[T]he Bank of Japan’s argument is, “Oh well, we’ve got the interest rate down to zero; what more can we do?” It’s very simple. They can buy long-term government securities, and they can keep buying them and providing high-powered money until the high powered money starts getting the economy in an expansion. What Japan needs is a more expansive domestic monetary policy.

In other words, Friedman was calling for large scale asset purchases (LSAPs) long before it was vogue and understood that for the purchases to help the economy there must be a sufficiently large and permanent expansion of the monetary base. On the latter point, Friedman knew that even though the monetary base and treasuries may be near perfect substitutes in a zero lower bound environment, they would not be in the future. And since investors make decisions on what they think will happen in the future, a monetary base injection that is expected to be permanent and greater than the demand for the it in the future is likely to affect spending today.

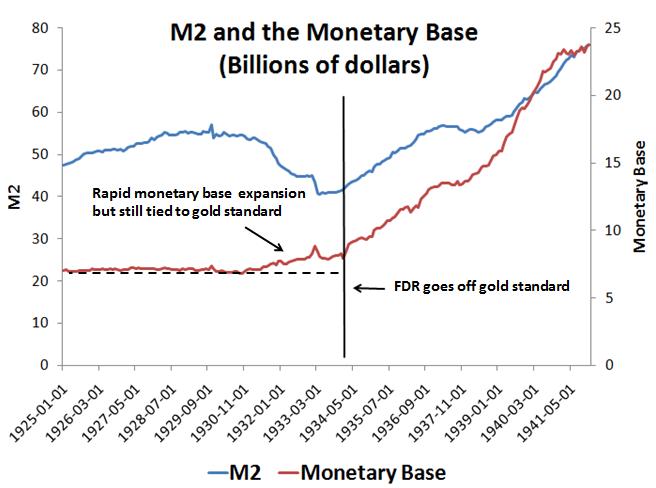

The importance of the public believing the monetary base expansion will be permanent can be illustrated by looking back to the early part of the Great Depression. As seen in the figures below, the monetary base grew rapidly between 1929 and early 1933 compared to previous growth. Yet during this time the money supply and nominal GDP continued to fall. The reason this monetary base growth did not stall the collapse of financial intermediation and aggregate spending is because it was still tied to the gold standard. Consequently, the public did net expect a large, permanent expansion of the monetary base. But that all changed with FDR in 1933. He created what Christy Romer calls a “monetary regime shift” both by signalling through articles, speeches, and movies a desire for a higher price level and by abandoning the gold standard which led to even more rapid monetary base expansion. This shift is apparent in the figures below. FDR’s actions caused the public to expect a permanent monetary base expansion that would raise future nominal income. A sharp recovery followed in 1933. 1

The key, then, to making monetary policy expansions work in a slump is to create the expectation that at least some part of the monetary base expansion will be permanent. Japan’s first try at quantitative easing in the early-to-mid 2000s failed on this front as noted by Scott Sumner and Michael Woodford. Here is Woodford:

The economic theory behind QE has always been flimsy…The problem is that, for this theory to apply, there must be a permanent increase in the monetary base. Yet after the Bank of Japan’s experiment with QE, the added reserves were all rapidly withdrawn in early 2006…

Well that was then and this is now. Prime Minister Shinzo Abe has committed the government to a radical monetary regime shift that is similar in spirit to FDR’s actions in 1933, as noted by Christy Romer. This program, called Abenomics, aims to permanently double the size of the monetary base and end the long run of deflation. It currently is engaged in asset purchases that are triple the size of the Fed’s relative to GDP. And the Bank of Japan has committed to doing more if needed.2 So this is a big regime shift and one that arguably fulfills Milton Friedman’s policy prescriptions for Japan.

It is too early to know for sure whether Abenomics is working, but the evidence so far suggest it is making a difference. Here is Ambrose Evans-Pritchard:

Abenomics is working,” says Klaus Baader, from Societe Generale. The economy has roared back to life with growth of 4pc over the past two quarters – the best in the G7 bloc this year. The Bank of Japan’s business index is the highest since 2007. Equities have jumped 70pc since November, an electric wealth shock.

“Escaping 15 years of deflation is no easy matter,” said Mr Abe this week, after winning control over both houses of parliament, yet it may at last be happening.

Prices have been rising for three months, and for six months in Tokyo. Department store sales rose 7.2pc in June from a year earlier, the strongest in 20 years.

I think Milton Friedman would be happy to see Abenomics if he were alive. Happy birthday Milton Friedman.

1Fiscal policy, though expansionary, was modest at this time. Thus Romer attributes, correctly in my view, most of the 1933 recovery to the new monetary regime.

2There is more to Abenomics including some modest fiscal policy stimulus and structural reforms. For now, though, the main part is the new monetary regime.

P.S. Whether one increases the monetary base through open market operations or through helicopter drops, the point that the increase remain permanent holds. See Willem Buiter for more this point.

The piece has bee cross-posted from Macro and Other Market Musings with permission.