Europe is headed toward recession – in fact, it’s probably already contracting – and EU policy makers agreed to explicitly enforce contractionary policy. Kevin O’Rourke calls it a Summit of Death, while Paul Krugman argues the impossibility of the grand internal devaluation experiment. I call it economic oppression coupled with zombie bank deleveraging – it is absolutely not in Spain’s best interest to be pushing sharp fiscal contraction while the private sector is itself deleveraging.

But alas, they’ve decided to put off the only credible solution, fiscal union, for another time. I suspect that global investors are going to see right through this simple fact. External investors will grow tired of the zombie deleveraging and recession, of which more selling will cheapen bonds further. Regarding bond spreads, why should this Summit lead to any different outcome than the ones before it? It shouldn’t.

Until EA policy makers make a concerted step toward fiscal union, the bond crisis will continue to evolve just as it has at each crossroad in the past. The european sovereign crisis will deteriorate further.

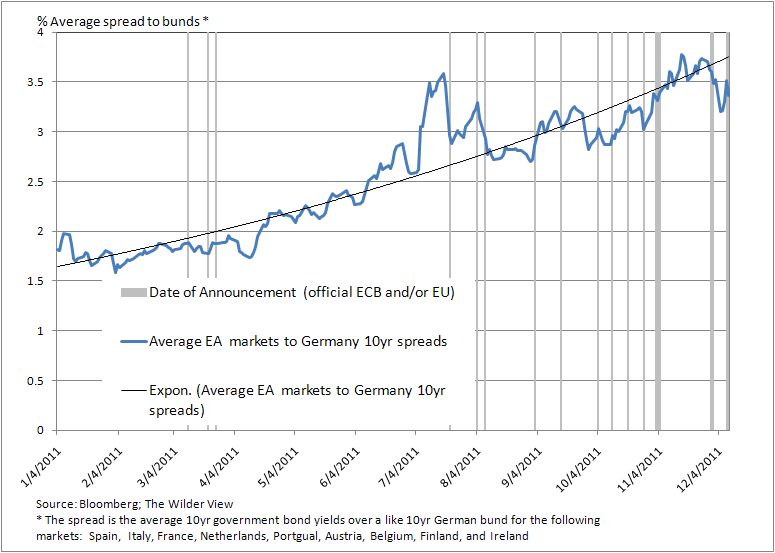

The chart above illustrates the average 10yr spread of the 9 bond markets listed over a like German bund alongside each major announcement date (see table below) through December 9. The trend has been up while volatile. Furthermore, no announcement to date has successfully stemmed the upward bias in bond spreads. EA policy makers consistently avoid the only truly credible answer: fiscal union.

Appendix

The table below lists the dates and associated ECB/EU announcements used in the chart above.

Also Read: The Rebirth of Social Darwinism