For some time, and primarily on the basis of Reinhart and Rogoff (2010), most of the debate focused on the existence of a certain debt-to-GDP ratio beyond which a country would likely experience a severe economic downturn. However, it is nowadays widely acknowledged that Reinhart and Rogoff (2010) hypothesis is not strongly supported by empirical data, see e.g. Herndorn et al. (2013). In contrast, the most recent strand of the literature has focused on the financial-market stress as an alternative threshold variable affecting the link between a country’s fiscal stance, and its macroeconomic performance (cf. Afonso et al. (2011) and Mittnik and Semmler 2012). Afonso et al. (2011) and Mittnik and Semmler (2013), for instance, argue that the main factor determining the effectiveness of fiscal policy as well as the sustainability of fiscal debt is the state of the financial markets and not the extent of public indebtedness itself, as postulated by Reinhart and Rogoff (2010).

Given the crucial role of sovereign bond spreads – and their spillover to the private sector credit costs –in the effect of sovereign debt on economic growth, an additional aspect of the non-linear nexus between these two variables is the question whether a country is in a monetary union or not. As argued by De Grauwe and Ji (2013), this point is of particular relevance for the EMU, since bond spreads may be more prone to investors’ sentiments in countries of a monetary union than in stand-alone countries. According to these authors’ findings, while the explanatory power of the debt-to-GDP ratio for bond spreads in EMU countries is significantly higher during times of economic distress than during times of economic stability, for non-EMU countries, however, this empirical regularity cannot be corroborated by statistical tests. A similar result is obtained by Schoder (2013), who also argues that investors’ sentiments are even more volatile in the EMU countries of the periphery than in the core EMU countries. According to these findings, the non-linearity in the sovereign debt-economic growth relation should be expected to be more pronounced in EMU countries, especially in the peripheral countries, than in stand-alone countries.

In a recent paper (Proaño et al. 2013), we estimate the effects of sovereign debt and financial stress on economic growth through an econometric, regime-dependent framework where the regimes depend on the debt to-GDP ratio and the level of financial stress. We investigate this relationship empirically for thirteen OECD countries from 1980 to 2010, employing quarterly data and using dynamic country-specific and dynamic panel threshold regression analysis. We pay special attention to the differences between EMU and stand-alone countries as well as between northern EMU and southern EMU countries. Our sample includes Australia, Austria, Belgium, Canada, Denmark, Germany, Spain, France, the United Kingdom, Italy, Japan, the Netherlands, and the United States.

After controlling for other macroeconomic variables which may affect the growth rate of real GDP such as the long-term real interest rate, the economy’s relative competitiveness and the growth rate of the population, we find empirical evidence supporting the following hypotheses through our dynamic panel threshold regressions: On the one hand, there is no evidence for a universally valid negative impact of government debt on economic growth in the countries considered in our econometric analysis, independently of whether we use country-specific or panel estimation methods, and independently of the different country-grouping schemes we may use (all countries, EMU and non-EMU countries and north-EMU and south-EMU countries). The notion that larger government indebtedness by itself may reduce economic growth, put forward by proponents of the expansionary austerity hypothesis, is simply not supported by macroeconomic data of industrialized countries over the last thirty years. In contrast, we identify the IMF financial stress index (unfortunately a rough and imperfect measurement for the uncertainty and volatility in the financial markets) as a crucial source of the nonlinearity between sovereign debt and economic activity. Only at high levels of financial stress does it appear possible for the debt-GDP ratio to negatively affect growth. However, our fourth finding makes this unlikely; we find evidence that debt reduces growth during high financial stress only for countries within a monetary union, i.e. the European Monetary Union.

