The purpose of this short article is to review the progress of external account adjustment and internal devaluation in Eurozone countries

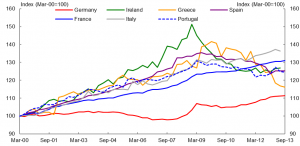

Unit Labour Cost Comparison

Unit labour cost-based measures of competitiveness are common-place in the literature. Those estimates show that German unit labour costs remained broadly unchanged between 2000 and 2009, while they rose by about one third in the rest of the Eurozone[2].

Since 2008, Ireland, Greece, Portugal and Spain have made some progress in reducing their unit labour cost gaps with Germany (see Chart 1), with the decline in unit labour costs in those countries often being larger in the tradable sector than in the non-tradable sector[3]. Greece and Ireland have recorded the largest improvements in relative unit labour costs since end-2008 (a fall of around 19 and 17 per cent in their relative unit labour costs vis-a-vis Germany, respectively). In the case of Ireland this substantial adjustment partly reflects the relatively high degree of labour-employer cooperation in that country[4].

It seems clear that reducing unit labour costs in uncompetitive countries is a sine qua non for internal devaluation to be successful. Unit labour costs can be reduced either by reducing wage and/or non-wage labour costs, or by increasing labour productivity.

However, there are at least six analytical qualifications attaching to the use of unit labour cost-based measures as the sole basis for competitiveness comparisons:

a) First, if there are different evolutions of labour costs and productivity in the traded and non-traded goods sectors, it is possible that an overall increase in relative unit labour costs could be due to relatively high unit labour cost growth in the non-traded goods sector, with little direct impact on competitiveness. The IMF[5] concludes that this was the case between 2000 and 2007 in Greece and Ireland, and to a much lesser extent in Portugal and Spain.

b) Second, if production structures and the degree of mechanisation and technological development are broadly the same as between two countries then unit labour costs may be meaningfully compared. But if the production, specialisation, product quality and technology structures, and export compositions are radically different, say as between Germany and Greece, or change through time, then one would need to be cautious when using unit labour cost index changes alone to draw strong inferences about changing competitiveness differences between Germany and Greece. Spain has been relatively successful in restructuring toward export activities, for example, whereas this may not have been the case for Greece.

c) Third, another reason why prices may not always move in-tandem with unit labour costs (across Eurozone countries in the short to medium terms) is because internal price competition policies may differ: the intensity of price competition may vary across countries, and through time.

d) Fourth, profit margins can be subject to substantial volatility, particularly in the traded-goods sector of the economy. Changing profit margins could cause competitiveness to vary from that suggested by relative movements in unit labour costs.

e) Fifth, unit labour costs relate to ‘labour’ costs alone. Capital, land, energy and finance combine with labour to create exports or domestic production to replace imports. A country could rate poorly on unit labour costs, but more than make-up for that through relatively low unit capital costs, energy, land and borrowing costs.

f) Finally, when countries experience recessions and depressions there is a natural weeding-out of relatively high cost business operations. It would be expected, therefore, that firms paying relatively high wages or experiencing relatively low productivity growth — that is, relatively high unit labour cost firms — would close. The closure of such firms would work to lower measured unit labour costs. However, the observed recorded reduction in unit labour costs does not, in this case, imply improved competitiveness.

Importantly, the unit labour cost chart is, of course, not a measure of the ‘price competitiveness’ of traded goods and services. Even so, the unit labour cost chart is used almost universally as an indicator of intra-Eurozone competitiveness. This partly reflects the fact that the President of the European Council (Hermann Van Rompuy) uses it repeatedly for that purpose. The unit labour cost chart is also a key indicator in the European Union’s Macroeconomic Imbalances Procedure. Almost all economists, particularly those in Europe, are addicted to it (possibly because it appears to suggest a much needed ‘good news’ story).

The unit labour cost (ULC) chart is, however, without very heavily qualified interpretation, grossly misleading when used in the Intra-Eurozone trade competitiveness context. Apart from the disparate trade imbalances existing at the base year, one of the main problems with it (alluded to earlier) is that it measures ULC for the whole economy, and not just for the traded goods sector. The traded goods sector is usually the most competitive sector in any economy, and this is particularly the case for competing contiguous periphery countries in Europe.

To illustrate just how misleading ULC comparisons can be, the unit labour cost comparison (Chart 1) suggests that Ireland experienced the worst competitiveness conditions of all periphery countries up until 2009. This view is totally mistaken. The mistake can be easily confirmed by observing the export price trade competitiveness comparison (Chart 2)[6]. That comparison shows that Ireland never had a significant price competitiveness imbalance vis-à-vis Germany. That view is confirmed in studies which suggest that Ireland was unsustainably super-competitive in 1999 (at the formation of the Eurozone) when its trade surplus stood at a massive 25 per cent of GDP, rising to 30 per cent a few years later.

Furthermore, between 2000 and 2007, whereas NULC measured for the whole Irish economy rose by around 30 per cent or so relative to NULC measured for the whole Germany economy, relative NULCs measured for the manufacturing sectors for both Ireland and Germany were relatively stable (that is to say, there was no loss of trend competitiveness in the sector of the Irish economy most linked to intra-Eurozone trade — the manufacturing sector)[7]. This observation supports, and is consistent with, the message in the export price indicator (see Chart 2, later), and the fact that Ireland’s trade surplus remained relatively very high, standing at around 20 per cent of GDP in 2009.

