For more than a decade now, China has had a sizable current account surplus, while the U.S. has been running an even larger current account deficit. In macroeconomic terms, this also means that savings have exceeded investment in China while the opposite has been happening in the U.S. This has resulted in China accumulating net foreign assets and the U.S. seeing its Net International Investment Position deteriorate. As at the end of 2011, the value of foreign liabilities of U.S. residents exceeded the value of their foreign assets by more than USD4 trillion. At the same time, the foreign assets of the residents of China exceeded their foreign liabilities by almost USD2 trillion.

To prevent the above imbalances from growing, both countries would as a minimum need to bring their current accounts back toward balance. Doing that and maintaining economic growth at the same time would require China to consume and import more, while the U.S. would need to increase its output and exports. The alternative way of rebalancing – China producing and exporting less and the U.S. consuming less would be a recipe for economic contraction.

The need for China to change its economic growth model from an export and investment driven to a consumption driven one has been discussed extensively (see, for example, Yongding or Chovanec). It is far from certain that China will be able to complete this transition without experiencing a considerable economic slowdown in the process. However, the other side of the required rebalancing is at least as important, but has recently attracted less attention. Namely, the U.S. would need to shift the emphasis in its economic growth model away from consumption and towards production and exports, which would also require considerable investment both on the company level and in the public infrastructure.

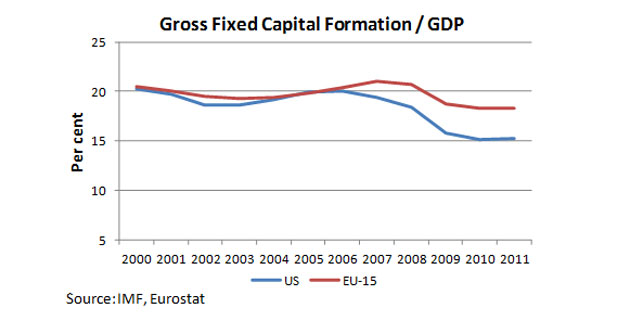

Recent evidence, however, suggests that while U.S. GDP growth has surpassed its pre-crisis level, investment has been declining. A comparison with China would not be appropriate due to differences in growth rates and the level of economic development, but even a comparison with the EU-15 is not flattering to the U.S. A look at the Gross Fixed Capital Formation to GDP ratio shows that since the onset of the financial crisis in 2007 the U.S. has been lagging behind the EU-15 countries with respect to investment in long-term assets (see chart below).

Also, the weight of construction sector in total value added has been consistently lower in the U.S. than in the EU-15 and has been declining since 2007 (see chart below). Not all investment or construction enhances the potential output of an economy. However, public infrastructure investment in the U.S. stands at 2.4% of GDP, half the level it was 50 years ago and half the level in Europe (Thomasson, The Economist). This is everything else but logical, in particular, given the record-low levels of long term interest rates. As Peter Orszag put it in a discussion at the Buttonwood Gathering, the current level of the 10-year Treasury yield and the current state of the JFK airport should not coexist.

The way the U.S. has dealt with the financial crisis – by running large budget deficits, keeping down interest rates and performing several rounds of quantitative easing – has often been contrasted favorably with the “austerity” approach in Europe. However, the massive fiscal and monetary stimulus also appears to have been an obstacle to structural change in the U.S. economy; in particular, it has failed to revive investment and prepare for the much needed transition from a consumption-oriented growth model to a production-oriented one.

Private investment has not been stimulated by extremely low interest rates. Uncertainty about the future investment climate remains high. Perhaps if Congress and the president could cooperate and make a credible commitment to resolve the long-term debt problem and increased certainty about future government taxation, spending and borrowing would increase private investment. However, acting in ways that take account of future costs and benefits has not been a strong suit for recent Congresses or presidents. They have only begun to take account of the “fiscal cliff” that will appear at the end of next month. Nor have they been able to agree on major new infrastructure spending, as Thomasson has pointed out.

Unless the situation is reversed quickly, this means bad news for both the U.S. and the global economy down the road. If insufficient investment results in the U.S. having to adjust by lowering consumption rather than increasing output, the rest of the world will also have to adjust in a way that is reducing growth; namely, produce less.

References

Bureau of Economic Analysis of the U.S. Department of Commerce, „U.S. Net International Investment Position at Yearend 2011”, June 26, 2012

Chovanec, Patrick, “Silver Linings in China’s Slowdown”, August 6, 2012

The Economist, “Life in the Slow Lane”, April 28, 2011

Thomasson, Scott, “Encouraging U.S. Infrastructure Investment”, Council on Foreign Relations, April 11, 2012

Yongding, Yu, “China’s Rebalancing Act”, Project Syndicate, September 26, 2012

Wall Street Journal, „Investment Falls Off a Cliff”, November 19, 2012