Ideally, competition and concerns over reputation should incentivize agencies to publish accurate and unbiased ratings. However, as Bernhard Bartels and Beatrice Weder di Mauro have argued in a recent Voxeu column (http://www.voxeu.org/article/rating-agency-europe-good-idea), flawed models, bad incentives, and the concentrated market structure distort competition in the rating business and can lead to biased rating decisions. Many of the concerns about biased sovereign ratings revolve around the role of the credit rating agency’s “home country” – a factor largely disregarded in previous research. We define a “home bias in sovereign ratings” as a deviation of the rating level in favor of the home country (or countries aligned with it) from what would be justified by the sovereign’s economic and political fundamentals. By analyzing a broad set of rating agencies, our recent paper (Fuchs and Gehring 2013) investigates whether there is systematic evidence for such a bias and analyzes the factors that might be driving it. While most of the variation in sovereign ratings is explained by the fundamentals of rated countries, our results provide empirical support for the existence of such a home bias, which is driven by the home country’s economic interests as well as cultural ties between home and sovereign.

The credit rating agencies

Of the current 150 credit rating agencies, most agencies are only active in narrow national or regional markets and focus solely on corporate ratings (White 2010; De Haan and Amtenbrink 2011). In addition to the three big U.S.-based agencies, Fitch, Moody’s and S&P, there are six other agencies, based in five different countries, that provide sovereign ratings for at least 25 sovereigns: Capital Intelligence (Cyprus), Dagong (China), DBRS (Canada), Feri (Germany), Japan Credit Rating Agency, and Rating and Investment Information (Japan). While the U.S.-based agencies dominate the market, the interest in these smaller agencies is increasing – not only in the financial sector. Downgrades by Dagong in particular receive a lot of media attention.[ii]

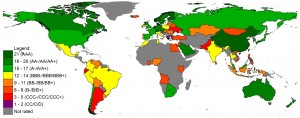

A simple comparison of the sovereign ratings issued by China-based Dagong and U.S.-based Moody’s illustrates why ratings might be perceived as influenced by the agency’s home country (see Figures 1 and 2). Compared to Moody’s, Dagong assigns higher ratings to the Chinese territories Hong Kong and Macao as well as to the group of BRICS countries, including China itself. At the same time, Dagong assigns lower ratings to many Western economies than Moody’s does.

Figure 1: Sovereign ratings assigned by Dagong (China, as of June 2013)

Source: Fuchs and Gehring (2013)

Figure 2: Sovereign ratings assigned by Moody’s (USA, as of June 2013)

Source: Fuchs and Gehring (2013)

Theories why the home country matters

As we argue in Fuchs and Gehring (2013), a home bias in sovereign ratings can be the result of both political economy influences and culture. With respect to political economy influences, governments have strong reasons to sway rating outcomes: Ratings determine a sovereign’s access to international capital markets and its borrowing costs. Moreover, there could be vested interests to prevent downgrades of countries in which the home country has strong geopolitical or economic interests (e.g., important export markets and countries to which home-country banks are particularly exposed). Home-country governments possess substantial leverage over agencies as they control the respective regulatory body whose official recognition agencies need to operate (White 2010; De Haan and Amtenbrink 2011). Since ratings provided to home-country firms are a major source of income, the prospect of losing that recognition is an imminent threat to agencies. Anecdotal evidence points at alleged attempts of intimidation against US agencies by the US government and at strong relations of China-based Dagong with the Chinese government (see Fuchs and Gehring 2013 for details).

The second mechanism could be culture: Various studies show that cultural distance affects financial decision-making of both households and firms (e.g., Grinblatt and Keloharju 2001). Giannetti and Yafeh (2012), for example, show that bank professionals grant smaller loans and charge higher interest rates to banks that are culturally more distant. Given this evidence, it would not be surprising if cultural distance also affects decision-making at rating agencies.

Empirical results

The empirical results in Fuchs and Gehring (2013) show that, for the nine agencies studied, 86% of the variation in sovereign ratings can be explained by “objective” sovereign-specific economic and political fundamentals. Nevertheless, we find evidence of a home bias in sovereign ratings. With respect to a “same-country effect,” the results show that the average agency assigns a rating to its home country that is almost one point higher than justified by how they assess other sovereigns. Analyzing each agency separately, Figure 3 shows that many agencies overrate their home country. The actual rating levels as assigned to the home country (black solid line) are in many cases above the rating levels that the home agency would assign if it were to treat the home country as all other sovereigns (blue-dotted line).

Figure 3. Same-country bias: Actual vs. predicted rating levels of all home countries

Notes: This figure contrasts the actual rating and the predicted rating based on how each agency weighs the economic and political fundamentals of sovereigns. The solid line depicts the actual rating, the dotted line the rating that should be assigned to the home country based only on the economic and political fundamentals. Source: Fuchs and Gehring (2013)

Furthermore, there is robust evidence that countries in which home-country banks possess more foreign claims obtain significantly better ratings. With regard to the role of culture, we find no evidence that racial or ethnic differences affect ratings. However, we find that countries with a higher level of cultural proximity, as operationalized by measures of linguistic distance, receive better treatment. This effect is both statistically and economically significant. Still, this does not necessarily reflect “irrational behavior” or bad intentions on behalf of the agencies. They have to base their decisions on limited and incomplete information that is acquired either from publicly available sources or from the rated country. Linguistic distance increases agencies’ costs of information gathering and can consequently lead to a lower amount of information being collected about culturally more distant countries. Predictions based on less information are less precise and thus yield a higher predicted default probability.