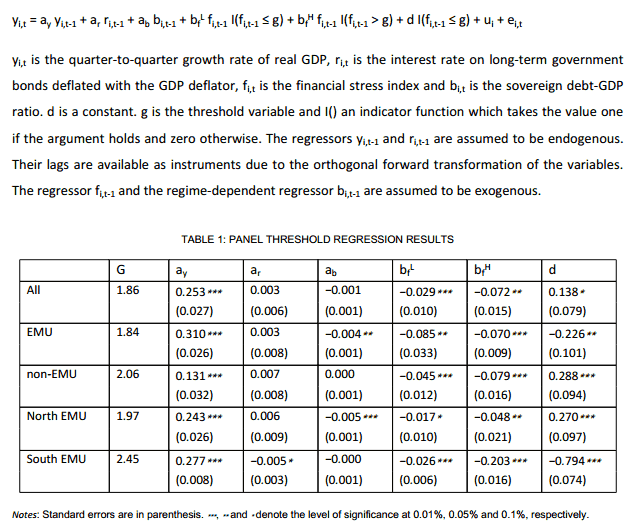

Further, we find that the direct influence of higher financial stress on economic growth is also nonlinear and depends itself on the level of the financial stress. Table 1 lays out our estimation results for the following regression:

As the results summarized in Table 1 clearly show, the effect of financial stress on economic growth is not only negative and statistically significant in both regimes (high and low financial stress) in all panel regressions considered even after controlling for other indirect effects. In all specifications, the direct negative effect of greater financial stress on economic activity is significantly larger in absolute values when financial stress is high.

In the context of the current debate on the U.S. debt ceiling, these findings not only provide further evidence against the suggested arguments for expansionary fiscal consolidations, but also stress the importance of avoiding financial havoc resulting from a still possible U.S. default. Indeed, as we outline in a theoretical model in our paper, financial stress depresses macroeconomic activity not only through its effects on the risk premium on government and private bond yields, but also through the direct effect that a greater degree of uncertainty and nervousness may have on consumption and investment decisions.

The world economy continues to struggle with the economic and social consequences of the recent 2007-08 worldwide recession. As the fiscal stance in the majority of industrialized countries remains also fragile, chances are low that fiscal programs could be implemented to the same extent as in the recent economic crisis if a new global crisis occurred. And chances are high that the ongoing ideological political struggle in the U.S. about the debt ceiling may indeed lead the world economy to a new recession due to the great uncertainty which has created in the financial markets – and too much is at stake to take chances now.

REFERENCES

Afonso, A., Baxa, J. and Slavik, M. (2011), ‘Fiscal developments and financial stress. A threshold VAR

Analysis’, Working Paper 1391, European Central Bank.

Blanchard, O. and Perotti, R. (2002), ‘An empirical characterization of the dynamic effects of changes

in government spending and taxes on output’, The Quarterly Journal of Economics 117(4), 1329–1368.

De Grauwe, P. and Ji, J. (2013), ‘Self-fulfilling crises in the eurozone: An empirical test’, Journal of

International Money and Finance 34, 15–36.

Herndon, T., Ash, M. and Pollin, R. (2013), Does high public debt consistently stifle economic growth?

A critique of Reinhart and Rogoff, Working Paper 4/15/2013, PERI.

Mittnik, S. and Semmler, W. (2012), Estimating a banking-macro model for Europe using a multiregime

VAR. SSRN http://ssrn.com/abstract=2012106.

Mittnik, S. and Semmler, W. (2013), ‘The real consequences of financial stress’, Journal of Economic

Dynamics and Control 37(8).

Proaño, C. R., Schoder, C. and Semmler, W. (2013), Financial Stress, Sovereign Debt and Economic Activity in Industrialized Countries: Evidence from Nonlinear Dynamic Panels. NSSR Department of Economics Working Paper 04/2013, New York.

Reinhart, C. M. and Rogoff, K. S. (2010), ‘Growth in a time of debt’, American Economic Review:

Papers & Proceedings May, 573–578.

Schoder, C. (2013), ‘The fundamentals of sovereign debt sustainability: Evidence from 15 OECD

countries’, Empirica. Journal of European Economics, forthcoming.