Current austerity and quantitative easing policies are proving ineffective in the new era of historically low interest rates, high public debt, deleveraging, credit and liquidity crises, and recession/depression.

Recovery is failing to take hold with sufficient force, and some countries are sliding deeper into depression. Deflationary tendencies remain strong and unemployment is entrenched.

Austerity

Many economies are entrapped in austerity straitjackets. While effective in certain circumstances – for example, when the economy is growing strongly or can rely on external growth – austerity fails to achieve its own objectives if applied during recession/depression. In such circumstances, austerity is counter-productive: fiscal revenues contract, budget deficits increase, and public debts are pushed upward. Austerity aggravates recession or depression. Aggregate demand and output are dragged down, unemployment rises, and where price rigidities prevail real incomes fall. Prosperity is denied, confidence collapses, and wealth is ruined.

As Nouriel Roubini has recently pointed out, fiscal austerity policies have been excessively front-loaded in the periphery to seriously damaging effect. (See, ‘Crisis Revisited: Appropriate Fiscal Policy in the Aftermath,’ Roubini Global Economics, July 16, 2013).

Many European authorities still obstinately refuse to recognize the danger of crude austerity. As well, they fail to acknowledge that the austerity policies they believe might be rational for one country are not rational if all countries in the region undertake them simultaneously. In such circumstances, the magnitudes of national fiscal multipliers actually multiply.

Further Quantitative Easing (QE)

Countries relying on unconventional monetary policies are not expanding rapidly enough to break-free from deflationary tendencies. QE has dramatically increased base money, but not the money supply that drives aggregate demand.

QE injects money to Wall-Streeters, not to Main-Streeters. Traders, hedge funds, investors, financial engineers, banks, high-wealth individuals, and speculators benefit from QE-inspired bond and asset price bubbles. But that tiny minority has a low propensity to consume ordinary goods and services. QE does not reach the ordinary people – those who have a relatively high marginal propensity to consume – and deprives them of safe interest incomes. With given or falling incomes and wages, and being left out by QE, they may even reduce consumption spending. Spare capacity and aggregate expenditure short-falls continue on a vast scale. Demand-pull inflation is not triggered. In such circumstances, QE has no direct effect on consumer prices. QE-induced devaluation (in Japan say) does result in higher import prices, but at the expense of lower import prices (adding to deflationary tendencies) in other countries (the United States, for example).

QE is supposed to stimulate investment. However, inadequate demand, not high policy interest rate costs, is the key constraint. Share prices have increased and business cash holdings are generally buoyant. Larger companies are buying their own assets – share buy-backs and debt-equity swaps – with no effects on output and employment. On the other hand, smaller companies with limited access to capital markets find it difficult to borrow from banks as these are not willing to lend to risky businesses. Banks are recapitalizing and also accumulating unproductive reserves at the central bank. All this suggests the existence of a continuing ‘structural’ credit and liquidity crisis. In such circumstances, there is no evidence that further QE will significantly increase business investment in plant and equipment.

Moreover, where QE seeks to flatten the yield curve the pricing of risk becomes distorted throughout the economy. New capital investment is directed toward otherwise unproductive and unprofitable businesses. Interest rate-dependent decisions are based on artificial borrowing price signals. Bond price and asset price bubbles proliferate, and high-risk structured financial instruments re-emerge. Mere discussions of exit strategies increase interest rates, thus raising uncertainties.

Finally, global financial instability is increasing. If the United States withdraws QE while Japan massively expands its QE program there will be substantial exchange rate changes, disruptive capital movements, and further currency conflicts. The risks and unintended negative side-effects of extended periods of monetary easing have been acknowledged in the latest G-20 Communique (Moscow, 19-20 July).

In summary: consumption and investment demand, efficient risk-and-resource allocation, output and productivity growth, are arguably all being held back by QE, and the hopes for strong and sustained widespread economic recovery are not being realised.

Moving towards a practical pro-growth economic plan

Recently, the idea has been revived to enact ‘overt money financing’ (OMF) of the fiscal deficit in order to finance tax cuts or new public spending programmes.

Wood proposes OMF as the means to resolve the problems of insufficient demand and high public debt simultaneously (How to Solve the European Economic Crisis: Challenging orthodoxy and creating new policy paradigms, Amazon Books, December 11, 2012; “The Economic Crisis: How To Stimulate Economic Growth Without Increasing Public Debt”, Policy Insight, No 62, Centre for Economic Policy Research, VoxEU, August 2012; and, “Conventional and Unconventional Fiscal and Monetary Policy Options”, EconoMonitor, June, 2013).

Bossone, proposes a mechanism to apply OMF in Eurozone countries. (see Bossone, “Time for the Eurozone to shift gear: Issuing euros to finance new spending”, VoxEu, 8 April 2013. (http://www.voxeu.org/article/time-eurozone-shift-gear-issuing-euros-finance-new-spending), and Bossone, “Italy, Europe: Please do something!”, EconoMonitor, April 19th 2013. (https://www.economonitor.com/blog/2013/04/italy-europe-please-do-something/).

