Introduction

The growing current account imbalances between several countries of the European Monetary Union (EMU) are generally not perceived as a core feature of the current Euro crisis. Most notably, Blanchard (2007) has argued that these imbalances have arisen from the deeper capital market integration resulting from the monetary unification allowing domestic agents to get easier access to international funds. From this perspective, the diverging current accounts in Europe reflect an optimizing behavior of agents under free-market conditions. On the other hand, the abolition of country-specific nominal exchange rates has led to a significant decrease in the real exchange rate flexibility in the Euro Area. Therefore, the present current account imbalances may be the result of the Euro Area’s inability to fully adjust to macroeconomic shocks through real exchange rate adjustments.

How to define debt sustainability?

As in Schoder et al. (2011), we consider two definitions of external debt sustainability, which we then test for ten early EMU-countries[i] from 1975 to 2009. First, we can call the development of an external debt-to-GDP ratio over time sustainable if it is consistent with the requirement that investors expect the stock of debt relative to GDP to converge to zero over time. A sufficient condition for debt to be sustainable is that the response of the net exports to a change in external debt is positive on average.[ii] Second, we can call a debt-GDP process operationally sustainable if it keeps returning to some long-run average, i.e. if it is stationary.

Are the growing imbalances optimal?

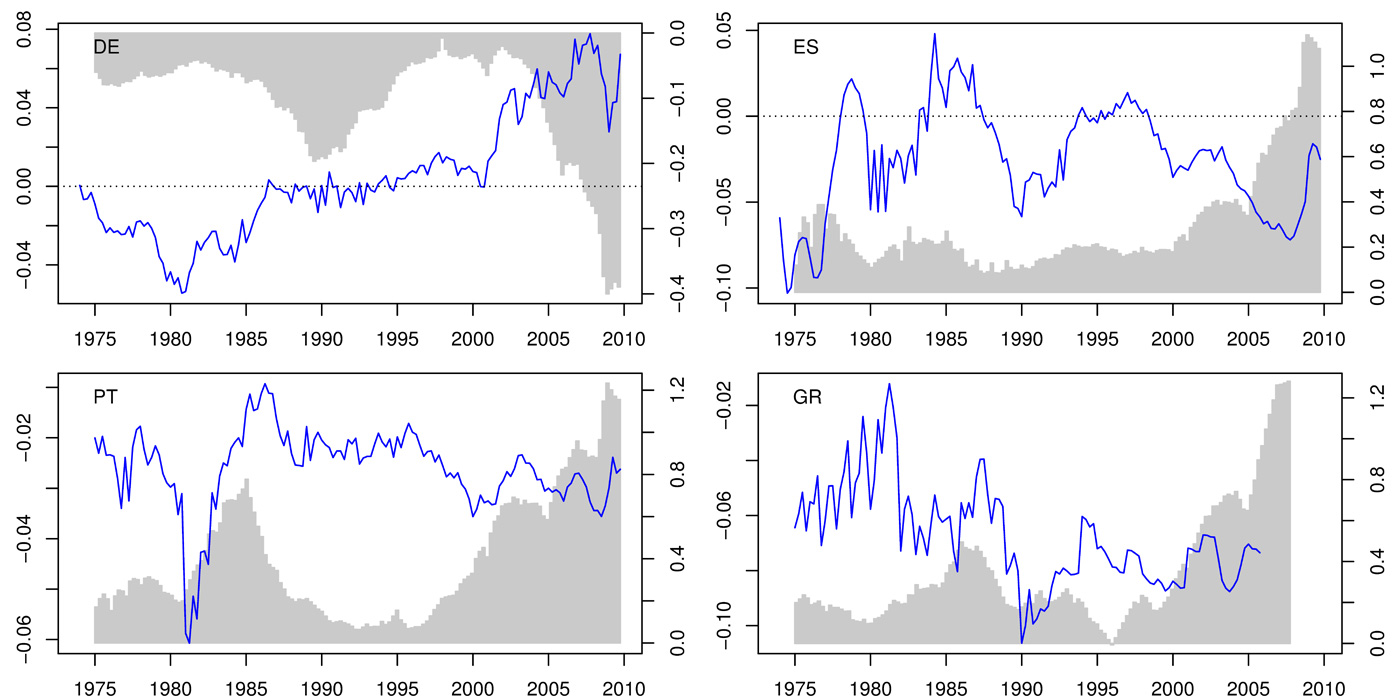

In recent years, the size and persistence of trade deficits in Euro countries such as Italy, Spain, Portugal and Greece led to a significant rise in their external debt. At the same time, other European countries such as Germany, France and Finland have managed to run persistent current account surpluses and to accumulate positive net assets. Figure 1 illustrates these developments, plotting the net exports-GDP ratio and the debt-GDP ratio for Germany, Spain, Portugal and Greece.

