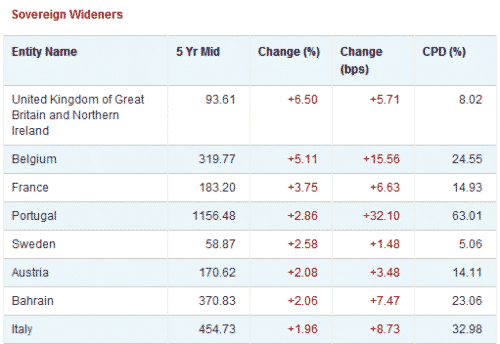

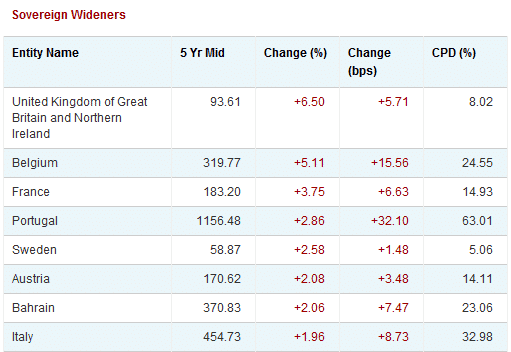

First, in the sovereign space, the UK was the biggest widener on the day, but the default probability is only 8%. I don’t see this as anything to note. On the other hand, if you look at the numbers for Belgium, and France and Austria to a degree, the default probabilities are getting worrisome. When thinking about sovereign contagion, those are the three countries to think about.

Here’s Win Thin last year on Belgium (and France and Austria):

Here are some more thoughts on S&P moving its outlook on Belgium’s AA+ rating to negative from stable. S&P noted that it may cut the rating by one notch within the next six months if the major political parties do not form a government soon, and added that a cut could still be seen over the next two years if the next government fails to stabilize public debt and improve political cohesion. S&P analyst noted that the current caretaker government may be “ill-equipped” to respond to any shocks to the public finances. In our view, Belgium and France are the weakest credits in the core as our sovereign ratings model still puts France as a borderline AA+/Aa1/AA+ credit compared to actual ratings of AAA/Aaa/AAA. While Belgium does have weak fundamentals, our model shows it to be correctly rated at AA+/Aa1/AA+. However, we acknowledge that contagion remains strong in the euro zone and we cannot rule out a downgrade for Belgium since the rating agencies remain on the warpath. As we saw during the Asian crisis, the agencies tend to overcompensate on the downside in times of crisis as they try to regain lost credibility.

The budget and debt ratios for Belgium have always been high, but we note that the rest of the core has in a sense caught up with Belgium during this crisis. In 1999, there was a gap between the debt/GDP ratios of Belgium and France of 55 percentage points. In 2010, that gap was only 16 percentage points. The market is now viewing Belgium as twice as risky as France, as its 5-year CDSs are trading at 204 bp vs. 101 bp for France. Indeed, this puts Belgium right around Italy (208 bp) and shows that the distinction between core and periphery is getting harder and harder to make. After France and Belgium, we view the next weakest core country as Austria, and note that its CDSs are trading at 93 bp today. CDS prices for Belgium, France, and Austria have all moved significantly higher over the past month and reflect growing contagion risk for the entire euro zone.

As I said in July, I expect contagion to be a real concern regarding the dithering policy approach. I believe the sovereign debt crisis will continue to deteriorate further for just this reason.

My argument has been that the extend and pretend route to prevent contagion doesn’t work. The contagion is already all around and no one has defaulted yet. Indeed, it is precisely because Greece has not defaulted that there is contagion to begin with. People want to know who is insolvent and who isn’t. Once they do know, the creditors writ large i.e. holders of bank debt, depositors, and taxpayers, can fight over how to apportion the losses.

So, what happens is that the crisis rolls through. More and more countries in the euro zone get plucked off and put into the penalty box. First it was Greece. Then it was Ireland and Portugal. Later the crisis rolled into Italy and Spain.

There are ever fewer players left to skate. Now we see Belgium in big trouble. Austria and France cannot be far behind. Once France has difficulties, the core only has one country, Germany, which is a truly large economy, capable of shouldering any burdens. In my view, that is the end of the line.

This is a rolling crisis wave through the eurozone infecting more countries, closer and closer to the core. As Marshall wrote recently, this is a structural problem. All of the euro zone countries face liquidity constraints and all of them will eventually succumb to the rolling wave of yield spikes one by one until we get a systemic solution: full monetisation and union or break up.

–Felix Zulauf on the inevitability of further crisis in Europe

Also Read: Felix Zulauf: Expect More Market Turmoil Than in 2008

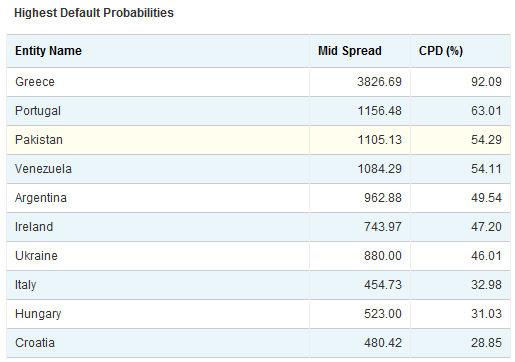

Second, notice here on this chart below how high the Italy default numbers are. Spain is not on this chart of the most likely sovereigns to default anymore. Italy is now.

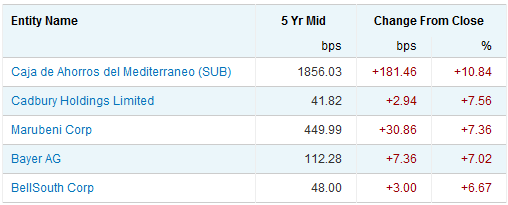

On the private sector debtors, it’s all about the banks. I just want to highlight the Spanish savings bank Caja de Ahorros del Mediterraneo (CAM) that has seen its spread widen significantly.

The reason Italy is in the hot seat instead of Spain has to do with the genesis of crisis. Spain’s sovereign was healthy before the crisis. Even now, sovereign debt to GDP is very manageable. The problem in Spain is the banks.

In April I wrote (when the crisis was all about Spain):

Depending on how the Irish stress test are received, the Irish could either finally put a line under the crisis or precipitate more concerns that spill over to Portugal or Spain. It’s Spain that counts since it is larger than the three other eurozone periphery countries combined. We would not like to see contagion to Spain because that would put the whole euro project at risk…

“Yes, the CAM thing is a disaster that shows the government’s recap plan won’t work. They need plan B now or contagion is coming.” But do they have plan B? Let’s hope so. But we have our doubts.

The Irish did put a line under the crisis. Investors feel they have taken substantially all credit writedowns. So their economy and spreads have improved. Of course, that improvement goes away in a European double dip scenario. But, net net, this was positive for Spain. The Spanish wanted to get private capital injections into their failing banks. That plan A didn’t work. No one ponied up. CAM failed the stress tests in July. At which point, it was nationalised (link in Spanish). So, plan B was a government backstop.

Why are CAM’s spreads widening then? Don’t tell me it’s because Spanish banks are now feeling the heat after Dexia’s collapse. Shouldn’t other non-backstopped Spanish banks see more spread widening if the European Bank Run is now moving to Spain? If anyone has the answer, please post in the comments.

This post originally appeared on Credit Writedowns and is reproduced here with permission.