The unit labour cost comparison (Chart 1) suggests that Portugal, Spain, Ireland and Greece have all improved their relative trade competitiveness since 2009/10. But the export price competitiveness comparison (Chart 2) shows that this has not been the case at all, and, indeed, that there has been no convergence of price competitiveness in the Eurozone.

We can conclude, therefore, that the impression of substantial progress in the realignment of intra-Eurozone trade competitiveness, given by the unit labour cost chart, is false[8], and that, thus far, the policy of internal devaluation in the Eurozone has very largely failed.

Chart 1: Nominal Unit Labour Cost-Based Competitiveness Comparison

Export Price-Based Comparisons

A more relevant parameter to rely on for drawing judgments about movements in relative competitiveness within the Eurozone would arguably be the traded goods price-based competitiveness indicators, based on export prices, import prices or a combination of both.

- For example, changes through time in a comparison of export price indexes for both deficit and surplus countries would illustrate changes in the relative competitiveness of exports.

– All other things equal, a rise in the price of exports of country A relative to country B would mean a rise in export competitiveness of country B which could lead to increased exports from country B to country A.

Chart 2: Export Price-Based Competitiveness Indicator

The export price-based competitiveness comparison (Chart 2) suggests that the positions of Greece, Italy, Portugal and Spain are showing little improvement relative to Germany, but that, at least in respect of export prices, France and Ireland are broadly competitive with Germany, and have generally been so since the introduction of the Euro. However, there has been no significant improvement in relative export price competitiveness in Ireland and Spain (and possibly Greece) since 2008, despite the substantial improvements recorded in their relative unit labour costs (see Chart 1).

Relevance

The issued raised above — simple as it may appear at first blush — cannot be overestimated (see further below). It bears on, and supports, the US Treasury’s analysis in its Report to the Congress on International Economic and Exchange Rate Policies (October 2013)[9].

In that report, the US Treasury is highly critical of the lack of adjustment in the Eurozone, Germany’s constrained demand and Germany’s large current account surplus; developments that the US Treasury rightly claims are creating a deflationary bias in the Eurozone area.

The US Treasury Report states as follow:

‘To ease the adjustment process within the euro area, countries with large and persistent surpluses need to take action to boost domestic demand growth and shrink their surpluses. Germany has maintained a large current account surplus throughout the euro area financial crisis, and in 2012, Germany’s nominal current account surplus was larger than that of China. Germany’s anaemic pace of domestic demand growth and dependence on exports have hampered rebalancing at a time when many other euro area countries have been under severe pressure to curb demand and compress imports in order to promote adjustment. The net result has been a deflationary bias for the euro area, as well as for the world economy. Stronger domestic demand growth in surplus European economies, particularly in Germany, would help to facilitate a durable rebalancing of imbalances in the euro area’.

This article provides support for the assertions made by the US Treasury.

[1] The Global Competitiveness Report 2013/14 (World Economic Forum, 2013) takes into account 12 different parameters to develop its overall measure of international competitiveness, including institutions, infrastructure, technology, labour market efficiency and product market efficiency, etc.

[2] See Martin Lueck, ‘European Economic Focus: Germany’s current account surplus and Europe’s rebalancing’, UBS, November 2013.

[3] See Euro Area Policies, 2013 Article IV Consultation Report, IMF, July 2013.

[4] According to the World Economic Forum’s Global Competitiveness Report, 2013-14, Ireland is highly ranked in ‘cooperation in labour-employee relations’ at rank 13, and above Germany (with the rank of 18). Dickens et al. found that in his sample of 16 countries Ireland had the highest degree of nominal wage flexibility and was among those countries with the lowest incidence of employment protection legislation and the highest degree of coordination in bargaining at a high level. See ‘How Wages Change: Micro Evidence from the International Wage Flexibility Project’, William T. Dickens et al., Journal of Economic Perspectives, Vol 21, Number 2, Spring, 2007.

[5] See International Monetary Fund, World Economic Outlook, April 2013.

[6] The export price competitiveness indicator does not suffer the many problems of the economy-wide unit labour cost indicator, and represents competitiveness based on the price of traded goods and estimated prices of services at the border.

[7] An analysis of Irish competitiveness conducted by the Irish Central Bank finds that ‘the deterioration in manufacturing price competitiveness was due almost entirely to [Euro] exchange rate movements’, not to unit labour cost movements. It also states that ‘In 2008 in the internationally traded goods industrial sector wage compensation per hour was lower in Ireland than the Eurozone average’. See ‘Measuring Price and Labour Cost Competitiveness’, Central Bank of Ireland, Quarterly Bulletin, January 2010.

[8] This observation, in and of itself, does not deny the proposition that, with fixed exchange rates within the Eurozone, the uncompetitive periphery countries do need to reduce unit labour costs and prices in the traded goods sector relative to those of Germany.

[9] See Report to Congress on International Economic and Exchange Rate Policies, US Department of the Treasury, Office of International Affairs, 30 October 2013.