Figure 1: The net external debt-GDP ratio (bars, right axis) and the net exports-GDP ratio (solid line, left axis) for four European countries from 1974:Q1 to 2009:Q4

In order to investigate whether the diverging current accounts among EMU countries can be considered sustainable along the lines of the previous definition, we estimate this relationship by employing an error correction model. This also allows us to determine the speed of adjustment by which net exports adjust to a change in external debt.

Click for enlarged table.

Column (a) in Table 1 reports the results for an estimation including all countries over the entire period considered. In this most general specification, we find a significantly positive common long-run response coefficient. This suggests that the accumulation of debt of the countries considered has been sustainable on average. The speed of adjustment implies that, on average, it took the net exports 7 quarters to adjust halfway to a one-unit change in the external debt.

The parameter estimates for the two sub-periods before and after the introduction of the Maastricht convergence criteria are reported in column (b). By splitting the sample, we are able to observe that the average long-run response coefficient decreased substantially and even turned negative in the Euro period. The speed-of-adjustment coefficient seems to have also decreased in absolute terms in the second period. While, in the former period, it took the net exports 5 quarters to adjust halfway to a one-unit change in the external debt, it took 8 quarters in the second.

This striking finding strongly suggests that within the currency union, which so far lacks ambitious policy coordination, adjustment through productivity growth and labor mobility is insufficient to keep trade accounts balanced and imbalances sustainable.

Are the debt-GDP ratios mean-reverting?

As defined above, a debt-GDP ratio is operationally sustainable if it keeps returning to some long-run mean. To analyze the mean-reverting properties of the debt-GDP series, we employ a unit root test for panels of countries.[iii]

Click for enlarged table.

The test results are reported in Table 2. We can reject the null of a unit root at the 5% significance level for the panel including all countries and covering the whole sample period as indicated in column (a). Hence, on average, the accumulation of external debt relative to GDP has been mean-reverting and, therefore, could be considered as operationally sustainable. The same holds for the period before the implementation of the EMU criteria (column (b)). Yet, for the period thereafter, we cannot reject the unit root hypothesis at any reasonable level of significance. Debt accumulation seems to have turned unsustainable on average. Once more, this suggests that the current account imbalances in Europe are not optimal and may jeopardize the stability of the Euro system. Column (c) shows that non-stationarity holds especially for the southern countries and Germany. For the other northern countries, the unit-root hypothesis can be rejected. To some extent, this reflects the imbalances between the Exportweltmeister Germany and the periphery countries.[iv]

Does the Euro alleviate or reinforce imbalances?

To determine by statistical measures whether the introduction of the Euro contributed to current account imbalances between the EMU countries, we use non-parametric estimation techniques. These allow us to estimate both the measure for sustainability (the response of net exports to debt) and the measure for operational sustainability (the persistence of the debt-GDP ratio) as functions of exchange rate flexibility. As illustrated in Figure 3, the real exchange rate volatility decreased substantially in the north and the south after the introduction of the Maastricht criteria in 1997.

Figure 2: The real effective exchange index rate based on the CPI for northern and southern European countries from 1974:Q1 to 2009:Q4

If the introduction of the Euro aggravated the current account imbalances by impeding the real exchange rate adjustment mechanism, then one would expect a positive (negative) relationship between the response coefficient (the auto-regressive coefficient) and the flexibility of the real exchange rate.

Figure 3 plots this relationship for the response coefficient for pooled estimations of the northern and southern European countries. In the north, the response coefficient seems to have increased, on average, with decreasing exchange rate flexibility. Thus, the exchange rate mechanism seems not to be so important for trade adjustment in these countries. We find the opposite for the south: the response coefficient decreased, on average, with decreasing exchange rate flexibility. Hence, the exchange rate mechanism seems to have been more important for southern than for northern countries. This suggests that the abolishment of flexible exchange rates through the EMU and rising rigidities in nominal adjustment mechanism have been more harmful to southern than to northern countries.

Figure 3: The relationship between the response of the net exports-GDP ratio to a one-unit change in the debt-GDP ratio and real exchange rate flexibility from 1974:Q1 to 2009:Q4

The auto-regressive coefficient as a function of the exchange rate volatility is plotted in Figure 4 for the north, excluding Germany, and the south including Germany. We find a similar result as above. In the north, the adjustment of the debt-GDP ratio to a long-run mean seems to accelerate with decreasing exchange rate volatility. In the south and Germany, however, decreasing real exchange rate flexibility is accompanied by a higher persistence of current account imbalances.

Figure 4: The relationship between the auto-regressive coefficient of the net exports-GDP ratio and real exchange rate flexibility from 1974:Q1 to 2009:Q4

Overall, these findings are consistent with the above results, indicating that current account imbalances in Europe became unsustainable in the era of the Euro. They strongly suggest that the introduction of the EMU affected the north and the south inversely and was somewhat harmful to the latter. The Euro seems to have slightly alleviated trade imbalances between northern countries without Germany, but reinforced the external imbalances between Germany and southern Europe.

