basic equation that underpins the model can be written as follows:

¶ t+1 – ¶ t = (i t+1 – p t+1 – g t+1) ¶t – r t+1 – tb t+1

Where: ¶ is the debt stock; i is the nominal interest rate; p is the GDP deflator; g is the real GDP growth rate; r is the primary fiscal balance; tb represents other non-debt creating inflows (grants, privatisations, etc.). Thus, if tb t+1 = 0 and (i t+1 – p t+1 – g t+1) @ 0, debt would increase (decrease) if there was a primary fiscal deficit (surplus). See, Escolano, J. (2010) “A Practical Guide to Public Debt Dynamics, Fiscal Sustainability, and Cyclical Adjustment of Budgetary Aggregates,” IMF Technical Note and Manual No. 2010/02 (Washington: International Monetary Fund).

[3] The variables used in the model were GDP growth, GDP deflator, Core Price Index (CPI), general government revenues, general government expenditures, general government primary balance and general government gross debt for the period 2014–19. An implicit interest rate was calculated as the difference between the projected general government fiscal balance and the general government primary fiscal balance, divided by the debt stock.

[4] Note that in the case of the “soft” option, fiscal space is defined as the additional non-interest expenditure – compared to the baseline scenario – that would return the debt to GDP ratio to its trend according to the RMF baseline following a reduction in the interest rate.

[5] The primary balance refers to difference between revenues and expenditures, excluding interest payments. A primary deficit, therefore, implies the need for additional resources, either through grants or borrowing, to finance the current level of expenditures. Given that in the initial stages of a sovereign default a country might find it difficult to obtain such additional financing, the primary balance becomes an additional constraint on fiscal policy. For methodological purposes, this OPP only uses the Maastricht criteria as the overriding constraint on fiscal policy. If the further constraint were to be included the fiscal space associated to the hard option would decrease by 0.7% of GDP per year.

[6] In the short term a sovereign default implies a temporarily exclusion from market funding. Nonetheless there is little empirical evidence which shows that such exclusion would last for an extended period of time. Furthermore as the fiscal position of a country would improve after the default, creditors would be more, not less, inclined to lend. This would also result in the stabilization or reduction in the interest rates. See, Stiglitz, J. (2010) “Sovereign Debt: Notes on Theoretical Frameworks and Policy Analyses” in Overcoming Developing Country Debt Crises, B. Herman, J.A. Ocampo, and S. Spiegel, eds., Oxford, Oxford University Press.

[7] Note that in the case of the “hard” option, fiscal space is defined as the additional non-interest expenditure – compared to the baseline scenario – that would stabilize the debt to GDP ratio at 60% following default.