McCulley and Pozsar (“Helicopter money: or how I stopped worrying and love fiscal-monetary cooperation”, Global Society of Fellows, 7 January 2013) and Adair Turner (“Debt, Money and Mephistopheles: how do we get out of this mess”, Cass Business School Lecture, 6 February 2013) have reviewed the combined use of monetary and fiscal policies in a deleveraging context, concluding that OMF provide the most effective way to address falling prices and declining real output.

Accounting standards and credit-rating agencies

Wood takes into account the implications of accounting standards and the use by credit rating agencies of general government debt as a measure of ‘public debt’. Wood argues that one way around these institutional constraints is for governments to legislate to enable the Ministry of Finance (not the independent central bank) to create new local legal tender currency to be used to finance budget deficits.

Wood identifies three ways to implement his model (See more here):

- The Ministry of Finance of a country, Italy say, could use its newly created currency (say ‘new lira’) to directly finance a budget deficit of pre-determined magnitude. The ECB could stand ready to convert the new currency for Euro at a fixed exchange rate.

- The Ministry of Finance could create ‘new lira’ and the central bank could create an equivalent value of existing currency (‘Euro’): these two currencies tranches could be swapped immediately so that the Ministry of Finance could then finance the budget deficit directly using ‘Euro’, avoiding the need for two currencies to circulate simultaneously. The currencies could be swapped back at a much later date.

- The government could require that the Ministry of Finance issue special non-transferable new government bonds to the national central bank and/or the ECB in exchange for (new) euro to be used to finance the fiscal deficits. At a later date, if and when appropriate, and after economic growth has provided a revenue dividend, these bonds could be redeemed. The use of non-transferable bonds ensures that the bonds will not be sold into the private sector: hence they cannot add to debt held by the public or contribute to credit rating downgrades.

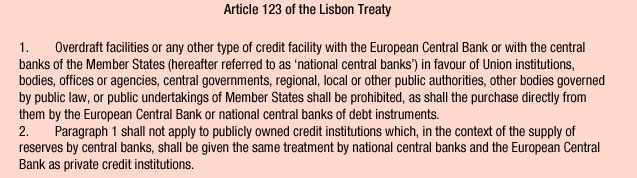

Navigating through Article 123 of the Lisbon Treaty

Under Bossone’s plan OMF can take place without generating new public debt, and without breaching Article 123:

- The central bank communicates to the government its readiness to finance, through money issuance, a fiscal package to achieve a pre-determined nominal demand (growth) target.

- The government issues new debt to be sold to the central bank in exchange for money. The central bank purchases the new debt and commits to holding it in perpetuity, rolling over the portion of it that reaches maturity, and returning the interest income to the government. Alternatively, the government issues to the central bank a non-interest bearing and never- redeemable note in exchange for newly issued money.

- The launch of the operation is accompanied by a central bank’s communication explaining that the OMF will not raise debt sustainability issues since the government securities will not be redeemed or sold to the market, will not pay interests, and will not give rise to government liabilities.

- At some future time, when economic growth and public finances will have been restored, the government may agree with the central bank on a plan for a (gradual) re-purchase of the note, if necessary. This would reduce the (ex ante and ex post) cost of OMF operations for central bank through money allocation.

Since no debt service burden will arise from OMF, no future tax revenues will be required and no (Ricardian) offsetting savings would take place.

Bossone argues that the above plan could be implemented by individual Eurozone countries in deep and protracted recession using as an extraordinary measure the Emergency Liquidity Assistance (ELA) facility provided for under the statute of the European System of Central Banks, and actionable by each national central bank of the system (Article 14.4 of the ESCB statute). Importantly, OMF through central bank money allocation to the government (see further below) under the ELA would not run counter to Article 123 of the Lisbon Treaty, since it would neither involve activation of overdraft or credit facilities in favor of EU public institutions nor the purchase of public debt instruments.

Turner (cit, footnote 22, p. 25) argues that the two alternatives identified in point 2 above are equivalent. If this is correct from the financial point of view (in both cases, the government would not return the money and would not pay interests to the central bank), the two alternatives might still differ from the legal and the accounting point of view, since in one case the government issues debt, while in the other case there is no debt obligation and the money issued by the central bank would amount to a money allocation from the central bank to the government. In accounting terms – in analogy to the Special Drawing Rights issued by the IMF and allocated to member states – the allocation of the newly issued money would appear on the asset side of the central bank’s balance sheet, while the reserves thus created would appear on the liability side. Correspondingly, the money allocation would show as a liability of the government toward the central bank, while the new reserves holdings would be on the asset side.

An objection to the money allocation could be that, while the central bank provides new money to the government, it gets nothing in return. Indeed, one could think of the new money as a “grant” of central bank money to the government, which is provided in the interest of society at a very critical juncture. In any case, extending the grant would cost nothing to the central bank, since the cost or producing money is zero. This owes to the right of seignorage through which the central bank creates purchasing power ex nihilo. In this case, its seignorage would be extracted and socialized as a way to help the economy recover from dire conditions. Provided that the newly created money would be able to mobilize economic activity, it would be backed up ex post by the additional output produced – as in circuit monetary theory or in Post-Keynesian models à la Paul Davidson (See Bossone, “Circuit theory of banking and finance”, Journal of Banking & Finance, vol. 25, May 2001, and Bossone, “Do banks have a future? A study on banking and finance as we move into the third millennium”, Journal of Banking and Finance, vol. 25, December 2001.