Imbalances and the European sovereign debt crisis

Although there is no straightforward empirical relationship between current account and public sector deficits, it is not a coincidence that the South European countries (Italy, Spain, Portugal and Greece) with large external deficits are confronted with a sovereign debt crisis. Since, as an accounting rule, the balances of the public sector, the private sector and the foreign sector have to add up to zero, a current account deficit (i.e. a surplus of the foreign sector) is necessarily associated with either a deficit in the public or private sector, or both. In the last decade, all southern European countries experienced a significant rise in household debt facilitated by financial market liberalization that fueled credit market booms and increased the fragility of the banking sectors. Private and partly public borrowing booms fueled import demand and contributed to the accumulation of external debt. After the credit bubble burst, sovereign debt rose in all southern European countries.

Policy implications

Our findings suggest that the recent development of current account imbalances among European countries is unsustainable and, therefore, cast some serious doubt on the view that the diverging current accounts are consistent with optimal behavior of economic agents as proposed by Blanchard (2007). Further, we have argued that the introduction of the EMU has contributed to the growth and persistence of these imbalances. The EMU eliminated the nominal exchange rate mechanism, and the common monetary policy aimed at price stability reduced the flexibility of inflationary adjustment. The Stability and Growth Pact and its rather inflexible requirements for national economic policy appears sub-optimal for monetary unions with economies that develop unevenly. Given the low labor mobility between European countries, we can therefore conclude that ambitious policy measures need to be implemented to reduce current account imbalances.

External re-balancing would facilitate overcoming the sovereign debt crisis in southern Europe. Policy measures aimed at increasing economic growth to grow out of the debt crisis would be more effective if the external account was not in deficit. This is because, in this case, a higher share of the domestic demand generated by expansionary policies would be realized in the home country and not abroad through imports.

Our results reinforce the view that ambitious political action is required to overcome the external imbalances. Although the literature and the public discourse diverge regarding the question of whether adjustment should take place in the surplus or deficit countries, a broad consensus seems to prevail on core requirements to reduce current account deficits:

First, the relative competitiveness of deficit countries needs to be increased. This cannot be achieved by limited wage growth in the deficit countries only, but must include an expansionary wage policy in the surplus countries. In any case, the benefits of a coordinated wage policy within the Euro Area become evident.

Second, instead of letting credit flows be regulated by the interest payments and bond yields, funds and low-cost credit for productivity enhancing infrastructure could be provided for the periphery countries. Thus, an EU-wide management of credit and investment flows may reduce an uneven development of productivity.

Third, the divergent development of domestic demand among EMU countries – due to regional boom-bust cycles – needs to be reduced as domestic and external demands drive imports and exports, respectively. Again, coordinated wage, credit and fiscal policy may allow for active management of relative domestic demand developments and help reduce current account imbalances.

References

Blanchard, O. (2007): Current Account Deficits in Rich Countries, IMF Staff Papers,

54(2), pp. 191-219.

Bohn, H. (1998): The Behavior of U.S. Public Debt and Deficits, The Quarterly Journal of Economics, 113(3), pp. 949-963.

Bohn, H. (2007): Are stationarity and cointegration restrictions really necessary for the intertemporal budget constraint?, Journal of Monetary Economics, 54(7), pp. 1837-1847.

Breitung, J. (2000): The Local Power of Some Unit Root Tests for Panel Data, in: Baltagi, B., eds., Nonstationary Panels, Panel Cointegration, and Dynamic Panels, Advances in Econometrics, Vol. 15, JAI, Amsterdam, pp. 161-178.

Pesaran, M. H., Shin, Y., Smith, R. P. (1999): Pooled Mean Group Estimation of Dynamic Heterogeneous Panels, Journal of the American Statistical Association, 94(446), pp. 621-634.

Schoder, C., Proaño, C. R., Semmler, W. (2011): Are the current account imbalances between EMU countries sustainable? Evidence from parametric and non-parametric tests, SCEPA Working Paper 2011-6, Schwartz Center for Economic Policy Analysis (SCEPA), The New School.

[i] Germany (DE), France (FR), Finland (FN), Belgium (BG), the Netherlands (NL), Austria (AT), Italy (IT), Spain (ES), Portugal (PT) and Greece (GR).

[ii] This has been shown by Bohn (1998).

[iii] We group countries with similar autoregressive coefficients in the debt-GDP ratio, i.e. France, Finland, Belgium, Netherlands, Austria (North w/o DE) vs. Germany, Italy, Spain, Portugal and Greece (South w DE). We employ the testing procedure developed by Breitung (2000). Assuming that the debt-GDP ratio in period t is defined as debt-GDPt = mean + ρ * debt-GDPt-1 + εt where εt is a random shock, we test the null hypothesis of ρ=1 (unit root) against the alternative hypothesis ρ<1 (stationary). Only under the alternative hypothesis the debt-GDP ratio keeps returning to its mean and is operationally sustainable.

[iv] Due to space constraints, we do not discuss here the question to what extent the German asset accumulation is a mirror image of the Southern countries’ debt accumulation. Schoder et al. (2011) discuss in detail the conditions under which such a symmetry holds for an open economic area and apply them to the countries considered here.