What is Peak Oil About?

Let’s start with The Economist:

As the developed-world economy tries to gain momentum, it faces a persistent headwind. The oil price remains stubbornly over $100 a barrel, acting like a tax on Western consumers. Some blame the high price on evil speculators—Barack Obama unveiled plans to increase penalties for market manipulation on April 17th. But there is a simpler explanation: that supply is inadequate to keep up with rising demand.

The concept of peak oil—the idea that global crude production may be at, or close to, its limit—is far from universally accepted. One leading asset manager talked recently of the world being “awash with energy” because of the exploitation of American shale gas. Nevertheless, oil is still the main fuel for cars and trucks. And crude output (as opposed to alternatives such as biofuels and liquids made from gas) has been flat since 2005.

A number of countries (including Britain, Egypt and Indonesia) have turned from net oil exporters into importers in recent years. And although rich countries have curbed their energy-guzzling a little, demand continues to surge in emerging markets.

This has left the oil market very vulnerable to temporary supply disruptions, such as the war in Libya.

This is a good synopsis of the real issues for individual economies. Let me get into how the peak oil argument is framed first before we look at what is happening. There are two versions of the peak oil theory: the hard peak oil view and the soft peak oil view.

Hard peak. The esoteric argument, derived from M. King Hubbard’s now undisputed prediction of peak oil in the (lower-48) United States, is that half of all oil reserves were consumed by 2005 or so and that means we have less than half left. According to King’s analyses about the relationship between reserve discovery and production and the rates of production decline in exploited oil fields, this would mean we have hit the absolute peak of oil production globally. The point is that no matter what happens, production from conventional oil sources will not increase… ever. That’s what I would call the “hard peak oil” argument. This argument is controversial.

Soft peak. The most relevant argument is a bit more subtle – and this is the one the Economist delves into. Here, it is not disputed that we will one day hit an absolute peak when half of the world’s extractable oil reserves have been consumed. Nor is it generally disputed that technology will be hard-pressed to increase production levels when we have consumed half of the oil. What is important here is that the cost of incremental supply exceeds the price at which demand destruction kicks in. Put simply, we are now at a point where oil prices are so high that if they go any higher, people cut back on consumption, threatening recession. I call this the soft peak.

The Impact of Oil on the Economy

Clearly, we have seen demand destruction a number of times in the last 40 years. In fact, every global recession in that time frame was preceded by oil shocks except the one after the tech bubble. We have had four global recessions on the heels of an oil price shock: in 1973, 1979, 1990 and 2008. So, the mechanism for how high oil prices lead to demand destruction and recession – as well as social unrest – is clear. The question is whether oil prices are high based on oil market fundamentals that are consistent with the soft peak oil argument or whether the rise in oil prices is due mostly to commodities speculation.

If you are a politician, you don’t like demand destruction because that slows growth and makes you look like you are presiding over a sluggish economy. The concept that these prices are due to some controllable factor is therefore very compelling for politicians and they will always act upon it. The Economist begins their article describing Barack Obama’s plans to go after commodities market manipulators for just this reason – high oil and commodity prices are politically combustible and President Obama’s plan is an attempt to defuse this as an election issue come November.

Politicians of all stripes will do whatever they can to tamp down these high prices. For example, in Argentina, President Cristina Fernandez de Kirchner has complained bitterly about high prices and Argentina,’s new role as oil importer. Fernandez has blamed the country’s oil company YPF for not increasing production. Her view is that the company’s Spanish owner Repsol is a rent seeker bent on extracting wealth from the company without adequately reinvesting in the Argentine economy. Recently Fernandez took action, nationalising the company and has decided to seek partners to exploit Argentine oil reserves, most likely China’s CNOOC or Sinopec. But clearly, peak oil could also explain Fernandez’s dilemma.

As for the speculation argument, there is plenty of evidence to support it. Commodities have been financialized, meaning they are readily available for purchase and sale as financial assets via primary and derivative financial markets. That means that the Fed’s zero rate policy causes investors in fixed income and annuities to seek alternative investments in commodities and other financialized real assets like precious metals. With commodities, Professor of Economics Randall Wray, of the University of Kansas City at Missouri and a frequent Credit Writedowns contributor, calls commodities speculation “The Biggest Bubble of All Time“:

An April report by expert Jeremy Grantham looks at the last decade’s bubble in commodities; Frank Veneroso expands upon that in a more recent report. Here’s the elevator speech summary. Take the top 33 commodities that are globally traded—everything from gold and oil to to rubber, flaxseed, jute, plywood, and something called diammonium phosphate. Over the past 110 years, an index price of these 33 commodities has declined at an annual rate of 1.2% per year. (Sure there are variations across the commodities—this is the average. And so much for inflation hedges. Commodities prices fell—they did not keep up with inflation. If you liked negative returns, commodities were a good bet.) Although demand for these 33 commodities has increased a lot over the century, new production techniques plus successful exploration has resulted in a declining price trend.

