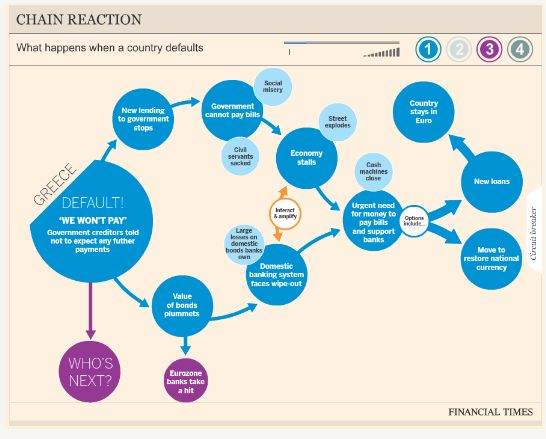

The Financial Times has gone through the very useful exercise of creating a decision tree on what a Greek exit from the euro zone entails. I think the Europeans are now actively preparing for a Grexit because to not do so would be folly. But that doesn’t mean that they want Greece to be forced out. Much of what we hear for public consumption is real. But much of it is also political posturing to improve negotiating positions. This decision tree can be helpful in figuring out what’s real and what’s just bluff.

Source: Consequences of a Greek eurozone exit, Financial Times

This post originally appeared at Credit Writedowns and is posted with permission.