However, if the cultural bias was solely due to a lack of information, the existence of an office in a rated country should alleviate the bias. When we interact the existence of an office with cultural distance, however, the bias is not mitigated. Thus, the most plausible explanation is that cultural distance relates to more pessimistic risk perceptions. Previous studies have shown that predictions about future developments are more optimistic when they refer to the home country (e.g., Kilka and Weber 2000) and that cultural distance is negatively related to bilateral trust (Guiso et al. 2009). Bilateral trust not only affects how the available information is perceived, but also affects beliefs about a sovereign’s willingness to repay its debt. History has shown that countries commonly default on their debt for reasons that are opportunistic and relate to domestic political considerations rather than to insufficient liquidity.

Reflections on an appropriate regulatory framework

There are several important policy conclusions from these results. First, the robust relationship between bank exposure and ratings is critical. The new limits on ownership and additional transparency requirements outlined in the EU Regulation on Credit Rating Agencies (12/2010, amended 5/2011) are a step in the right direction, but it must be followed up. New regulation should do more to stimulate competition between agencies in order to reduce the reliance on the “Big Three.” In this regard, further propositions by the EU Commission (EC MEMO/13/13) seem to reflect political activism rather than economic arguments. For example, restricting the update frequency of unsolicited ratings to three times per year would lower the economic benefits that ratings can provide. Such a regulation would particularly affect smaller agencies which rely more on unsolicited ratings and could thus stifle competition. A more promising approach would be to explicitly embrace the plurality of methods and opinions in cases where economic arguments suggest the use of external ratings. Since our results (in line with previous research) suggest that culture affects economic assessments and predictions, regulation could require ratings by two or more agencies, ideally with different cultural backgrounds. This would help to obtain more comprehensive risk assessments and automatically lead to a more diverse and competitive rating agency landscape.

References

Afonso, António, Davide Furceri and Pedro Gomes (2012). Sovereign Credit Ratings and Financial Markets Linkages: Application to European Data. Journal of International Money and Finance 31(3): 606-638.

Bartels, Bernhard and Beatrice Weder di Mauro (2013). A rating agency for Europe – A good idea? http://www.voxeu.org/article/rating-agency-europe-good-idea

Borensztein, Eduardo, Kevin Cowan, and Patricio Valenzuela (2013). Sovereign Ceilings “Lite”? The Impact of Sovereign Ratings on Corporate Ratings. Journal of Banking & Finance 37(11): 4014-4024.

De Haan, Jakob and Fabian Amtenbrink (2011). Credit Rating Agencies. DNB Working Paper No. 278. Amsterdam, Netherlands: De Nederlandsche Bank

Fuchs, Andreas and Kai Gehring (2013). The Home Bias in Sovereign Ratings? University of Heidelberg Department of Economics Discussion Paper Series No. 550. Available at http://papers.ssrn.com/sol3/papers.cfm?abstract_id=2370374.

Giannetti, Mariassunta and Yishay Yafeh (2012). Do Cultural Differences Between Contracting Parties Matter? Evidence from Syndicated Bank Loans. Management Science 58(2): 365-383.

Grinblatt, Mark and Matti Keloharju (2001). How Distance, Language, and Culture Influence Stockholdings and Trades. Journal of Finance 56(3): 1053-1073.

Guiso, Luigi, Paola Sapienza and Luigi Zingales (2009). Cultural Biases in Economic Exchange? Quarterly Journal of Economics 124(3): 1095-1131.

Kilka, Michael and Martin Weber (2000). Home Bias in International Stock Return Expectations. Journal of Psychology and Financial Markets 1(3-4): 176-192.

White, Lawrence J. (2010). Markets: The Credit Rating Agencies. Journal of Economic Perspectives 24(2): 211-226.

[i] See media reports by AFP (http://www.google.com/hostednews/afp/article/ALeqM5jj73UJWw-IDUL1HU5WqDhvPBfqcA?hl=en; accessed 12 September 2013), The Express Tribune (http://tribune.com.pk/story/211912/breaking-the-oligopoly-ratings-agencies-under-attack-amid-debt-crisis/; accessed 13 June 2013), Today’s Zaman (http://www.todayszaman.com/news-280044-.html; accessed 13 June 2013), and BBC News (http://www.bbc.co.uk/news/business-14043293; accessed 12 September 2013).

[ii] See, for example, articles on the websites of The Economist (http://www.economist.com/blogs/buttonwood/2011/08/debt-ceiling-crisis-1; accessed 13 November 2013), the Wall Street Journal (http://blogs.wsj.com/moneybeat/2013/10/17/chinas-dagong-takes-aim-at-u-s/?KEYWORDS=dagong; accessed 13 November 2013) and CNN (http://edition.cnn.com/2011/BUSINESS/08/02/china.us.rating/; accessed 13 November 2013)