In any event, a central bank cannot become illiquid, and can operate quite effectively with negative accounting net worth. However, the following central bank’s balance-sheet effects of money allocation should be noticed. For those central banks that fair value their financial instruments, the money allocation would bear zero-value, implying an equity write-down of the difference between face value and fair value. Even if the central bank held the instrument at face value, the zero-income stream would asymptotically erode equity by the same amount. As for the cost of liabilities, on impact the servicing cost of the money allocation would be zero (central banks do not pay interest on government deposits with the central bank). Eventually, however, as the government mobilizes such deposits, they would be replaced by central bank’s reserves liabilities with the banking system. To the extent that these are remunerated, this would add to the costs for the central bank, requiring it to issue new money to pay for its interest liabilities. Furthermore, should the increase in base money subsequently need to be sterilised, sterilisation costs would be incurred by the central bank at somewhere close to market rates. Of course, nothing prevents the central bank from sterilizing money injections by raising the minimum reserve requirements and stopping remunerating reserves.

Remarks and observations

Under Wood’s proposals the Ministry of Finance initiates and directs the policy coordination, given its wider remit, responsibility for financing deficits, and the possible need to take-back the note issue function from the central bank. Under Bossone’s proposal the central bank assumes the initiative. In either case, strong coordination between monetary and fiscal policies would be essential. In the context of money financing of budget deficits, Olivier Blanchard et al have also asserted that “…it is essential that monetary policy decisions continue to be the sole purview of the central bank…” (see Blanchard O, Dell’Ariccia G and Mauro P “Rethinking macroeconomic policy: Getting granular”, VoxEU, 31 May 2013).

As a general proposition, in an economy experiencing severe recession/depression and high public debt, coordination between the (independent) central bank and the government should be ensured and subject to parliamentary control.

The comparative magnitudes are revealing. Consider the UK. The total value of new base money created to give effect to the purchases of government bonds (Gilts) under quantitative easing since 2009 has been around 375 billion Pounds. Had that new base money been used instead to fund additional budget deficits the added stimulus delivered over the past 3 years or so would have been around 26 per cent of GDP. (See Fawley B and C Needy “Four Stories of Quantitative Easing”, Federal Reserve Bank of St. Louis Review, 2013, January/February).

If Japan was to apply its latest announced monetary expansion to finance increased budget deficits, the added fiscal stimulus would amount to 30 per cent of GDP between now and the end of 2014. (See Magnus G “Carney to the Rescue”, Australian Financial Review, June 28, 2013).

In both cases there would be an increase of money in circulation, aggregate demand would increase but there would be no increase in public debt.

Conclusion

In many afflicted countries, borrowing – either from the public, commercial banks, central banks, other governments or the IMF – has already reached or exceeded its limits. Attempting to solve existing chronic debt problems through further bail-outs – taking on even more debt – is short-sighted: it creates new future obligations, condemns the debtor to long-term suffering, drains the budget, and limits his capacity to restore economic growth.

Current monetary and fiscal policies are not effective, efficient, or sustainable. They are not sufficiently coordinated domestically or internationally.

In Europe, a ‘banking union’ and a ‘fiscal union’ may represent desirable longer term goals, but they do not automatically address or resolve the current collapse of aggregate demand and GDP or the threat now posed by high and rising public debt.

Recent analyses of alternative policy options demonstrate that money financing of (increased) budget deficits – OMF – offers to deliver the most powerful stimulus possible without increasing interest rates or public debt. Since there is no ‘crowding-out’ and confidence would be favourably impacted, the fiscal multipliers would be relatively high.

OMF could replace current austerity and QE policies. Adverse side-effects (such as asset price bubbles, risk and resource misallocation, rising debt and unemployment, accumulating risk on unbalanced central bank balance sheets, or currency wars) would be avoided. Taxpayers of fiscally solvent states should welcome the proposed approach, as they would be relieved of having to bail out states that become insolvent due to bond financing of future budget deficits.

Even so, in some countries (particularly those at or near insolvency) debt deferral or restructuring would seem necessary to re-establish a workable equilibrium in a sensible timeframe. And, as austerity is wound down, renewed efforts would need to be made in uncompetitive countries to undertake appropriate structural reforms and needed adjustments to wages and prices. Medium-term fiscal consolidation could be resumed in earnest when economic recovery has taken hold.

Central banks could be left to address the exit strategy from QE over time, but that separate action would not preclude OMF from filling the policy void.

The scale of OMF could be set/limited by legislation. OMF should then begin operating immediately.

We are grateful to David Archer and Philip Turner for their very helpful comments on some technical central banking finance issues. Obviously, we remain responsible for the all ideas and opinions expressed in this article.