Further—and this is a bit surprising—deviations from the trend follow a normal distribution (you learned about this in high school; it is a bell curve with nice properties; chief among these is the finding that about 68% of outcomes fall within one standard deviation; about 95% fall within two standard deviations (once a generation); and you’ve got just about a snowball’s chance in hell of finding outcomes that are three or four standard deviations from the mean).

But what is more surprising is that over the past decade, the price rises you find for these 33 commodities are just about beyond the realm of possibility—2, 3, and 4 standard deviations away from trend. It is a boom without any precedent. Quite simply, nothing even close has ever happened before, in any market, including hi tech bubbles and real estate bubbles.

Professor Wray’s conclusion: speculative fervour is causing an asset price bubble in the commodities sector, not just for oil alone.

Le Figaro: Hard Peak

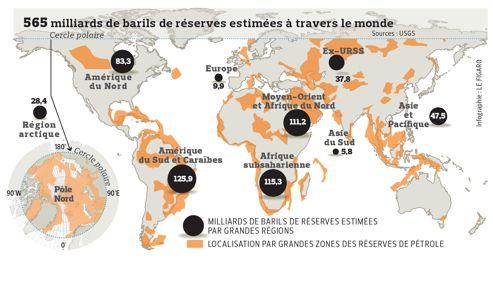

Looking at the other side of this, I saw in Le Figaro on peak oil and the controversy over oil reserves. My translation of an excerpt from French is below, with a chart from that article

…According to the USGS, “undiscovered but technically exploitable” reserves total 565 billion barrels for oil, and 158,760 billion cubic meters for natural gas. That is the equivalent of seventeen years of world consumption in 2011 for oil and fifty years for gas.

The U.S. report took into account neither the reserves of the United States, subject of separate studies, nor so-called unconventional resources like oil and gas from shale or tar sands. The estimates are based on the study of the geology of 313 areas across nine major world regions. three-quarters of the potential are concentrated in four of them, South America, sub-Saharan Africa, the Middle East with North Africa and the Arctic. Adding so-called proved reserves to those newly identified by the USGS would provide sixty years of oil consumption at the level of 2011 consumption.

Biased data

A misleading picture, protests Jean Laherrère, former head of exploration techniques at Total and president of ASPO (Association for the Study of Peak Oil and Gas). This work is “not scientific”, he condemns, citing estimates from the USGS in 2000, not verified by facts, and reflects the ignorance of the authors about the realities of oil exploration. Concerning oil, “public data are either political or financial, and are mostly biased”, warned Laherrère in a note circulated at the Club of Nice, a conference of energy experts in late 2010. As confirmation of these criticisms, hardly had the USGS published its estimate when the U.S. Department of the Interior congratulated it. In a statement released Wednesday, the agency welcomed the visit of Secretary Ken Salazar to Brazil to forge energy partnerships in this region among the world’s richest reserves of oil.

Without denying the existence of huge reserves of oil and gas yet undiscovered , Laherrère and many experts worldwide working for decades on the notion of “peak oil” (“peak oil”, in English) recall that operated field production declines at 4.5 to 6.7% per year. All while world demand rises. “The production has been roughly constant over the past seven years despite an increase in crude prices by about 15% per year,” noted climatologist James Murray and economist David King in an article published on Peak Oil in the scientific journal Nature (January 26, 2012).

Faced with uncertain numbers but the inexorability of the underlying trend, seven experts including Laherrère published a forum last month at lemonde.fr calling on presidential candidates to anticipate an energy transition, otherwise ” it will be chaotic” with “disastrous economic consequences.”

The Financial Times: Soft Peak

That’s the hard peak view. And as I have said, it is controversial. The Financial Times takes up the soft peak story:

It’s nothing new, this questioning of what permanently higher oil prices means for world economic growth. Gregor MacDonald, Chris Nelder and Gail Tverberg are just a few of those who’ve been dedicated to considering the economic effects of an energy-constrained world. James Hamilton has been attempting to bridge the gap between peak oilists and economist for years; his ‘How to talk to an economist about peak oil‘ post (from 2005!) is a must-read.

[…]

The question of what that impact will be, and how it will be managed, is much more interesting than straw man arguments about when exactly the oil will “run out”.

I think that’s it exactly. Even forgetting about the hard peak story, we can focus in on whether the soft peak story explains much of the run up in oil prices and what impact this could have over the longer term. It may be the case that peak oil explains much of the increase in prices irrespective of speculative excess. In my view, then the story about a “chaotic” energy transition with “disastrous economic [and investing] consequences” would be the same.

This post originally appeared at Credit Writedowns and is posted with permission.